Buying your first home is exciting. It can also feel overwhelming. There is a lot of jargon, a lot of paperwork, and a genuine fear of making an expensive mistake. This first-home buyer checklist is built specifically for 2026 because the rules have changed, and the broker team at Stryve Finance helps first-home buyers navigate every step.

The problem with most first-home buyer guides floating around online is that they were written for a different year. Generic checklists miss the policy changes that directly affect your deposit, your eligibility, and your borrowing power. In 2026, the Help to Buy scheme and the expanded First Home Guarantee have shifted the goalposts. If your checklist does not reference these, it could cost you money or time you do not have.

According to the Australian Bureau of Statistics, first-home buyer loan commitments rose 6.8% in the December quarter of 2025 alone (up 9.1% through the year), the largest quarterly rise since late 2023. Search interest in first home buyer guidance has surged heading into 2026. Plenty of people are looking for current, reliable information and not finding it.

This is your start-here page. Each step below links to deeper guides so you can go further when you are ready, without ever feeling lost.

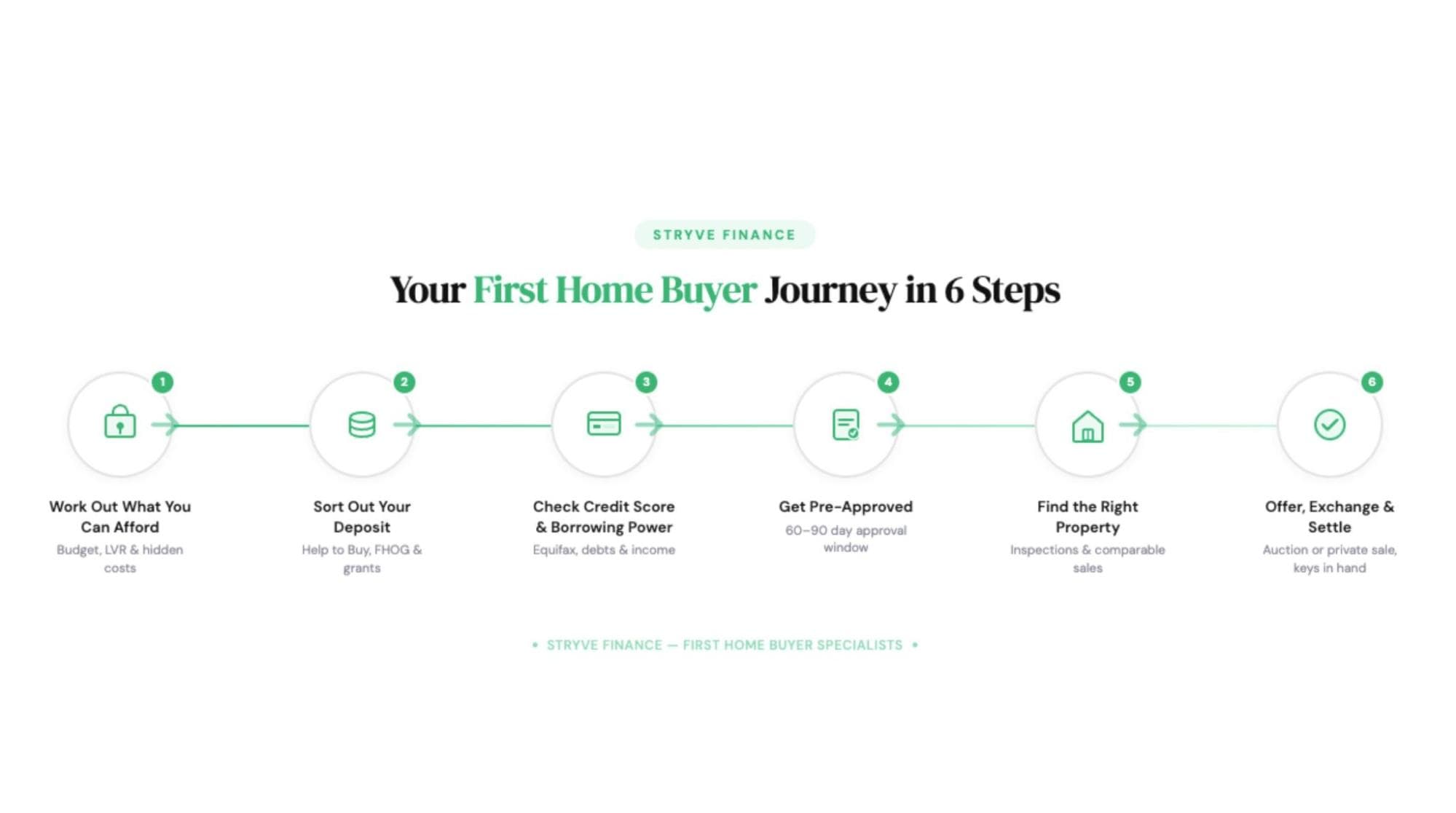

Step 1: Work Out What You Can Actually Afford

Before you browse a single listing, you need a realistic number. Not a dream number. A number that accounts for everything you will actually pay.

