You have never missed a repayment. Not one. You have paid every month, on time, for years. But when you try to refinance to a lower rate, the answer comes back no. Not because of bad credit. Not because of missed payments. Because of a regulatory test you did not know existed. This is the mortgage prisoner Australia problem, and it is affecting more borrowers in 2026 than at any point since the APRA buffer was tightened.

That is what it means to be a mortgage prisoner in Australia.

Mortgage prisoner definition

A mortgage prisoner is a borrower who is trapped on an uncompetitive rate with their current lender because they cannot pass the serviceability assessment required by a new lender. They are meeting all their repayments but are unable to refinance to a lower rate due to APRA's 3% serviceability buffer.

This is different from the UK definition, where mortgage prisoners are typically borrowers stuck with closed-book lenders regulated by the FCA. The Australian mortgage prisoner problem is a policy-created trap driven by APRA's serviceability buffer.

ASIC's MoneySmart defines mortgage stress as spending more than 30% of pre-tax household income on repayments. Mortgage prisoners are a sharper subset of that group. They are stressed, and they cannot access relief through refinancing.

The asymmetry is the crux: your existing lender can keep you on your current loan without reassessing you, but any new lender must apply the full buffer.

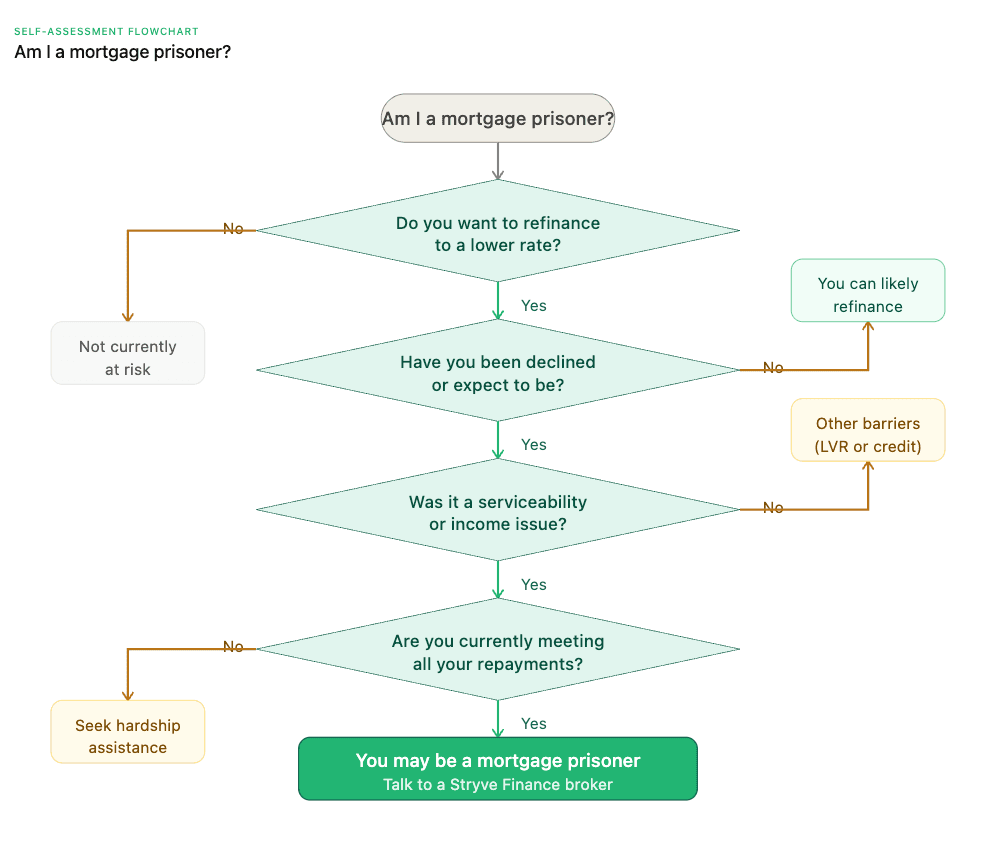

Work through the flowchart below to find out whether the mortgage prisoner problem applies to your situation.

If the flowchart points to ‘you may be a mortgage prisoner,’ the next section explains the exact regulatory mechanism that is trapping you, and why it is not your fault.

