If you're a first-home buyer right now, you're staring down two major government schemes with confusing overlap, and a property market where every month of indecision costs you money. You're not imagining it. This is genuinely complicated.

Here's where things stand. The Help to Buy shared equity scheme launched in December 2025. The First Home Guarantee (officially the Australian Government 5% Deposit Scheme) was expanded in October 2025, with unlimited places and the removal of income caps. Both are designed to get you into your first home sooner. But they work in fundamentally different ways, and choosing the wrong one could cost you tens of thousands over the life of your loan.

The urgency is real. The RBA cash rate sits at 3.85% following the February 2026 hike, and three of four major banks predict another rise in May 2026. That tightens borrowing power and makes scheme choice more consequential than ever.

This article is a decision framework, not just a feature list. Both schemes sit within a broader suite of government schemes and grants available to first-home buyers, and by the end of this guide, you'll know exactly which one fits your situation.

Help to Buy vs First Home Guarantee at a glance

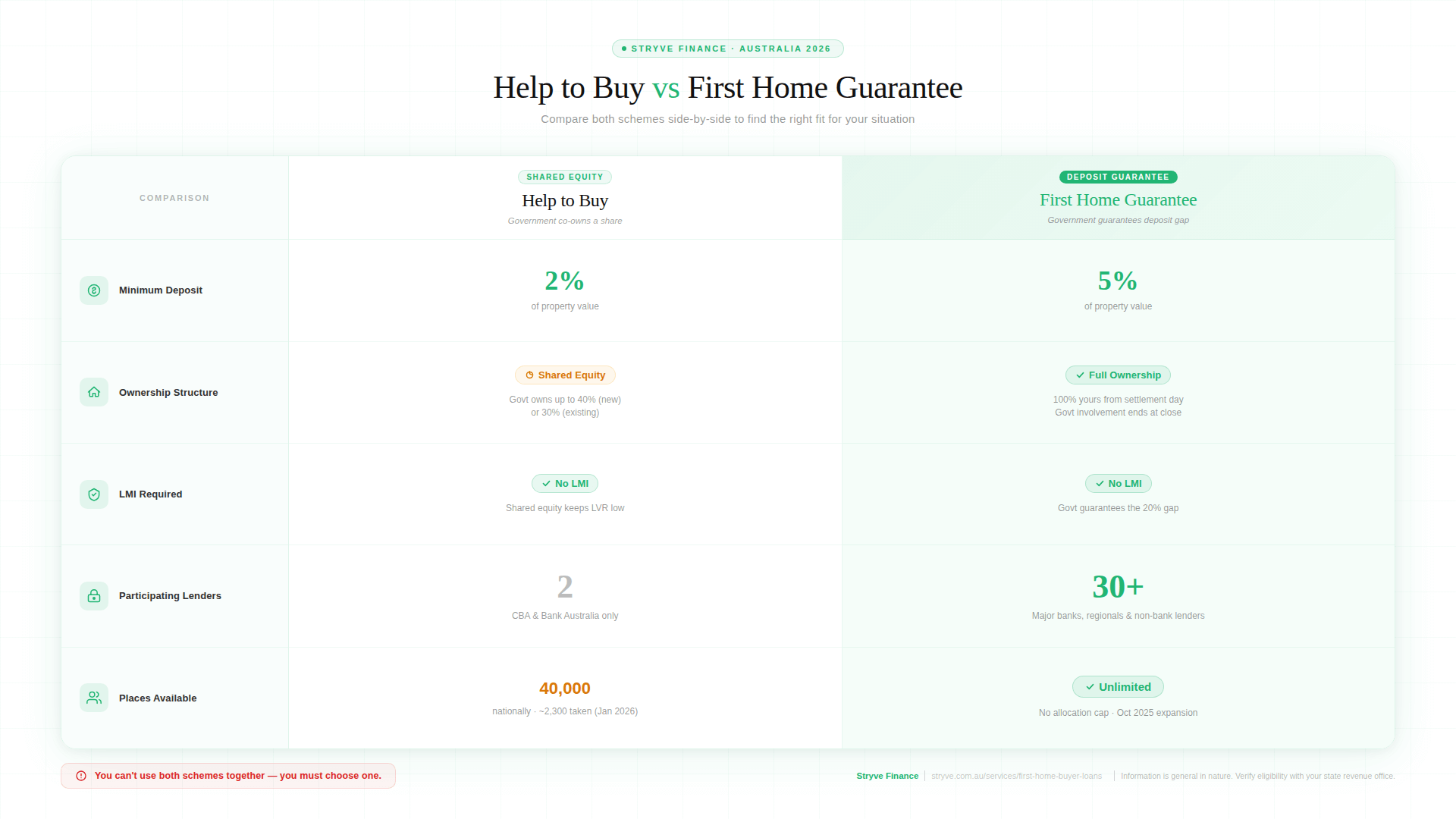

Before we get into the details, here's the fundamental difference you need to understand. Help to Buy is shared equity. The government co-owns your home. You get a smaller loan, but you don't own 100% of the property. The First Home Guarantee is exactly that, a guarantee. The government guarantees the gap, so you avoid Lenders Mortgage Insurance (LMI), but you own your home outright from day one.

LMI is insurance that protects the lender (not you) when you borrow more than 80% of a property's value. LVR (loan-to-value ratio) is the percentage of the property's value that you borrow. Both schemes eliminate LMI, but through very different mechanisms.

You cannot use both schemes together. You must choose one.

Here's how they compare side by side. For a deeper understanding, read how the Help to Buy shared equity scheme works and the full details on the First Home Guarantee.

