If you've been researching the first home buyers grant lately, you've probably noticed the goalposts have moved. Three major policy shifts landed in quick succession, and most online guides haven't caught up yet.

First, Queensland extended its $30,000 regional grant in late 2025 (as confirmed by the Queensland Revenue Office), making it the most generous state-level incentive in the country. Second, the First Home Guarantee was expanded in October 2025, removing income caps and place limits entirely, as announced by Housing Australia. That means thousands of buyers who were previously locked out can now qualify. Third, the federal government launched the Help to Buy equity-sharing program in December 2025 (subject to final state participation agreements), adding a new pathway to ownership.

The result is that more first-home buyers now qualify for support than at any point in the scheme's 25-year history, and search interest in first-home buyer benefits has surged in recent months, reflecting how many Australians are actively exploring their options right now.

This guide exists because the landscape shifted fast. We've mapped every federal scheme and state grant side by side so you can see exactly what you're eligible for and how to combine them for maximum savings.

Federal Schemes Every First Home Buyer Can Access

Before diving into state-by-state details, it's worth understanding the four federal-level schemes available to you. These work alongside your state's first-home owner grant, not instead of it. At Stryve Finance, we help first home buyers navigate all of these schemes together, so nothing gets missed and every eligible dollar ends up in your pocket.

1. First Home Owner Grant (FHOG)

The FHOG was introduced on 1 July 2000 to offset the impact of GST on home ownership. The first home buyers grant (also called the First Home Owner Grant or FHOG) is a one-off payment from state and territory governments to help eligible Australians buy their first new home. Since its launch, more than 1.4 million grants have been paid nationally, totalling over $12 billion in assistance. It's funded by each state and territory under their own legislation, which is why grant amounts and price caps vary. The key rule that applies across the board: FHOG applies only to new homes or substantially renovated properties, not to established homes. Only one grant is payable per person or couple, regardless of which state you buy in. You must be an Australian citizen or permanent resident and occupy the home as your principal place of residence.

2. First Home Guarantee

The First Home Guarantee scheme lets you buy with just a 2 to 5% deposit without paying Lenders Mortgage Insurance (LMI). LMI is typically required when your loan-to-value ratio (LVR) the percentage of the property's value you're borrowing, exceeds 80%. On a $700,000 home with a 5% deposit, your LVR is 95%, and LMI can add $15,000 to $25,000 to your upfront costs. The First Home Guarantee lets the government act as guarantor on the gap, so you avoid that cost entirely. Since October 2025, income caps and place limits have been removed, opening the scheme to a much wider pool of buyers.

3. Help to Buy

The Help to Buy scheme is a federal equity-sharing program in which the government holds a share of your home. This means you need a smaller deposit and a smaller loan, reducing both your upfront costs and your ongoing repayments.

4. First Home Super Saver Scheme (FHSS)

The FHSS lets you make voluntary contributions to your super fund and later withdraw them to put toward a deposit. Because super contributions are taxed at a lower rate, you effectively save faster. If you want the full walkthrough, read our guide on applying for the FHSS.

State-by-State First Home Buyers Grant Guide for 2026

Every state and territory runs its own version of the FHOG, with different grant amounts, price caps, and stamp duty concessions for first-home buyers. Here's what each offers in 2026.

New South Wales

The first home buyers grant in NSW provides $10,000 for new homes up to the state's property price cap. NSW also offers a stamp duty exemption for first home buyers on properties up to certain thresholds, which can save you tens of thousands on top of the grant itself. For established homes, you won't get the FHOG, but stamp duty concessions may still apply.

Queensland

The first home buyers grant QLD is the standout in 2026. Queensland offers $15,000 for new homes in metro areas and an incredible $30,000 for regional new builds, with the incentive extended in late 2025. This is the highest state grant available anywhere in Australia. The grant applies only to new or substantially renovated homes. Property price caps apply, so check the Queensland Revenue Office for current thresholds.

Victoria

The first-home buyers grant in VIC provides $10,000 for new homes in metropolitan Melbourne and regional areas. Victoria also offers stamp duty concessions and exemptions depending on the property value. Regional buyers may access additional benefits. As with all states, the grant is available only for new or substantially renovated homes.

Western Australia

The first-home buyers grant WA offers is $10,000 for new homes. WA has its own property price cap for eligibility, and the Western Australian government confirms that only one grant is payable per person or couple. Stamp duty concessions are also available for first home buyers purchasing below certain thresholds.

South Australia

South Australia provides a $15,000 FHOG for new homes with a property price cap of $650,000. Stamp duty concessions are available for first home buyers purchasing below certain thresholds, and the state has been competitive in keeping these thresholds accessible. For current amounts and caps, check RevenueSA at revenuesa.sa.gov.au.

