If you have been watching your home loan repayments climb since 2022, you are not imagining things. The RBA cash rate moved from 0.10% in April 2022 to 4.35% by November 2023, taking variable mortgage rates up roughly four percentage points in the process. A lot of Australian borrowers are paying more than they need to, and reaching for a refinance home loan calculator is usually the first step in working out what to do about it. That anxiety about overpaying is completely valid.

But before you jump ship to a new lender, you need to answer two questions. How much could you actually save by refinancing? And how quickly do you break even on the costs of switching? Here is the problem with most online tools. A typical refinance home loan calculator will spit out a gross savings figure that looks impressive. What it will not show you is the real cost of switching, which means the estimate is almost always over-optimistic.

If you have been searching for a refinance home loan calculator Australia borrowers can actually trust, ASIC's Moneysmart mortgage switching calculator is one of the few independent tools that models all three outputs: whether you will save money, how long it takes to recover switching costs, and whether making higher repayments on your current loan might work just as well. Bank-owned calculators from the likes of CommBank, Westpac, ING, and Macquarie pre-populate their own rates. They are sales tools, not decision tools.

This guide, put together by Stryve Finance, a Sydney-based mortgage broker, takes a different approach. We walk through three real-number scenarios, a 5-year savings table, and a break-even framework so you can make a genuinely informed decision about whether refinancing your home loan stacks up.

What refinancing actually costs in Australia

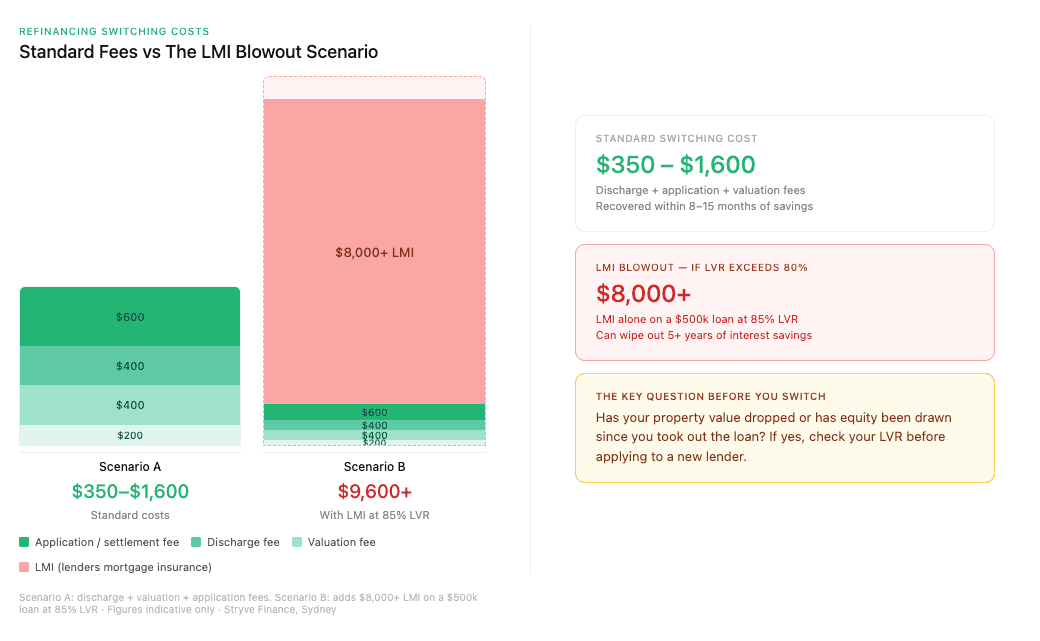

Before you calculate refinance home loan savings, you need to know what switching actually costs. Most borrowers underestimate this, and it changes the maths significantly.

The chart below shows exactly how quickly LMI reshapes the cost picture, and why it is the number you must check before anything else.

With those costs in mind, the next step is working out how long it takes to recover them, which is where the break-even formula comes in.

Here are the core cost categories identified by Moneysmart:

- Discharge fee (old lender): $150 to $400

- Application or settlement fee (new lender): $0 to $600

- Valuation fee (new lender): $200 to $600

- Ongoing fee differences: your new loan may have higher or lower annual or monthly fees

That adds up to roughly $350 to $1,600 in direct switching costs for a straightforward refinance. But there is one cost that can blow the entire calculation apart.

Lenders Mortgage Insurance (LMI) may apply if your loan-to-value ratio (LVR) has crept above 80% with the new lender. LMI protects the lender, not you, and it is not cheap. On a $500,000 loan at 85% LVR, you could be looking at $8,000 or more in LMI. That single cost can wipe out years of interest savings. See our guide to what LMI actually costs and when it applies for the full picture.

One more thing. Under the National Consumer Credit Protection Act, lenders must display a comparison rate alongside the headline rate. The comparison rate folds in fees and gives you a truer picture of the loan's cost. Always use the comparison rate, not the headline rate, when calculating your potential savings. One important caveat: ASIC calculates comparison rates on a standardised $150,000 loan over 25 years, so the figure may not perfectly reflect costs on much larger loans or shorter terms. Treat it as a guide, not a precise quote for your specific situation.

