The Reserve Bank of Australia (RBA) cut the cash rate in February 2026, and lenders responded fast. Major banks including ING, NAB, and Commonwealth Bank repriced their fixed-rate home loan products within 48 hours. If you've been watching the news and wondering what this means for your mortgage, you're not alone.

Search data backs this up. According to Google Trends data, Australian searches for fixed-rate home loan comparisons have more than doubled since the February 2026 RBA decision, with queries for best home loan rates reaching a 12-month high. People are actively trying to figure out whether now is the time to lock in.

This Stryve Finance guide won't push you toward a product. It will walk you through how fixed-rate home loans work, the genuine pros and cons, and a simple framework to help you decide what makes sense for your situation.

How Fixed-Rate Home Loans Actually Work

What is a fixed rate home loan?

A fixed-rate home loan locks in your interest rate for a set period, typically between 1 and 5 years in Australia, so your repayments stay the same regardless of RBA rate changes. At the end of the fixed term, the loan reverts to the lender's standard variable rate unless you renegotiate.

A fixed-rate home loan locks in your interest rate for a set period, typically between 1 and 5 years in Australia. During that time, your repayments stay the same regardless of what the RBA does. When the fixed term ends, your loan usually reverts to the lender's standard variable rate unless you renegotiate.

A variable home loan moves with the market. When variable home loan rates go up, your repayments increase. When they drop, you pay less.

One thing to watch is the comparison rate. According to ASIC MoneySmart, the comparison rate includes fees and charges to give you a truer picture of the loan's total cost. The advertised fixed rate is not the full story. Always check the comparison rate and the revert rate before committing.

Fixed vs Variable: A Side-by-Side Comparison

Neither option is universally better. It depends on your circumstances. Here's how they stack up across the factors that matter most.

| Feature | Fixed rate | Variable rate |

|---|---|---|

| Repayment certainty | Repayments stay the same for the fixed term | Repayments move up or down with RBA changes |

| Offset account access | Rarely available, or only partial offset offered | Full offset accounts are standard |

| Extra repayments | Capped at $10,000 to $20,000 per year before fees apply | Unlimited extra repayments with most lenders |

| Impact of RBA rate changes | No impact during the fixed term | Direct impact on your repayments |

| Break costs | Apply if you exit early (sell, refinance, or switch) | No break costs |

| Revert rate risk | Reverts to standard variable at end of term, often higher than competitive rates | No revert rate to manage |

Want to dig deeper into how to compare home loans beyond just the rate? We break it down here.

The Honest Pros and Cons of Fixing Your Rate in 2026

Pros of fixing

- Budget certainty. You know exactly what your repayments will be for the fixed term. No surprises.

- Protection from further hikes. If the RBA raises rates again, your repayments don't change.

- Peace of mind. For first home buyers on tight budgets, predictability can reduce genuine financial stress.

