Cashback refinance has hit peak search interest this month. But here's the thing: home loan cashback offers are already declining, down 8% as lenders quietly pull promotions in the wake of the February 2026 RBA rate rise.

It makes sense when you understand why lenders offered cashback in the first place. In a low-rate environment where margins were razor-thin, lenders competed aggressively for refinancers. A $2,000 to $4,000 sweetener was a cheap way to win a loan book that would generate interest income for decades. Now that rates have shifted, the economics have changed. Lenders don't need to buy your business quite as hard.

So let's be clear about what this piece is and isn't. This isn't a cheerful listicle telling you to grab free money. Cashback is not free money. It's a strategic tool to offset switching costs, and ASIC's MoneySmart guidance is explicit: cashback must be assessed as part of the total cost of the loan, not in isolation.

The window to use this tool effectively is genuinely narrowing. Here's what's still available, what it's actually worth, and how to avoid the traps.

Current Home Loan Cashback Offers

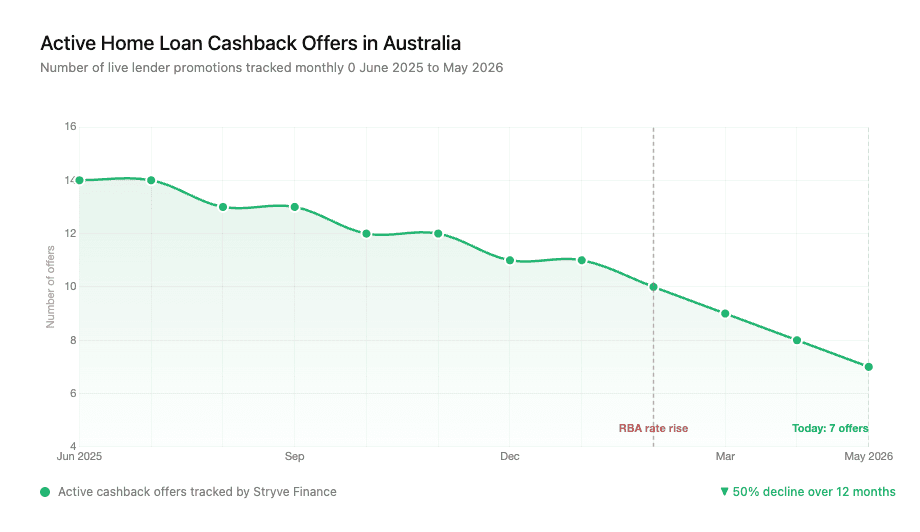

We verify these offers monthly. The number of live cashback home loan offers has dropped noticeably over the past quarter. Three months ago, we tracked 10 or more active promotions. Today, we're down to the following.

The chart below tracks how many home loan cashback offers were active each month over the past year, and the direction is unmistakable.

The seven offers that remain are listed below, along with the exact terms, deadlines, and clawback periods you need to check before you apply.

Here are the refinance cashback offers still available in May 2026. All LVR (loan-to-value ratio) figures refer to the maximum ratio of your loan balance to property value required to qualify.

| Lender | Cashback amount | Min. loan size | LVR (loan-to-value ratio) requirement | Settlement deadline | Clawback period | OO / Investor |

|---|---|---|---|---|---|---|

| ANZ | $4,000 | $250,000 | ≤ 80% | 31 Jul 2026 | 24 months | Both |

| Macquarie Bank | $3,000 | $500,000 | ≤ 80% | 30 Jun 2026 | 12 months | OO only |

| ING | $3,000 | $500,000 | ≤ 80% | 31 Aug 2026 | 24 months | Both |

| Suncorp | $2,000 | $250,000 | ≤ 80% | 30 Jun 2026 | 12 months | OO only |

| St George | $2,000 | $250,000 | ≤ 80% | 30 Jun 2026 | 18 months | Both |

| Bank of Melbourne | $2,000 | $250,000 | ≤ 80% | 30 Jun 2026 | 18 months | Both |

| Bankwest | $2,000 | $200,000 | ≤ 80% | 31 Jul 2026 | 12 months | OO only |

The trend is clear: fewer offers, tighter deadlines, and shorter settlement windows. Under the Australian Banking Association's Banking Code of Practice, all cashback terms and clawback provisions must be disclosed before settlement. Always confirm the fine print directly with the lender or your broker.

ANZ Cashback vs Westpac Cashback

ANZ's cashback refinance offer is the standout right now. Search interest for ANZ refinance cashback is up 20%, and for good reason. ANZ is offering $4,000 on loans of $250,000 or more, available to both owner-occupiers and investors, with a settlement deadline of 31 July 2026. The clawback period is 24 months, which is on the longer side.

Westpac's cashback tells a different story. Search interest has dropped 20%, and the offer has been scaled back significantly. At the time of writing, Westpac's cashback home loan promotion is either paused or limited to very narrow eligibility windows. That decline in visibility usually signals a lender preparing to exit the cashback space entirely.

