Last updated: June 2026

If you're getting ready to buy your first home, pre-approval is the step that turns “I think I could buy a place” into “I know what I can afford.” It's where your budget stops being a guess and becomes something you can house hunt with.

But most guides skip the parts that actually matter: what to do before you apply, why approvals get delayed, and what gets buyers rejected. This one doesn't.

What Is Pre-Approval (and Conditional Approval)?

Pre-approval is a lender's conditional “yes.” Based on your income, savings, debts and credit history, the lender tells you roughly how much they're willing to lend before you've found a property.

You'll also hear it called conditional approval in Australian lending, pre-approval and conditional approval mean the same thing. It's an in-principle agreement to lend you a specific amount, issued before you find a property, and it typically lasts 3 to 6 months.

There are two kinds:

- A system-generated pre-approval runs your details through an automated check. It's fast, but carries less weight because no human has reviewed your file.

- A full-assessment pre-approval involves a credit assessor thoroughly reviewing your documents. It takes longer but is far more reliable, and far more persuasive to agents and at auction.

One thing pre-approval is not is a guarantee. It indicates your borrowing capacity, but final (unconditional) approval only comes after you've found a property and the lender completes a valuation and final checks. Think of it as a budget you can trust enough to shop with confidence.

Before You Apply: 4 Things to Do First

Most guides jump straight to “submit your application.” Here's what to do in the two to four weeks beforehand.

- Check your credit score. Three credit bureaus operate in Australia, Equifax, illion and Experian, and you can request a free copy of your report from each. A forgotten default or an old bill in collections can derail an application, so it's better to find it now.

- Confirm your deposit position. Work out your LVR (loan-to-value ratio), your loan size compared to the property's value. If your deposit is under 20%, you'll generally pay Lenders Mortgage Insurance (LMI), a one-off cost that protects the lender. Also check whether you qualify for the First Home Owner Grant in your state, which can lift your deposit position (amounts vary by state and property type). Our deposit guide shows where you stand.

- Track your spending for 30 days. Lenders read your bank statements closely. Buy-now-pay-later, subscriptions, gambling and frequent discretionary spending all feed into their view of whether you can repay.

- Stop applying for new credit. Every application, a card, a car loan, even a phone plan, leaves an enquiry on your file, and several in a short window can hurt your score. Avoid applying to multiple lenders at once for the same reason.

Once you've ticked these off, check your estimated borrowing capacity for a ballpark figure before you formally apply.

Documents You'll Need

Having your paperwork ready before you apply is the single biggest thing you can do to speed up pre-approval. Requirements vary by income type.

If you're a PAYG employee

- 100 points of ID (driver's licence, passport, Medicare card)

- Last 2-3 payslips to show current, ongoing income

- Most recent tax return or Notice of Assessment (downloadable free from myGov)

- 3 months of bank statements showing your spending and savings

- Details of all existing debts, credit cards, HECS-HELP, car loans, BNPL

If you're self-employed

- Two years of personal and business tax returns

- ATO Notices of Assessment for both years

- Business Activity Statements (BAS) for the last 12 months

- An accountant's letter or financial statements

- ABN registration details

If you're casual, on a fixed-term contract, or earning irregular income, most lenders will want around two years of tax returns to show stability. Self-employed applications are more complex but far from impossible, Stryve Finance specialises in self-employed borrowers and knows which lenders are flexible with non-standard income.

For the complete list, see our full application document checklist.