Your budget is not just the purchase price. According to Moneysmart, you need to factor in stamp duty, conveyancing fees, building and pest inspections, loan application fees, and ongoing costs like council rates, insurance, and maintenance. These extras can add tens of thousands of dollars to the purchase price.

Two terms you will hear constantly: LVR (loan-to-value ratio) is the percentage of the property's value you are borrowing. LMI (Lenders Mortgage Insurance) is a one-off cost you pay if your LVR is above 80%, meaning your deposit is less than 20%. LMI protects the lender, not you, but it comes out of your pocket.

The 2026 interest rate environment directly affects how much a lender will lend you. With the RBA cash rate at 3.85% as of February 2026, up from 3.60% following the February rate hike, borrowing capacity is tighter than it was 12 months ago. Even small rate changes can affect your borrowing capacity by tens of thousands of dollars. According to ABS data, the average first-home buyer loan reached a record of $607,624 in the December quarter of 2025. Research comparable property sale prices in your target area before you set a budget so your expectations align with reality. The Stryve Finance team can run a borrowing capacity assessment using current lender criteria before you commit to a number.

Common roadblock

Your borrowing capacity comes back lower than expected. This happens more often than you think, especially when rates are higher. Do not panic. A broker can assess your situation across multiple lenders, because each one calculates capacity differently. Reducing existing debts or lowering credit card limits before you apply can also make a meaningful difference.

Step 2: Sort Out Your Deposit (It might be less than you think)

The traditional benchmark is a 20% deposit. That figure exists because it lets you avoid paying LMI, which is a significant saving. But for a $600,000 property, 20% means $120,000 in cash. For many first home buyers, that number feels impossible.

Here is where 2026 policy changes work in your favour.

The Help to Buy scheme is a shared equity arrangement where the government contributes a portion of the purchase price (up to 40% for new homes, 30% for existing homes). This means you need a smaller deposit and a smaller loan. Eligibility is based on income caps and property price thresholds, and you must be an Australian citizen who does not currently own property.

The expanded First Home Guarantee allows eligible buyers to purchase with as little as a 5% deposit and pay no LMI. The government guarantees the remaining portion up to 80% LVR. In 2026, price caps and available places were updated, so check the current limits for your state. Your state matters here. In NSW, first-home buyers can access stamp duty exemptions for properties up to certain thresholds, with concessions available above those thresholds.

In Victoria, the FHOG (First Home Owner Grant), a one-off payment for eligible buyers of new homes, operates alongside separate duty concessions with different thresholds. The numbers are not the same, so a first-home buyer guide for NSW will look different from one for Victoria.

Legislative status note

The Help to Buy scheme was announced in the 2023-24 Federal Budget and reintroduced in 2024-25, with the launch delayed until late 2025. Check services.gov.au for the latest eligibility criteria and available places. For NSW-specific stamp duty exemptions. Stryve Finance brokers track these changes in real time and can confirm exactly what you qualify for today.

2026 Government Scheme Comparison

| Scheme | Scheme Type | Min. Deposit | Income Cap | States |

|---|---|---|---|---|

| Help to Buy | Shared equity (govt buys up to 40% new / 30% existing) | 2% (new) / 2% (existing) | $90k single / $120k couple | All states (check services.gov.au) |

| First Home Guarantee | Loan guarantee (no LMI on 5% deposit) | 5% | $125k single / $200k couple | All states (price caps vary by state) |

| FHOG (Vic) | Cash grant for new homes | No set minimum | No income cap | Victoria only (new homes up to price cap) |

| NSW Stamp Duty Exemption | Stamp duty waiver or concession | No set minimum | No income cap | NSW only (see revenue.nsw.gov.au) |

Step 3: Check Your Credit Score and Borrowing Power

Lenders are looking at four things: your credit score, income stability, existing debts, and living expenses. Understanding what they see helps you present the strongest possible application.

Start by checking your credit report for free through agencies like Equifax or Illion. Look for errors, old debts you have already paid, or defaults you were not aware of. Dispute anything incorrect before you apply.

Practical steps that improve your position: cancel unused credit cards or reduce their limits (lenders count the full limit as a potential debt, even if you never use it), cut unnecessary subscriptions, and avoid applying for any new credit in the months before your home loan application.

If your income is non-standard, for example, if you are self-employed or work on contract, this step is even more important. Not every lender assesses non-standard income the same way.

Common roadblock

Your credit score is lower than you expected, and you are worried about being rejected. Every rejected application can further lower your score. This is exactly why talking to a Stryve Finance broker early matters. With access to 40-plus lenders, a Stryve Finance broker can match you to a lender whose criteria suit your specific situation, rather than you guessing and risking a knock to your score.

Step 4: Get Pre-Approved Before You Start Looking

Pre-approval (sometimes called conditional approval) is a lender's written indication of how much they are willing to lend you, based on an initial assessment. It typically lasts 60 to 90 days, depending on the lender.

Why does this matter? If you plan to buy at auction, you must have finance arranged beforehand. There is no cooling-off period at auction. Without pre-approval, you are either locked out of auction properties or taking on serious financial risk.