But here's what matters more than the headline number: the ongoing rate. A $4,000 cashback from ANZ means nothing if their variable rate is 0.25% higher than a lender offering no cashback at all. When you compare against current refinance rates for 2026, the net picture can look very different.

Under ASIC Regulatory Guide 273, brokers must document why a recommended cashback loan is in the client's best interests compared to alternatives. That means the comparison has to go beyond the cashback headline.

Are home loan cashback offers actually worth it?

This is where most articles fall short. They list the offers but never show you the maths. Let's fix that.

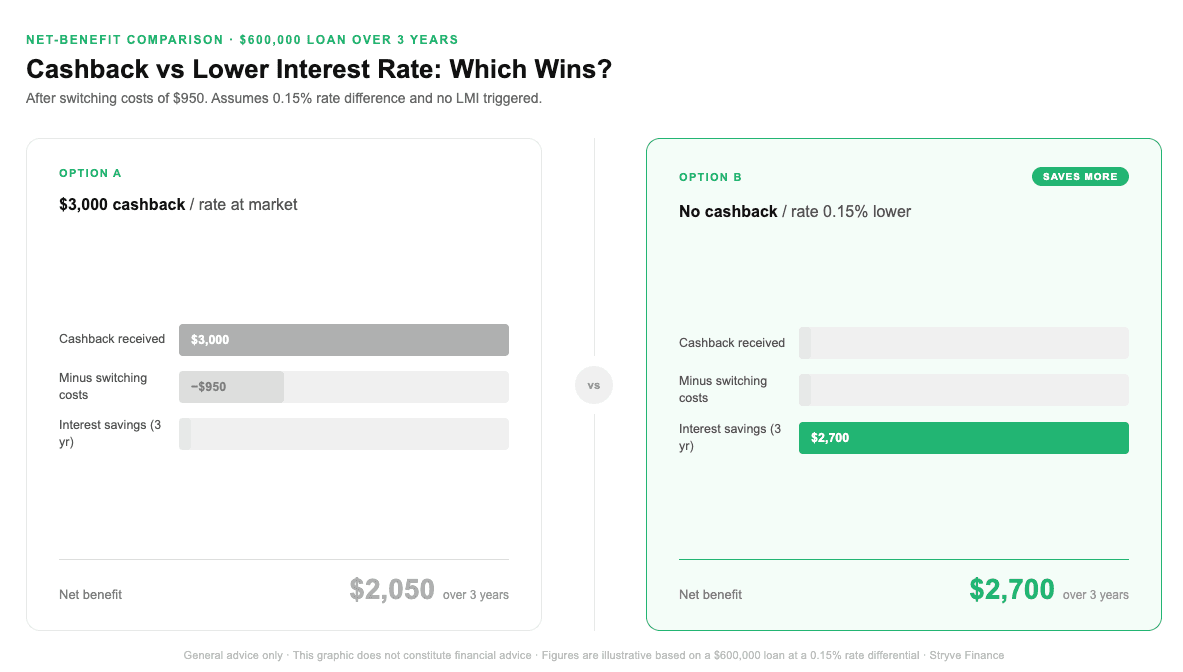

Worked example: $600,000 loan, $3,000 cashback

Here are your switching costs:

- Discharge fee from current lender: $350 (variable rate loans typically cost $150 to $400)

- Application fee at new lender: $600

- LMI (Lenders Mortgage Insurance): $0, assuming your loan-to-value ratio (LVR) stays under 80%

Net cashback benefit: $3,000 - $350 - $600 = $2,050.

That looks decent. But now compare it against a lender offering no cashback but a rate that's 0.15% lower.

On a $600,000 loan, 0.15% saves you roughly $900 per year. Over three years, that's $2,700 in interest savings, beating the $2,050 net cashback.

Now flip it. What if the cashback lender's rate is 0.30% higher than the best available rate? That costs you roughly $1,800 per year, or $5,400 over three years. Your $3,000 cashback just cost you $2,400.

The numbers tell a clear story. Here's what the same $600,000 loan looks like when you compare a $3,000 cashback deal against a lender offering no cashback but a rate just 0.15% lower.

As the comparison shows, a marginally better rate compounds quietly over three years and outpaces the upfront cashback, which is why the ongoing rate, not the headline dollar figure, should drive your decision.

The takeaway: a cashback home loan offer is only worth it when the ongoing rate is competitive with or better than alternatives. The cashback covers your switching costs. It doesn't compensate for a bad rate.

One critical trap: if your property value has declined since you bought, your LVR might now exceed 80%. That means LMI could be triggered on the new loan, potentially costing thousands and wiping out any cashback benefit entirely.

See our guide. And to plug in your own numbers with our refinance savings calculator, run the scenario for your specific loan.