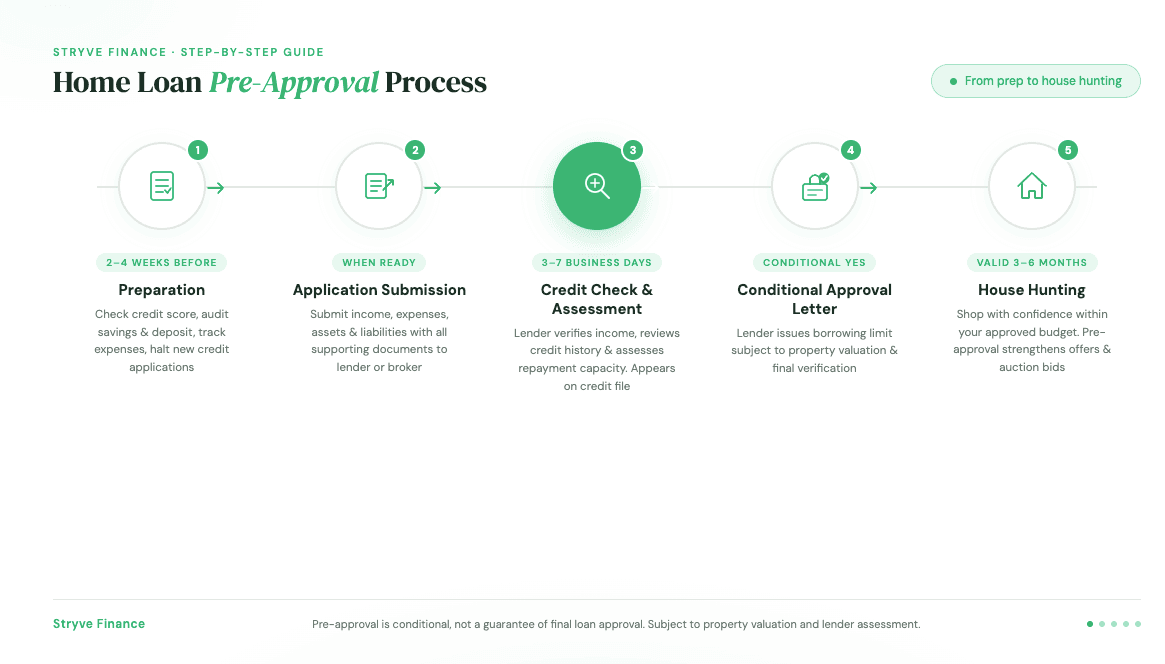

How to Apply for Pre-Approval, Step by Step

You've done the prep. Here's the actual process.

1. Choose your path: broker or direct to a bank

Going direct means you only see one bank's products. A broker compares options across many lenders. Stryve Finance has access to 50+ lenders, so your application is matched to the lender most likely to approve it on the best terms, and broker commission is disclosed upfront, with no fees to you as the borrower.

| Mortgage broker (e.g. Stryve Finance) | Direct to bank |

|---|---|

| Access to 50+ lenders | Limited to one lender's products |

| One credit enquiry, matched to the right lender first | May need multiple applications to compare |

| Commission disclosed upfront; no fees to the borrower | Direct relationship with the lender |

2. Submit your application and documents

Online or through your broker, you'll complete a detailed application covering income, expenses, assets and liabilities, with the documents from the checklist attached.

3. The lender runs a credit check and assessment

They verify your income, review your credit history and assess your ability to repay. This check appears on your credit file, which is exactly why applying to one well-matched lender beats blanketing the market.

4. Receive your conditional approval letter

This sets out how much the lender will lend, subject to conditions like finding a suitable property and a satisfactory valuation.

Working with a broker reduces the risk of rejection by identifying the right lender before you apply, fewer enquiries, a cleaner file. Talk to a Stryve Finance broker to get matched to the right lender the first time.

How Long Does Home Loan Pre-Approval Take?

A system-generated pre-approval can come back in 24-48 hours. A full-assessment pre-approval usually takes 3-7 business days, or up to 2-3 weeks for complex cases.

| Type | Timeline | Reliability | Best for |

|---|---|---|---|

| System-generated | 24-48 hours | Lower, automated, less scrutiny | A quick budget check; not for auctions |

| Full-assessment | 3-7 business days (up to 2-3 weeks if complex) | Higher, a human assessor reviews everything | Auctions, competitive markets, serious buyers |

What affects the speed:

- How complete your documentation is, one missing item can add days.

- The lender's processing times, some are consistently faster than others.

- How complex your finances are, self-employed or multiple-income applicants take longer to verify.

- Time of year, end-of-year and holiday periods create industry-wide backlogs.

Your pre-approval is typically valid for 3 to 6 months. If you haven't found a property by then, extensions are generally possible, so you won't necessarily start from scratch.

Why Pre-Approval Gets Delayed in Australia (and How to Avoid It)

Delays are one of the most common frustrations in the pre-approval process, and they're usually preventable. Knowing what causes them puts you ahead.

The most common causes of pre-approval delays:

- Incomplete or inconsistent documents. If your bank statements don't match your declared income, the lender pauses to ask questions.

- Recent changes to your job or income. Starting a new role mid-application, even a higher-paying one, introduces uncertainty.

- Undisclosed liabilities such as BNPL accounts, discovered during the credit check.

- Lender backlogs during peak periods.