Tasmania

Tasmania offers a $30,000 FHOG for new homes one of the highest in the country in dollar terms. With Tasmania's median house price sitting around $560,000 (compared to Sydney's $1.1 million), the grant stretches considerably further here than in most other states. Stamp duty concessions also apply for eligible buyers. For current thresholds, check the State Revenue Office Tasmania at sro.tas.gov.au.

Australian Capital Territory

The ACT takes a different approach. Rather than a traditional FHOG, the territory focuses on stamp duty concessions for first-home buyers. These can be substantial depending on the property value. Check ACT Revenue for current concession thresholds.

Northern Territory

The NT offers a $10,000 FHOG for new homes with a property price cap of $650,000. The NT also provides a home renovation grant of up to $10,000 for eligible renovations to existing homes, a rare additional benefit not available in most other states. Stamp duty concessions apply, and first home buyers purchasing below $650,000 may receive a full stamp duty exemption. Verify current thresholds at territorytax.nt.gov.au.

Quick comparison of key states:

| State | FHOG amount | Applies to | Stamp duty |

|---|---|---|---|

| NSW | $10,000 | New homes | Yes, up to threshold |

| QLD | $15,000 - $30,000 | New homes | Yes |

| VIC | $10,000 | New homes | Yes |

| WA | $10,000 | New homes | Yes |

| SA | $15,000 | New homes | Yes |

| TAS | $30,000 | New homes | Yes |

| ACT | No traditional FHOG | N/A | Yes, stamp duty concessions instead |

| NT | $10,000 | New homes | Yes |

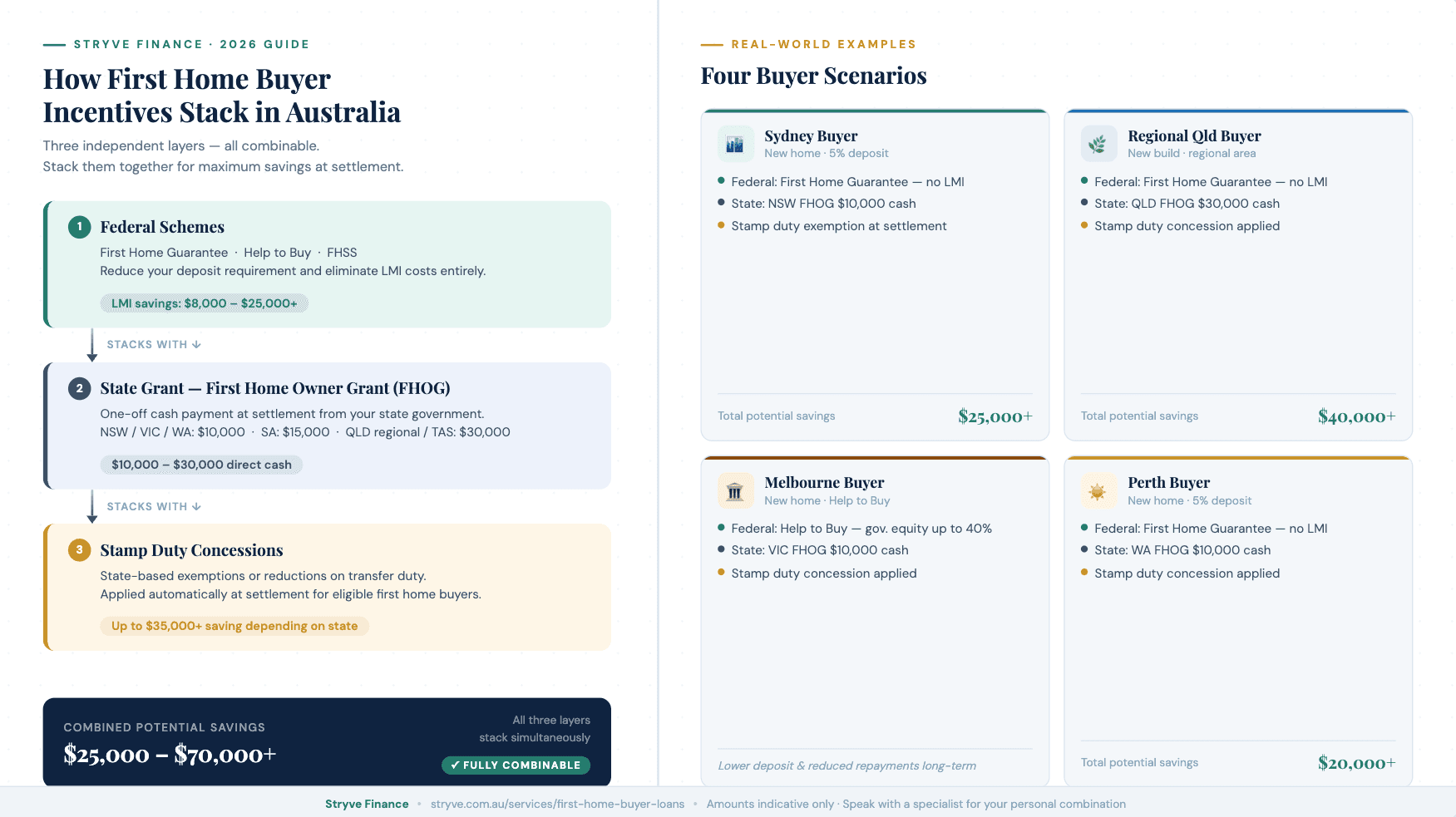

How to Stack Grants and Schemes for Maximum Savings

Here's where it gets genuinely exciting. State grants and federal schemes are not either/or. You can combine them. Let's look at what that means in real dollar terms.

Scenario 1: Sydney buyer, new home, 5% deposit.

You could stack the NSW FHOG ($10,000), the First Home Guarantee (no LMI, potentially saving $8,000 to $15,000 on a typical Sydney purchase), and the NSW stamp duty exemption. Total potential savings: $25,000 or more, depending on purchase price.

Scenario 2: Regional Queensland buyer, new build.

Stack the QLD $30,000 regional grant with the First Home Guarantee. You're looking at the grant itself plus thousands in LMI savings. Total potential savings: $40,000 or more before you even factor in FHSS tax advantages on your deposit savings.

Scenario 3: Melbourne buyer, new home, using Help to Buy.

Combine the VIC $10,000 FHOG with the Help to Buy equity share (reducing your loan size and deposit requirement), plus any FHSS savings you've built up. The government's equity share means lower repayments for years to come.

Scenario 4: Perth buyer, 5% deposit.

Stack the WA $10,000 FHOG with the First Home Guarantee and WA stamp duty concessions. With access to 40 or more lenders, a broker can find the right loan to pair with your grants for the best overall outcome.

It's not as complicated as it looks. The pieces fit together, and a broker can map the combination that works for your situation.

See which grants and schemes you're eligible for. Talk to a Stryve Finance first home buyer specialist to explore each scheme in detail and map the combination that maximises your savings.