| Feature | Help to Buy | First Home Guarantee |

|---|---|---|

| Minimum deposit | 2% | 5% |

| Ownership structure | Shared equity (government owns up to 40% new / 30% existing) | Full ownership from day one |

| LMI required | No | No |

| Government equity stake | Yes, appreciates with property value | None |

| Income caps | Yes, apply | Removed (October 2025) |

| Property price caps | Yes, vary by location | Yes, higher caps post-expansion |

| Number of places | 40,000 nationally | Unlimited |

| Participating lenders | 2 (CBA, Bank Australia) | 30+ lenders |

| Refinancing flexibility | Restricted | Unrestricted |

That lender column is worth a closer look.

The lender limitation problem nobody is talking about

Right now, only two lenders participate in Help to Buy: Commonwealth Bank and Bank Australia. That's it.

Compare that to the First Home Guarantee's panel of 50+ participating lenders, which includes major banks, regional banks, and non-bank lenders. More lenders means more competition on rates, more product options, and more flexibility in how your loan is structured. This matters practically. Most mortgage brokers can't lodge Help to Buy applications yet because their aggregator platforms haven't integrated the scheme. If you're working with a broker who doesn't have access to CBA or Bank Australia on their panel, they physically can't help you with Help to Buy.

We'll be transparent here. As first-homebuyer loan specialists, Stryve has access to 50+ lenders, including. Help to Buy participating lenders. But even with that access, we'd be doing you a disservice if we didn't flag that two lenders versus thirty-plus is a significant constraint on your ability to secure a competitive rate.

When rates are rising, the difference between lenders' pricing can be as high as 0.30% to 0.50%. That gap compounds over the life of your loan. Which brings us to the real cost question.

What shared equity actually costs you over 5 and 10 years

This is where most comparisons stop at the eligibility checklist. Let's go further.