- Mid-application policy changes, shifts in APRA lending guidelines or a lender's own serviceability rules can change your numbers.

How to avoid them:

- Submit every document upfront, don't drip-feed paperwork.

- Be transparent about all debts, including BNPL and HECS-HELP.

- Don't change jobs during the application window.

- Avoid large, unexplained transactions in the months before you apply. A sudden $10,000 deposit from an unclear source will trigger questions.

A delay doesn't mean a rejection. It usually means the lender needs more information, so respond quickly and completely when they ask. A broker helps most here by submitting a clean, complete application the first time and heading off the back-and-forth that slows everything down.

5 Mistakes That Get Pre-Approval Rejected

These are all preventable.

- Not disclosing all debts. BNPL services like Afterpay and Zip are liabilities, and lenders find them on your credit file regardless. Undisclosed debt is a red flag.

- Changing jobs mid-application. Lenders want income stability; even a better role can cause issues during a probation period.

- Applying to multiple lenders at once. Each application triggers an enquiry every other lender can see, which can hurt your score. Work with a broker to identify the right lender first.

- Overstating income or understating expenses. Lenders verify everything against tax returns, payslips and bank statements. Inconsistencies lead to rejection.

- Making large, unexplained deposits or withdrawals. A $15,000 cash deposit with no paper trail looks like undisclosed debt or undeclared income. Keep your accounts clean and explainable.

For a broader view of pitfalls, see our guide to first home buyer mistakes.

Pre-Approval vs Unconditional Approval

Pre-approval (conditional approval) is the lender's in-principle agreement based on your finances. Unconditional approval, also called formal or full approval, comes after you've found a specific property and the lender has completed a full valuation and final verification.

Pre-approval can still fall through before that point. The usual reasons:

- The property valuation comes in lower than the purchase price.

- Your finances change, new debt, a job loss, reduced income.

- The lender updates its lending policies.

That's a normal part of the process, not a sign something went wrong, and extensions are often available if you need more time to find the right place. Once you reach unconditional approval, you can move towards exchange and settlement, our guide on the path from approval to settlement covers what happens next.

What to Do After You're Pre-Approved

With pre-approval in hand, you can house hunt within a defined budget, and agents and sellers take pre-approved buyers more seriously. At auction, you bid knowing your limit.

A few things to keep in mind:

- Watch the expiry date. Pre-approval typically lasts 3 to 6 months, mark it in your calendar.

- Keep your finances stable. Don't take on new debt, change jobs, or make large unexplained transactions.

- Your serviceability assessment is set from when you applied. If lending criteria tighten later, that can work in your favour.

If you haven't started yet, now is the time. See what you could qualify for and get your pre-approval moving with Stryve Finance.

Frequently Asked Questions

What does conditional approval mean on a home loan?

Conditional approval is another name for pre-approval. It's a lender's in-principle agreement to lend you a set amount based on your income, savings, debts and credit history, issued before you've found a property. It's “conditional” because final approval still depends on finding a suitable property and a satisfactory valuation.

How long does home loan pre-approval last?

Most pre-approvals are valid for 3 to 6 months. If you haven't found a property in that time, you can usually apply for an extension rather than starting again.

Does pre-approval affect my credit score?

Applying for pre-approval creates a credit enquiry on your file, which can have a small effect. The bigger risk is applying to several lenders at once, since multiple enquiries in a short period can lower your score. Going through one well-matched lender or a broker keeps your file clean.

Can pre-approval be declined or fall through?

Yes. Pre-approval isn't a guarantee. It can fall through if a property valuation comes in low, your financial situation changes, or the lender updates its policies. This is why it's called conditional approval.

Can I get pre-approval online?

Yes. Many lenders offer online pre-approval, often as a fast system-generated result. It's useful for a quick budget check, but a full-assessment pre-approval reviewed by a credit assessor carries far more weight at auction or in a competitive market.

What's the difference between system-generated and full-assessment pre-approval?

A system-generated pre-approval is automated and fast (24 to 48 hours) but less reliable. A full-assessment pre-approval is reviewed by a human credit assessor, takes longer (3 to 7 business days), and is taken much more seriously by agents and sellers.

Dylan Bertovic is the Director and Senior Finance Broker at Stryve Finance, specialising in non-traditional lending solutions. He helps clients across Australia with tiny home loans, construction finance, equipment and asset lending, refinancing, and investor loans. With deep expertise in self-employed and renovation mortgages, Dylan is known for crafting tailored strategies that get results