For a detailed breakdown specific to your situation, see the switching costs you need to factor in.

How to calculate your refinance break-even point

Every refinance decision comes down to one number: the break-even month. This is the point where your cumulative monthly savings overtake the upfront costs of switching.

The formula is simple:

The refinance break-even formula

Total switching costs ÷ gross monthly savings = break-even point (in months)

Say your switching costs are $1,200 and your new loan saves you $150 per month. That is $1,200 ÷ $150 = 8 months to break even.

Why does this matter? If you plan to sell your property or refinance again before you hit that break-even month, you lose money on the switch. The savings have not had enough time to offset the costs.

Keep this formula in mind as you read through the scenarios below. It is the lens we apply to every set of numbers.

Three refinance scenarios with full numbers

The best way to understand how much you could save refinancing is to see worked examples. These use standard amortisation at realistic market rates available across 50+ lenders, not a single bank's product shelf. If you want to see how lenders compare before diving in, visit our home loan comparison page.

To follow along with your own loan, you will need three figures: your current payout balance (call your lender), your remaining loan term, and the comparison rate on the new loan (found on the lender's key facts sheet).

Scenario 1: the moderate saver

- Loan balance: $600,000

- Remaining term: 25 years

- Current rate: 6.20%

- New rate: 5.90% (0.30% drop)

| Metric | Value |

|---|---|

| Old monthly repayment | $3,951 |

| New monthly repayment | $3,840 |

| Monthly saving | $111 |

| Annual saving | $1,332 |

| 5-year gross saving | $6,660 |

| Estimated switching costs | $1,500 |

| 5-year net saving | $5,160 |

| Break-even month | 14 months |

A 0.30% rate drop does not sound dramatic, but on a $600,000 balance it delivers over $5,000 in net savings across five years. You can model your new repayment amount to see the post-refinance figure for your specific loan.

Ready to check your own numbers? Plug your own numbers into the refinance calculator and see your personalised savings estimate.

Scenario 2: the big mover

- Loan balance: $400,000

- Remaining term: 20 years

- Current rate: 6.50%

- New rate: 5.70% (0.80% drop)

| Metric | Value |

|---|---|

| Old monthly repayment | $2,982 |

| New monthly repayment | $2,789 |

| Monthly saving | $193 |

| Annual saving | $2,316 |

| 5-year gross saving | $11,580 |

| Estimated switching costs | $1,200 |

| 5-year net saving | $10,380 |

| Break-even month | 7 months |

A larger rate gap on a smaller loan still delivers strong savings. The break-even is just seven months, meaning you are in the clear quickly.

What about cashback offers? If the new lender offers a $3,000 cashback, your net switching costs drop from $1,200 to effectively negative $1,800. You are ahead from day one. Cashback deals change regularly, so check how cashback offers affect your savings calculation before you commit.

Plug your own numbers into the refinance calculator to see where you land.

Scenario 3: the high-balance refinancer

- Loan balance: $1,000,000

- Remaining term: 25 years

- Current rate: 6.00%

- New rate: 5.85% (0.15% drop)

| Metric | Value |

|---|---|

| Old monthly repayment | $6,443 |

| New monthly repayment | $6,352 |

| Monthly saving | $91 |

| Annual saving | $1,092 |

| 5-year gross saving | $5,460 |

| Estimated switching costs | $2,500 |

| 5-year net saving | $2,960 |

| Break-even month | 28 months |

Even a 0.15% drop on a million-dollar loan produces meaningful monthly savings. But the break-even stretches to 28 months because switching costs are higher at this level. A higher valuation fee and the risk of triggering LMI on a large balance both push costs up.

Plug your own numbers into the refinance calculator to see your personalised result.

How much could you save over five years?

This mortgage refinance calculator comparison table lets you scan for a scenario that matches your situation. All figures assume principal-and-interest repayments over 25 years using standard amortisation.

| Loan balance | Rate drop | Monthly saving | 5-year gross saving | Est. switching costs | 5-year net saving | Break-even month |

|---|---|---|---|---|---|---|

| $400,000 | 0.30% | $74 | $4,440 | $1,200 | $3,240 | 17 |

| $400,000 | 0.80% | $193 | $11,580 | $1,200 | $10,380 | 7 |

| $600,000 | 0.30% | $111 | $6,660 | $1,500 | $5,160 | 14 |

| $600,000 | 0.80% | $290 | $17,400 | $1,500 | $15,900 | 6 |

| $1,000,000 | 0.30% | $185 | $11,100 | $2,500 | $8,600 | 14 |

| $1,000,000 | 0.80% | $483 | $28,980 | $2,500 | $26,480 | 6 |

These are indicative figures. Your actual savings depend on your loan structure, fees, and the comparison rate offered to you. A refinance savings calculator gives you a ballpark, but your specific numbers will differ. Run the numbers for your exact loan and get a personalised result.