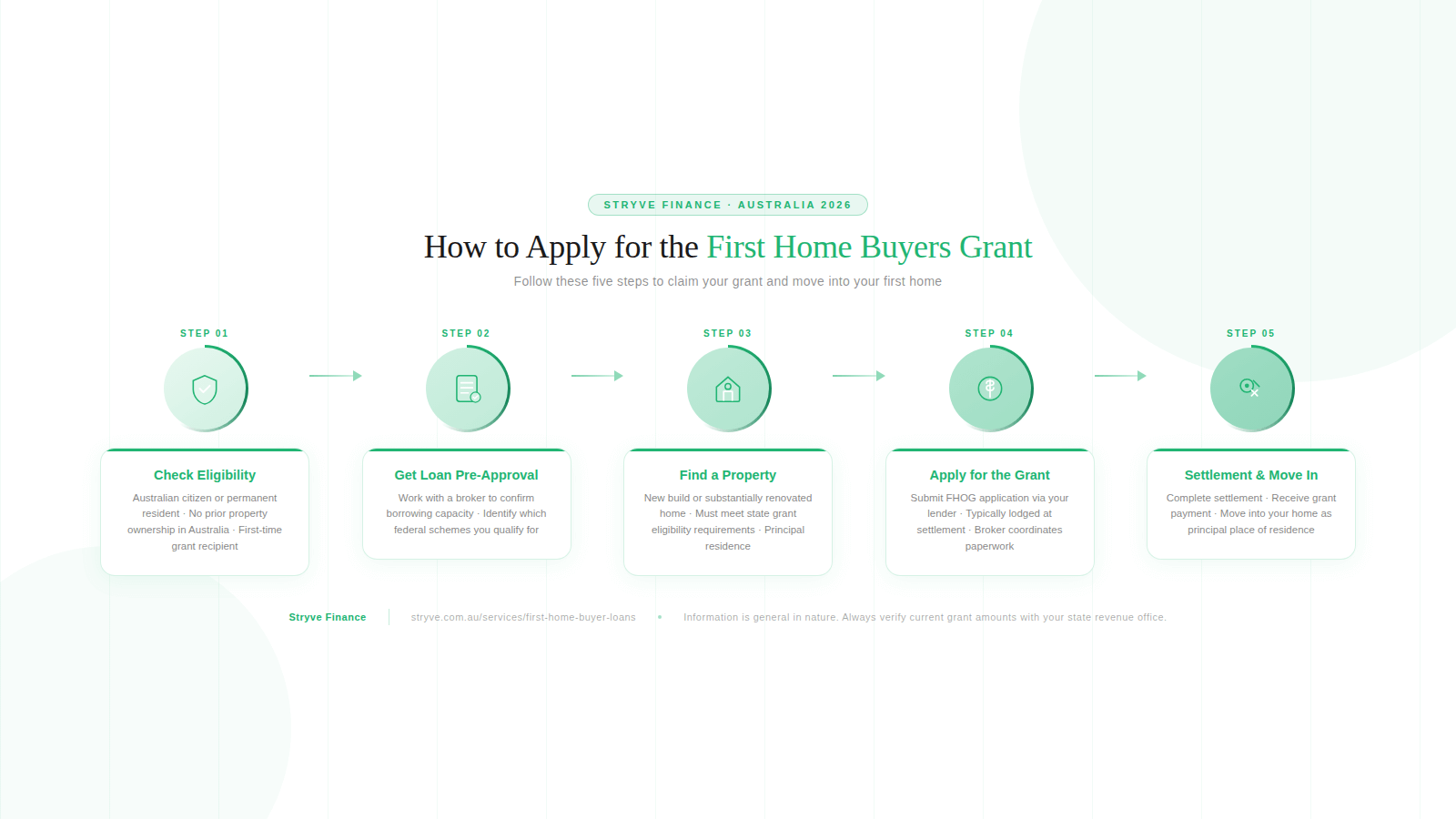

How to Apply for the First Home Buyers Grant

The process is more straightforward than most people expect. Here's the timeline.

Step 1: Check your eligibility.

You must be an Australian citizen or permanent resident. You must not have previously received an FHOG or owned residential property in Australia. The home must be new or substantially renovated (meaning major structural work, not just a kitchen refresh).

Step 2: Get pre-approval.

This tells you how much you can borrow and confirms which schemes you qualify for. A first home buyer loan specialist handles the complexity here, comparing options across lenders and matching you with the right grants.

Step 3: Find your property.

Your “principal place of residence” simply means the home you'll live in as your main address. You need to move in within 12 months of settlement in most states.

Step 4: Apply for your grants.

The FHOG is typically applied for through your lender at settlement, not as a separate application. Your broker coordinates this alongside your loan paperwork.

Step 5: Settle and move in.

“Settlement” is the legal completion date when ownership transfers to you, and funds are exchanged. Your FHOG is usually credited at this point.

Most eligible buyers are approved. The key is confirming eligibility upfront so there are no surprises later. Your broker handles the bulk of the paperwork and keeps everything on track.

Frequently Asked Questions about First Home Buyer Grants

Can I get the FHOG for an existing home?

No. The FHOG only applies to new homes or substantially renovated properties across all states and territories. If you're buying an established home, you may still be eligible for stamp duty concessions, the First Home Guarantee, or Help to Buy.

Can I combine state and federal schemes?

Yes. State grants such as the FHOG, stamp duty concessions, and federal schemes such as the First Home Guarantee and Help to Buy can be stacked. The scenarios above show how this works in practice.