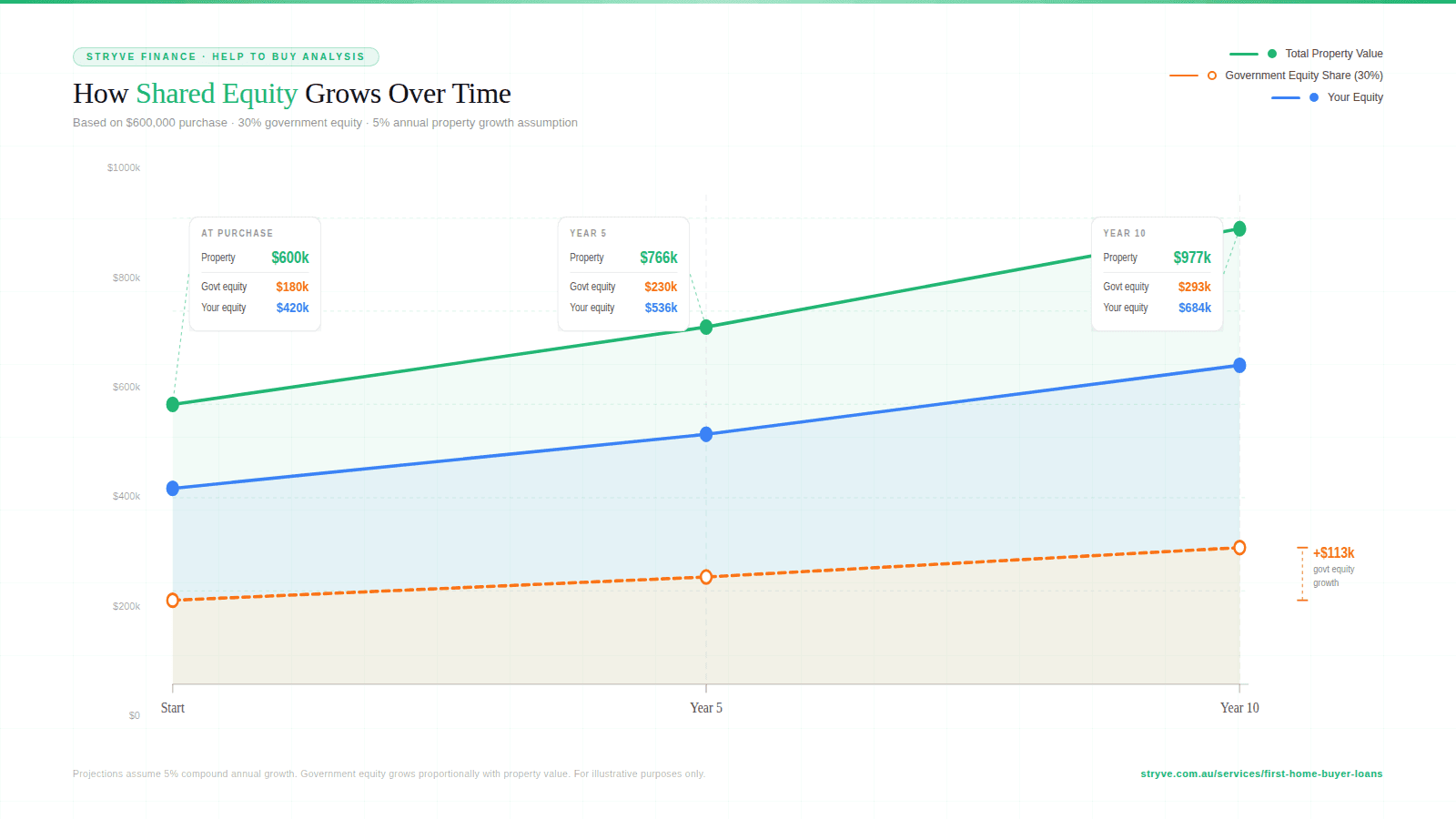

Take a $600,000 existing property. Under Help to Buy, the government contributes 30%, owning $180,000 of equity. You put down 2% ($12,000) and borrow the remaining 68% ($408,000). Under the First Home Guarantee, you put down 5% ($30,000), borrow 95% ($570,000), pay no LMI, and own 100%.

The Help to Buy borrower has significantly lower repayments. No question. But the government's 30% share is not a fixed dollar amount. It's equity. It grows in value with your property.

At 5% annual growth over 5 years:

- Property value: ~$766,000

- Government's 30% share: ~$230,000

- That's $50,000 more than their original contribution, and it's money you'll need to pay to buy them out

At 5% annual growth over 10 years:

- Property value: ~$977,000

- Government's 30% share: ~$293,000

- The cost of buying out the government has grown by $113,000, equity that would have been yours under the Guarantee

Under the First Home Guarantee, the government's involvement ends at settlement. Every dollar of growth is yours.

There are also refinancing restrictions under Help to Buy. You generally need to buy out the government's share or refinance within the participating lender panel. That limits your ability to chase better rates down the track.

The shared equity model isn't bad. But you need to understand what it actually costs over time, not just what it saves you today.

Get a personalised comparison based on your deposit, income, and property goals.

How Rising Rates Change the Equation

Here's the trade-off that makes this decision genuinely difficult.

Help to Buy borrowers only service a loan on 58-68% of the property's value. When the RBA cash rate is 3.85% and potentially heading higher in May 2026, that's a meaningful buffer. Your repayments are lower, and each rate rise hits you less hard in dollar terms.

But remember the lender constraint. With only two participating lenders, you can't shop around for the sharpest rate. In a rising rate environment, that lack of competition could erode some of the repayment advantage.

First Home Guarantee borrowers service a loan on 95% of the property's value. Repayments are higher and more sensitive to each rate movement. However, access to 30+ lenders means you can secure a more competitive rate upfront and refinance freely if better options emerge. Neither scheme wins outright here. If your income has a limited buffer for rate rises, Help to Buy's lower loan amount provides genuine protection. If you have a comfortable income buffer and want to maximise long-term equity, the Guarantee's flexibility and lender access may better suit you.