Cons of fixing

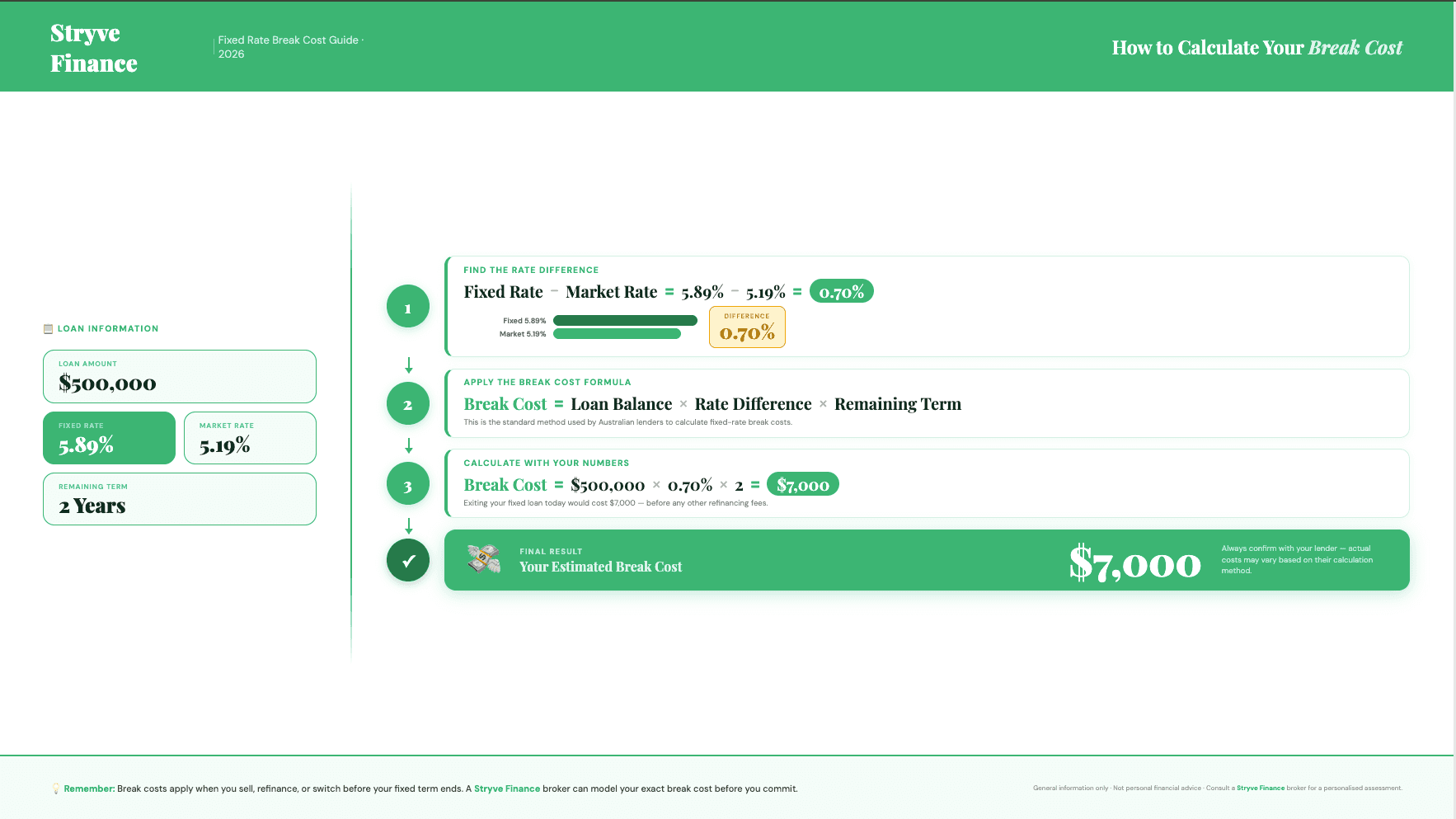

- Breakdown costs can be high. These are not a flat fee. ASIC MoneySmart explains that break costs are calculated based on the difference between your fixed rate and the current rate, multiplied by the remaining term and your loan balance.

- You miss out if rates drop. You stay locked in at your fixed rate regardless.

- Limited flexibility. Extra repayment caps and restricted offset access reduce your ability to manage cash flow.

- Revert rate shock. When the fixed term ends, you land on the lender's standard variable rate, which is typically 0.5% to 1.2% higher than the best variable rates available on the open market.

A worked example of break costs:

Say you fixed at 5.89% for three years on a $500,000 loan. One year in, the market rate drops to 5.19%. The lender calculates the 0.70% difference across your remaining two years and loan balance. That break cost could reach $7,000 or more on a typical loan. This is why it's critical to understand the scenarios before you sign.