What if I've owned property overseas?

Owning property overseas does not automatically disqualify you, but rules vary by state. The consistent requirement is that you must not have previously owned residential property in Australia or received an FHOG.

Do I need to live in the property?

Yes. You must occupy the home as your principal place of residence. Most states require you to move in within 12 months of settlement and live there for a continuous period.

What's the income limit for the First Home Guarantee in 2026?

Since October 2025, income caps have been removed from the First Home Guarantee. There is no longer an income threshold to qualify, which is a significant change from previous years.

Can my partner and I both claim the grant?

No. Only one FHOG is payable per person or couple, regardless of which state you purchase in.

What is the Difference Between the First Home Buyers Grant and Help to Buy?

These are two completely different types of support. The FHOG is a one-off cash payment, you receive the money (typically $10,000-$30,000, depending on your state), and it goes directly toward your purchase. Help to Buy, by contrast, is an equity-sharing arrangement where the federal government co-purchases a share of your home (up to 40% for new builds), reducing your required deposit and your loan size. You own your home outright in day-to-day terms, but the government holds a financial interest it recoups when you sell or buy it out. The key point: you can use both. Stacking the FHOG cash payment with Help to Buy's equity contribution is one of the most powerful combinations available to eligible buyers in 2026.

Dylan Bertovic is the Director and Senior Finance Broker at Stryve Finance, specialising in non-traditional lending solutions. He helps clients across Australia with tiny home loans, construction finance, equipment and asset lending, refinancing, and investor loans. With deep expertise in self-employed and renovation mortgages, Dylan is known for crafting tailored strategies that get results