When you should not refinance your home loan

Honesty matters here. Refinancing is not the right move for everyone.

- You are near the end of your loan term: If you have five years left on a $200,000 balance, the interest savings from a small rate drop are minimal. Switching costs may never be recovered.

- Your LVR has crept above 80%: If property values have dipped or you have drawn on your equity, refinancing to a new lender could trigger LMI. On a large loan, that cost alone can eliminate years of savings.

- You are on a fixed rate with high break costs: Breaking a fixed-rate loan early often incurs a break fee that dwarfs any savings from a lower variable rate. See our fixed rate home loan guide for help calculating whether breaking your fixed rate is worth it.

In all three cases, Moneysmart notes that making higher repayments on your current loan can sometimes deliver equivalent or better outcomes than switching. On a $600,000 loan at 6.20% over 25 years, an extra $200 per month shaves around 2.5 years off the loan term and saves approximately $72,000 in total interest over the life of the loan.

Not sure refinancing is right for you? Try the extra repayment calculator to see if paying more on your current loan gets you a better result, or read our full guide on how to pay off your mortgage faster.

How to evaluate a refinance offer beyond the interest rate

Now that you have a savings target, the next step is finding the right offer. The lowest headline rate is not always the best deal.

Always compare on the comparison rate, not the advertised rate. The comparison rate includes fees and gives you a truer cost under ASIC's requirements. For a deeper explanation of how comparison rates work, read our guide on comparison rates on home loans. Beyond the rate, look at ongoing fees, offset and redraw features, and loan flexibility like the ability to make extra repayments without penalty.

For a full walkthrough, read our guide on how to compare refinance offers beyond the headline rate.

What a Stryve Finance does that no calculator can

A home loan refinance calculator gives you an estimate. A broker gives you a real comparison sheet with actual rates you qualify for, drawn from 50+ lenders. If you want to understand the full value of using a broker, read our guide on why Australians use a mortgage broker.

That matters because rate is only part of the equation. A broker understands each lender's credit policies, which affects whether you actually get approved. They know which lenders are offering cashback deals this month. And they manage the entire application from start to settlement, so you are not chasing paperwork across two lenders.

Stryve Finance, a Sydney-based mortgage broker, offers full lender commission transparency and charges no hidden fees. You see exactly what we earn and from whom. You can explore our refinancing home loan service to understand what we do before booking a call.

The calculator showed you the potential. The next step is finding out what is actually available for your loan.

Talk to a Stryve Finance broker and get a real comparison sheet with live rates from 50+ lenders, tailored to your loan.

Frequently Asked Questions About Refinance Savings

How much can I save by refinancing my home loan?

Your savings depend on your loan balance, remaining term, and the rate difference between your current and new loan. A 0.30% rate drop on a $600,000 loan can save around $111 per month, or over $5,000 net over five years after switching costs. Use a refinance savings calculator to get a figure specific to your situation. If you are still deciding whether to act, our guide on whether to refinance your home loan in 2026 covers the decision framework in full.

What does refinancing cost in Australia?

Typical switching costs include a discharge fee ($150 to $400), application or settlement fee ($0 to $600), and valuation fee ($200 to $600). If your LVR exceeds 80% with the new lender, you may also need to pay LMI, which can cost thousands. See our full breakdown of refinancing costs for details.

How long does refinancing take?

Most refinances settle within four to six weeks from application, though timelines vary by lender. Having your documents ready, including payslips, bank statements, and your current loan payout figure, helps speed up the process. For a step-by-step overview, see our guide on from approval to settlement.

Will I have to pay LMI again if I refinance?

You may need to pay LMI again if your LVR exceeds 80% with the new lender. LMI from your original loan does not transfer. On a $500,000 loan at 85% LVR, LMI could cost $8,000 or more, which can eliminate years of interest savings. Check your current LVR before applying.

Should I use a broker or go direct to a lender?

A broker compares rates and policies across 50+ lenders, giving you a broader view than any single bank can offer. They also handle the application process and can negotiate cashback offers on your behalf. Stryve Finance, a Sydney-based mortgage broker, offers full commission transparency so you know exactly how we are paid.

Is it better to refinance or make extra repayments?

Both strategies can work, and often the best answer is to combine them. On a $600,000 loan at 6.20% over 25 years, refinancing to 5.90% saves around $111 per month, or about $5,160 over five years after switching costs. Adding an extra $200 per month to your current loan saves around $72,000 in total interest over the life of the loan and pays it off roughly 2.5 years earlier. If switching costs are high, your remaining term is short, or your LVR has crept above 80%, extra repayments usually deliver better value. If your rate is materially above market and your situation is straightforward, refinancing wins. A Stryve Finance broker can model both paths against your specific numbers.

Dylan Bertovic is the Director and Senior Finance Broker at Stryve Finance, specialising in non-traditional lending solutions. He helps clients across Australia with tiny home loans, construction finance, equipment and asset lending, refinancing, and investor loans. With deep expertise in self-employed and renovation mortgages, Dylan is known for crafting tailored strategies that get results