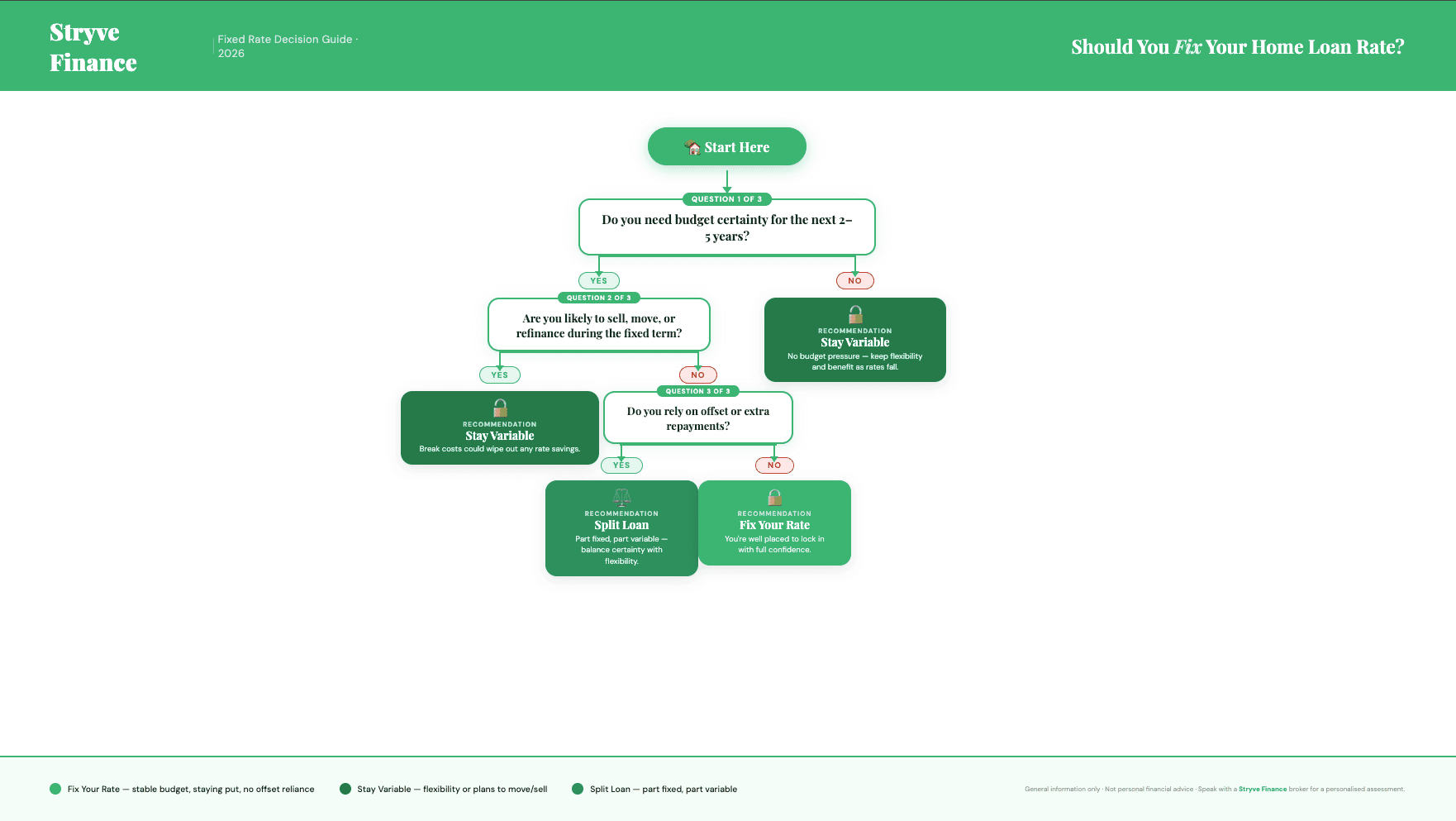

A Simple Framework to Decide: Should You Fix or Stay Variable?

Forget trying to predict what the RBA will do next. Base your decision on your own circumstances. Ask yourself three questions.

1. Do you need budget certainty for the next two to five years? If your household budget has little room for increases in repayment, fixing gives you a known number to plan around.

2. Are you likely to sell, move, or refinance during the fixed term? If there's a reasonable chance your circumstances will change, break costs could wipe out any savings from fixing.

3. Do you rely on offset or extra repayments tomanage cash flow? If you regularly park money in an offset account or make lump sum payments, a fixed loan's restrictions may cost you more than the rate certainty saves.

Scenario 1: First home buyer on a tight budget who plans to stay put for three or more years. Fixing could make sense for predictable repayments.

Scenario 2: Refinancer with strong equity who wants flexibility to make extra repayments or access an offset. A variable or a split loan (part fixed, part variable) might suit better. Split loans are available with most Australian lenders and offer a middle ground.

Scenario 3: Mum and Dad investor focused on cash flow certainty. Fixing a portion of the loan can help with forecasting rental yield. Note that Interest Only (IO) fixed terms are more common for investors, while Principal and Interest (P&I) structures are standard for owner-occupiers.

Your LVR (loan-to-value ratio), which is the size of your loan compared to the property's value, affects the rates you're offered on both fixed and variable products. A lower LVR generally unlocks better pricing.

Not sure which scenario fits you?

A broker can model your options in 15 minutes, comparing fixed, variable, and split loan scenarios based on your actual numbers. It's free, and there's no obligation.

Fixed Rate Home Loans and First Home Buyers: What You Need to Know

If you're buying your first home, you've got specific questions. Here are the answers.

Can you use the FHLDS with a fixed-rate loan? The First Home Loan Deposit Scheme (FHLDS)allows eligible first home buyers to purchase with as little as 5% deposit without paying

LMI (Lenders Mortgage Insurance). Yes, you can use it with a fixed-rate loan, but availability depends on the lender.