Application Reality Check

Help to Buy requires state legislation to operate. Not all states have passed the necessary laws yet, so your first step is to confirm your state is participating. This is a practical barrier that catches people off guard.

Of the 40,000 places available nationally, around 2,300 had been approved by the end of January 2026. That's roughly 5.75% uptake in the first two months. Plenty of spots remain, but the allocation is finite and will tighten as awareness grows.

The First Home Guarantee, by contrast, now has unlimited places following the October 2025 expansion. No allocation stress. No rushing to beat a cap.

Here's the practical move. If you're considering Help to Buy but aren't sure about your state's participation or your eligibility, a broker can prepare both pathways simultaneously. If Help to Buy doesn't work out, you can pivot to the Guarantee without starting from scratch. Explore your 5% deposit home loan options under the Guarantee as a parallel pathway from day one.

Which Scheme is Right for You: Three Real Buyer Scenarios

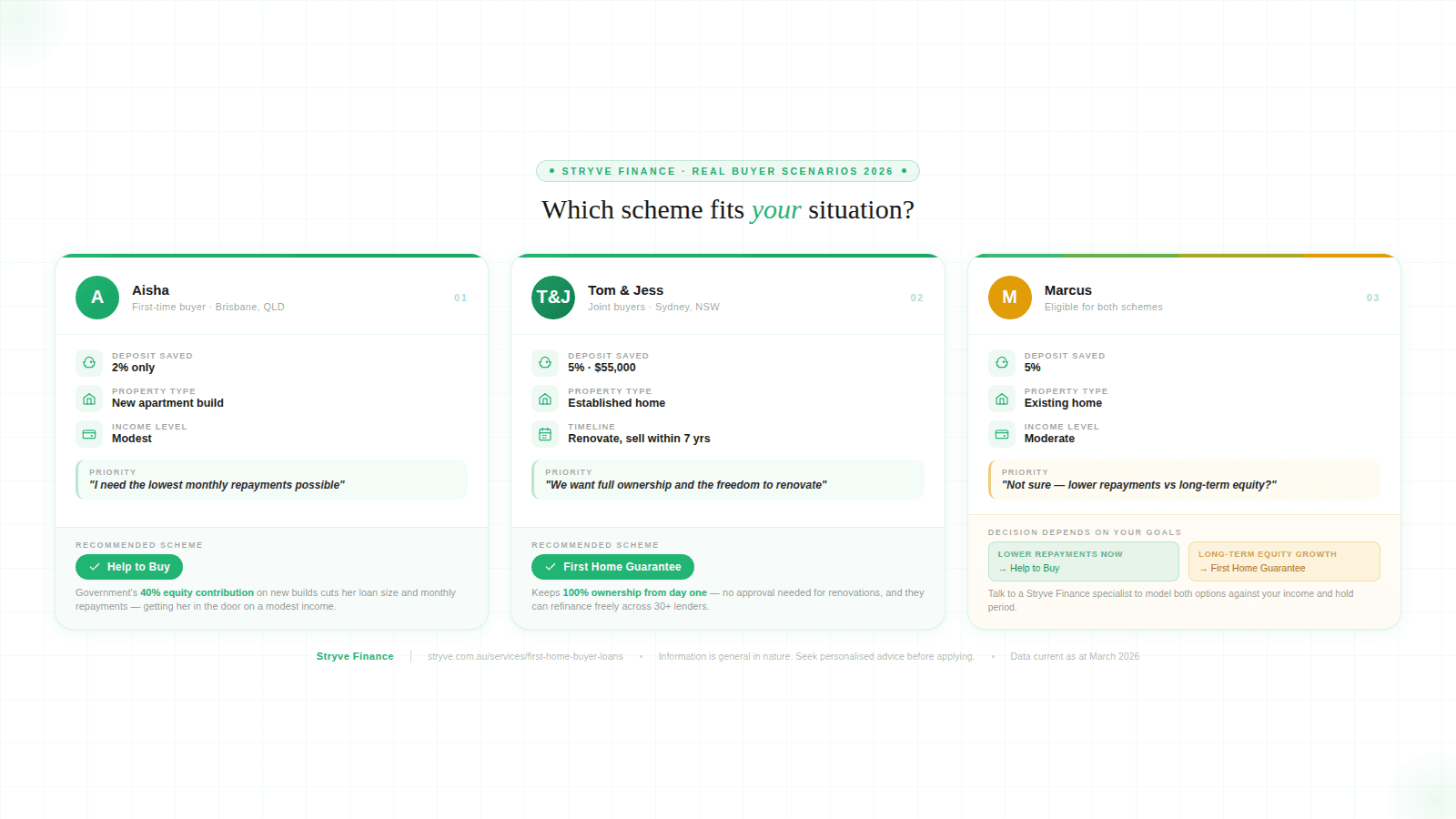

Scenario 1: Aisha, buying a new apartment in Brisbane

Aisha has saved a 2% deposit and earns a modest income. She's buying a new build in a participating state. Help to Buy lets her get in sooner with lower repayments, and the government's 40% contribution on a new home dramatically reduces her loan size. The lender limitation is a trade-off she's willing to accept because the repayment protection matters more to her right now. Help to Buy is the stronger fit.

Scenario 2: Tom and Jess, buying an established home in Sydney

They've saved 5% ($55,000) and want full control. They plan to renovate within three years and potentially sell within seven. Shared equity would restrict renovations (you typically need approval for major changes to a co-owned property) and mean handing back 30% of any value they add. They also want to shop rates across multiple lenders. The First Home Guarantee is the clear choice.

Scenario 3: Marcus qualifies for both but can't decide

Marcus has 5% saved, earns a moderate income, and is buying an existing home in a participating state. Marcus's decision framework comes down to three questions. Do you value lower repayments now, or full equity growth later? How long do you plan to hold the property? Are you comfortable with only two lender options?

If Marcus plans to hold for 10+ years and values simplicity, the Guarantee's full ownership and lender flexibility may outweigh Help to Buy's repayment savings. If he's stretched on income and needs the lowest possible repayments to sleep at night, Help to Buy deserves serious consideration.

Choosing the simpler option is not choosing the lesser option. Both schemes exist because different buyers need different things.

Choose Help to Buy if...vs choose the First Home Guarantee if. . .

Choose Help to Buy if:

- You have less than 5% deposit saved

- You're buying in a participating state with legislation passed

- You're comfortable with the government co-owning your home