Don't Chase Cashback at the Expense of a Bad Deal

It's easy to get tunnel vision on a $4,000 number. But a higher ongoing rate, restrictive loan features, or poor serviceability can cost far more than the cashback saves.

Watch for loans that come with no offset account, no ability to make extra repayments, or annual fees that quietly erode the benefit. Some cashback home loans are attached to basic products stripped of the features that give you flexibility.

This is exactly where a broker earns their keep. A broker doesn't just compare cashback amounts. They stack the cashback against the rate, the fees, and the loan features across dozens of lenders to find the actual best deal.

At Stryve Finance, a Sydney-based mortgage broker, we compare across 50+ lenders in one conversation, with full lender commission transparency. There's no hidden incentive to push one cashback offer over another.

Under ASIC Regulatory Guide 273, brokers are legally required under the best interests duty to recommend the loan that's genuinely in your favour overall, not simply the one with the biggest cashback headline.

Eligibility Traps That Could Cost You the Cashback

You find a great cashback refinance offer, you apply, you settle. Then three months later, you realise you don't qualify. Or worse, you have to pay it back. Here are the conditions most borrowers miss.

- LVR thresholds: Most offers require your LVR (loan-to-value ratio) to be 80% or below. If your property value has dropped, you might not meet this even if you did when you first bought.

- Minimum loan size: Ranges from $200,000 to $500,000 depending on the lender. Check before you apply.

- Owner-occupier vs investor restrictions: Several offers are owner-occupier only. Mum and dad investors need to read the fine print carefully.

- Settlement window deadlines: Most offers require settlement by a specific date. Miss it by a day and the cashback disappears.

- New-customer-only exclusions: If you already hold a product with the lender, you may not qualify.

- Clawback clauses: This is the big one. Most lenders require the loan to stay open for 12 to 24 months. Close it early, whether you refinance again or sell, and you repay the full cashback amount.

Under ASIC's responsible lending obligations (NCCP Act), lenders must still assess whether the new loan is “not unsuitable” for you. Switching purely for cashback doesn't bypass this assessment. If your financial situation has changed, you may not be approved regardless of the offer.

Frequently Asked Questions About Home Loan Cashback

Is cashback on a home loan taxable in Australia?

Generally, no. The ATO treats cashback payments on refinancing as a reduction in borrowing costs, not assessable income. However, if you're using the loan for investment purposes, you should confirm the tax treatment with a qualified tax adviser, as it may affect your deductible interest calculations.

Which banks are offering cashback on home loans in 2026?

As of May 2026, active offers include ANZ, Macquarie Bank, ING, Suncorp, St George, Bank of Melbourne, and Bankwest. The list is shrinking. Check the comparison table above for current terms, and note that offers can be withdrawn at any time.

How long does cashback take to be paid?

Most lenders pay cashback within 60 to 90 days of settlement. Some are faster, some slower. Your broker can confirm the expected timeline for each lender before you commit.

Can I keep cashback if I refinance again?

Only if you've held the loan past the clawback period, which is typically 12 to 24 months depending on the lender. If you close the loan before that period ends, you'll need to repay the cashback in full.

Cashback vs lower interest rate: which saves more?

It depends on your loan size and how long you hold the loan. On a $600,000 loan, a $3,000 cashback nets roughly $2,050 after switching costs. A lender with no cashback but a rate just 0.15% lower saves $2,700 in interest over three years, more than the cashback. If the cashback lender's rate is 0.30% higher, the cashback costs you $2,400 over three years after accounting for the upfront payment. The cashback wins only when the ongoing rate is competitive. Use the net-benefit formula above to run your own numbers, or speak to a Stryve Finance broker who can compare both scenarios across 50+ lenders.

General advice warning

This article provides general information only and does not constitute financial or credit advice. It does not take into account your personal objectives, financial situation, or needs. Before acting on any information in this article, consider its appropriateness to your circumstances and speak to a qualified mortgage broker or financial adviser.

Let a Stryve Finance broker find the best cashback deal for your situation

The cashback window is narrowing. Offers that were live last month are gone. The ones still standing have tighter deadlines and stricter conditions.

A Stryve Finance broker can check your live cashback eligibility across 50+ lenders in one conversation. No chasing individual bank websites. No hidden fees. Full transparency on lender commissions so you know the recommendation is genuinely in your interest.

If you're thinking about refinancing, now is the time to run the numbers. Refinance your home loan with a broker who'll show you whether cashback is worth it for your specific loan, or whether a better rate without cashback puts more money in your pocket over the long run.

Talk to a Stryve Finance broker to see which cashback offers you actually qualify for, and whether they're worth it for your loan.

Dylan Bertovic is the Director and Senior Finance Broker at Stryve Finance, specialising in non-traditional lending solutions. He helps clients across Australia with tiny home loans, construction finance, equipment and asset lending, refinancing, and investor loans. With deep expertise in self-employed and renovation mortgages, Dylan is known for crafting tailored strategies that get results