What about the FHOG? The First Home Owner Grant (FHOG) varies by state and territory. It's a one-off grant, not a rate product, but it affects your deposit position, which influences your LVR and the rates you're offered.

What if you need to sell during the fixed term? Break costs will apply. A broker can model these scenarios before you commit, so you know the potential cost upfront. LMI is typically required when your LVR exceeds 80%. On a $600,000 property with a 10% deposit, LMI can add $8,000 to $15,000 to your upfront costs. This applies to both fixed and variable loans.

At Stryve Finance, we help first home buyers navigate these schemes every day. Explore your first home buyer loan options here.

How to Lock in a Fixed Rate (and what to watch for)

The rate you see advertised today is not guaranteed at settlement. Without a rate lock, your fixed rate is set at the date of settlement, not the date you apply. If rates move in between, you could end up with a different rate than you expected.

What is a rate lock? It's a commitment from the lender to hold a specific fixed rate for you during the period between application and settlement. In Australia, rate lock periods are typically 60 to 90 days.

Rate lock fees usually apply. Expect a one-off cost of around 0.10% to 0.15% of the loan amount. On a $500,000 loan, that's typically a one-off cost of $500 to $750.

The timeline matters. From application to settlement typically takes 4 to 6 weeks in Australia. If you're buying at auction or in a competitive market, the gap between approval and settlement is when rates can shift.

A Stryve Finance broker with access to 40 or more lenders can compare rate lock terms, fees, and fixed rate products across the market, not just the headline rate from one or two banks.

What about ING, NAB, and other lender fixed rates?

Searches for specific lender products are surging. According to Google Trends data, searches for specific lender fixed rate products rose by over 50% in the two weeks following the RBA's February 2026 decision. It makes sense that people want to compare specific offers.

But comparing individual lender rates in isolation is risky. Comparison rates, fee structures, offset availability, and revert rates vary among lenders. A rate that looks sharp on the surface can cost more over the life of the loan once you factor in the full picture.

This is where Stryve Finance adds value. Rather than comparing two or three banks yourself, our brokers compare across 40 or more lenders with full commission transparency. They disclose exactly what they earn from each lender. Stryve Finance broker services are free for borrowers.

Frequently Asked Questions about Fixed-Rate Home Loans

What happens if rates drop after I fix?

You stay on your fixed rate. That's the trade-off for certainty. You can refinance, but break costs will apply when you exit a fixed loan early.

What if I need to sell my property during the fixed term?

Break costs apply whether you sell, refinance, or switch. A broker can estimate these before you commit, so there are no surprises.

Can I make extra repayments on a fixed-rate loan?

Usually yes, but capped at typically $10,000 to $20,000 per year, depending on the lender. Exceeding the cap triggers fees. Always check the product terms.

Fixed rate vs split loan: which is better?

A fully fixed loan gives maximum repayment certainty but restricts extra repayments and usually eliminates offset access. A split loan divides your borrowing between a fixed and a variable portion. You get rate certainty on the fixed part while retaining flexibility (offset account, unlimited extra repayments) on the variable part. If you value flexibility but want some protection from rate rises, a split is often a better fit than fixing 100% of the loan. Most Australian lenders offer split structures.

Can self-employed borrowers get fixed-rate loans?

Yes. It's about documentation, not loan type. Brokers who specialise in self-employed applicants can guide you through the requirements.

Not sure whether to fix? Here's your next step

There's no universally right answer to the fixed vs variable question. The best fixed-rate home loan for you depends on your budget, your plans, and your appetite for rate movement. Stryve Finance brokers specialise in helping Australians cut through the noise and make the right call for their situation.

At Stryve Finance, our brokers don't push a product. They model scenarios based on your situation, compare across 50+ lenders, and show you exactly what they earn from each one. Full transparency, no hidden fees.

Talk to a Stryve Finance broker about your fixed rate options.

General information disclaimer: This guide provides general information only and does not constitute personal financial advice. The information has been prepared without taking into account your personal objectives, financial situation, or needs. Consider your own circumstances and seek independent financial advice from a licensed professional before making any financial decisions.

Dylan Bertovic is the Director and Senior Finance Broker at Stryve Finance, specialising in non-traditional lending solutions. He helps clients across Australia with tiny home loans, construction finance, equipment and asset lending, refinancing, and investor loans. With deep expertise in self-employed and renovation mortgages, Dylan is known for crafting tailored strategies that get results