- You need the lowest possible repayments to manage rate rises

- You're happy to work with CBA or Bank Australia

- You plan to hold long-term and can manage the buyout process later

Ready to take the next step? Explore Help to Buy with a specialist broker.

Choose the First Home Guarantee if:

- You want full ownership from the settlement day

- You want access to competitive rates across 30+ lenders

- You plan to renovate, sell, or refinance within 5-10 years

- You value the flexibility to switch lenders down the track

- You have 5% deposit saved and want unlimited scheme availability

Check your eligibility and see if you qualify for the 5% deposit scheme.

You cannot use both. It's one or the other, which is exactly why personalised advice matters. See which scheme you qualify for, and talk to a first-home buyer specialist.

Frequently Asked Questions

Can I use Help to Buy and the First Home Guarantee together?

No. You must choose one scheme. They cannot be combined. A broker can help you assess which one delivers more value based on your specific deposit, income, and property goals.

What happens when I want to sell my Help to Buy property?

The government receives their equity share based on the property's market value at the time of sale, not the original purchase price. If your home has grown in value, so has your share. This is the core mechanic of shared equity.

Do I pay LMI with either scheme?

No. Under Help to Buy, the shared equity structure means your LVR stays low enough to avoid LMI. Under the First Home Guarantee, the government guarantees the gap between your 5% deposit and the 20% threshold lenders normally require.

Can I refinance a Help to Buy loan?

Restrictions apply. You generally need to either buy out the government's share first or refinance within the participating lender panel (currently CBA and Bank Australia). This is a significant limitation compared to the Guarantee, which allows you to refinance freely with any lender at any time.

What is the Help to Buy scheme exactly?

In plain terms, the government buys a portion of your home alongside you, up to 40% for new builds, 30% for existing homes. You live in the property and make repayments on your smaller loan. But the government owns their percentage and gets it back (adjusted for market value) when you sell, refinance fully, or reach certain triggers. It's not a grant. It's not a loan. It's co-ownership.

For a full rundown of other grants and schemes you might be eligible for, including state-based concessions and the First Home Owner Grant (FHOG), check our complete guide.

Not sure where to start? Talk to a broker who knows both schemes inside out.

Dylan Bertovic is the Director and Senior Finance Broker at Stryve Finance, specialising in non-traditional lending solutions. He helps clients across Australia with tiny home loans, construction finance, equipment and asset lending, refinancing, and investor loans. With deep expertise in self-employed and renovation mortgages, Dylan is known for crafting tailored strategies that get results