The process involves gathering documents: payslips, tax returns, bank statements, identification, and details of your assets and liabilities. Your Stryve Finance broker submits these across their lender panel, comparing options from 40-plus lenders to find the right fit for your circumstances. Commission transparency means you will know exactly how your broker is paid.

Pre-approval is not a commitment. It does not lock you into a lender or force you to buy. It is a tool that tells you exactly where you stand so you can search with confidence, not anxiety. When you are ready to take this step, see how the pre-approval process works.

Step 5: Find the Right Property (and do your homework)

With pre-approval in hand, the search begins. Set your non-negotiables early: location, minimum bedrooms, proximity to transport or schools. Everything else is a compromise you can weigh up.

Research comparable sales in your target suburbs. Knowing what similar properties have sold for recently stops you from overpaying. Attend open inspections with a critical eye, not just an emotional one.

Two non-negotiable steps before you commit: get a professional property inspection (building and pest at minimum) and engage a conveyancer or solicitor early. Skipping either of these to save a few hundred dollars can cost you thousands in hidden defects or contract issues.

Be aware that the buying process differs by state. In Victoria, vendors must provide a Section 32 statement before sale, and cooling-off periods apply to private sales but not auctions. In NSW, the contract structure and cooling-off rules have their own requirements. If you are using a first home buyer guide for Victoria, do not assume the same rules apply in NSW, and vice versa.

Step 6: Make Your Offer, Exchange, and Settle

You have found the property. Now you either make an offer through private sale or bid at auction. If buying at auction, your pre-approval is essential because the fall of the hammer creates a binding contract.

Once your offer is accepted (or you win at auction), contracts are exchanged. Settlement typically takes30 to 90 days, during which your lender completes final checks, your conveyancer handles the legal transfer, and you arrange insurance.

Common roadblock

Finance falls through between approval and settlement. This can happen if your circumstances change (new debt, job loss) or if the lender's valuation comes in lower than the purchase price. Protect yourself by avoiding any new credit commitments between approval and settlement, and ensure your contract includes a finance clause on private sales. At auction, there is no finance clause, which is why pre-approval is critical.

The process from first inspection to getting the keys follows a clear path: deposit saving, borrowing capacity, loan comparison, property search, negotiation, and settlement. With Stryve Finance guiding your finance from start to finish, there are no hidden fees, no surprises.

Your 2026 First Home Buyer Checklist at a Glance

Before you start

- Calculate your full budget (purchase price, stamp duty, fees, ongoing costs)

- Understand your LVR and whether LMI applies

- Research 2026 government schemes (Help to Buy, First Home Guarantee)

- Check state-specific grants and concessions (NSW or Victoria)

Getting finance ready

- Check your credit report and dispute any errors

- Reduce credit card limits and unnecessary debts

- Gather income and identity documents

- Get pre-approved with a broker

Finding and buying

- Research comparable sales in target suburbs

- Attend inspections and engage a conveyancer

- Arrange building and pest inspections

- Make your offer or bid at auction

Settling in

- Finalise your loan and complete lender requirements

- Arrange property insurance before settlement

- Complete settlement and collect your keys

Read our full guide to first home buyer loans and see how the process works step by step.

Frequently Asked Questions

How much deposit do I need to buy my first home in 2026?

The standard benchmark is 20% of the purchase price to avoid LMI. However, the First Home Guaranteelets eligible buyers purchase with just 5% and no LMI. The Help to Buy scheme reduces your required deposit further through shared equity. Your actual figure depends on the property price, your state, and which schemes you qualify for.

How long does the first home buying process take from start to finish?

Allow three to six months from first budget calculation to settlement. Pre-approval takes one to two weeks, and settlement runs 30 to 90 days after exchange. Starting your finance preparation early gives you the most flexibility.

What are the most common reasons first home buyer applications get rejected?

Low credit scores, insufficient genuine savings, high existing debts (including credit card limits), and unstable income documentation are the most frequent reasons. Each lender weighs these differently, which is why a rejection from one does not mean a rejection from all.

When should I talk to a mortgage broker?

As early as possible. A Stryve Finance broker can assess your borrowing power, identify which schemes you qualify for, and match you to the right lender before you apply, avoiding any unnecessary hits to your credit score.

What is the difference between buying at auction and buying by private sale?

At auction, the fall of the hammer creates a legally binding contract immediately. There is no cooling-off period and no finance clause, so you must have finance fully arranged before you bid. Pre-approval from Stryve Finance is essential if you plan to buy at auction. By contrast, a private sale includes a standard cooling-off period (typically five business days in Victoria and NSW) and allows you to include a finance clause, which protects you if your lender does not come through. Private sale also gives you more room to negotiate on price, conditions, and settlement terms. If you are a first home buyer unsure which method suits your situation, a Stryve Finance broker can walk you through both paths and ensure your finance is ready for whichever opportunity comes first.

Dylan Bertovic is the Director and Senior Finance Broker at Stryve Finance, specialising in non-traditional lending solutions. He helps clients across Australia with tiny home loans, construction finance, equipment and asset lending, refinancing, and investor loans. With deep expertise in self-employed and renovation mortgages, Dylan is known for crafting tailored strategies that get results