The APRA 3% serviceability buffer explained in plain English

When you apply for a new loan, including a refinance, the lender does not test whether you can afford the actual rate. They test whether you could afford a rate 3 percentage points higher. This is APRA's serviceability buffer. If you are searching for information on a serviceability buffer refinance, this is the mechanism you are dealing with. It is sometimes called the mortgage stress test in search results, though serviceability buffer is the correct regulatory term.

So if you are refinancing to a rate of 6.5%, the lender must assess you as though the rate were 9.5%. If your income cannot support repayments at 9.5%, the application fails. Even if you are comfortably paying 6.5% right now.

Worked example: how the buffer blocks a refinance. A borrower with a $600,000 loan on a 6.5% rate pays roughly $3,792 per month in principal and interest over a 30-year term. But the new lender must assess them at 9.5%. At that rate, repayments jump to approximately $5,048 per month. If the borrower's income cannot support $5,048, the application is declined. They are paying $3,792 without difficulty. They would continue paying $3,792 after the refinance. But the regulatory test says no.

The table below shows how this plays out across different loan sizes at a 6.5% rate (assessed at 9.5%):

| Loan size | Actual rate | Assessed rate | Actual repayment/mo | Assessed repayment/mo |

|---|---|---|---|---|

| $400,000 | 6.5% | 9.5% | $2,528/mo | $3,363/mo |

| $600,000 | 6.5% | 9.5% | $3,792/mo | $5,045/mo |

| $800,000 | 6.5% | 9.5% | $5,057/mo | $6,727/mo |

| $1,000,000 | 6.5% | 9.5% | $6,321/mo | $8,409/mo |

Figures based on 30-year P&I amortisation. Illustrative only. Actual repayments vary by lender and loan structure.

APRA introduced the 3% buffer in October 2021, raising it from 2.5%, to prevent borrowers from overextending in a low-rate environment. That made sense at the time. Rates were near historic lows and borrowing capacity was stretched.

But rates have risen significantly since then. The buffer has not been reduced. APRA confirmed in its 2023 and 2024 reviews that it would maintain the 3% buffer, citing macroeconomic uncertainty, even as the MBA and individual lenders lobbied for a reduction.

Under ASIC's responsible lending obligations in the National Consumer Credit Protection Act 2009, lenders must not provide credit that is unsuitable for the borrower. This is the regulatory foundation that makes lenders apply the buffer strictly. They have limited flexibility to approve refinances for borrowers who cannot pass the stress test.

Policy commentary: The 3% serviceability buffer was designed for a world of 2% interest rates. In a world of 6% to 7% rates, it forces borrowers to demonstrate they can afford repayments at 9% to 10%. The policy has not been recalibrated for the environment it now operates in, and the borrowers paying the price are the ones who can least afford it.

Why The Trap is Getting Worse in 2026

The serviceability gap is not static. It moves with rates. If rates remain elevated or rise further in 2026, the buffer rises with them. A borrower on 7% would need to qualify at 10%. The escape hatch gets smaller every time.

APRA has not signalled any intention to reduce the 3% buffer despite sustained industry lobbying from the MBA and individual lenders.

Search interest in “mortgage stress test” has risen significantly over the past 12 months, a direct signal that more borrowers are discovering the trap exists only after they have walked into it. If you are already feeling the weight of mortgage stress in Australia, the prisoner problem is the sharpest edge of that story.

The compounding effect is what makes this urgent. Every rate increase does not just raise your repayments. It raises the bar you need to clear to leave.

Who is most at risk of becoming a mortgage prisoner

Four borrower profiles are most exposed.

- Borrowers who took loans at the top of their capacity in 2021 or 2022 when rates were at historic lows. They qualified at the time, but the rate environment has shifted beneath them.

- Borrowers whose income has plateaued or reduced while rates have risen. This includes people who changed jobs, went part-time, or took a pay cut.

- Self-employed borrowers and contractors with variable income who struggle to demonstrate consistent serviceability on paper, even when their actual cash flow is strong.

- Single-income households after a life change such as parental leave, separation, or redundancy.

Two structural risk factors make the trap even harder to escape.

High LVR borrowers: If your loan-to-value ratio (LVR) is above 80%, you may be required to pay Lenders Mortgage Insurance (LMI) again when refinancing. LMI protects the lender, not you, and it can add thousands to the cost of switching. That is a financial barrier on top of the serviceability barrier.

Declining property values: If your property is worth less than when you bought it, your LVR has increased even if you have been paying down the loan. Less equity means a higher LVR, which means tighter lending criteria and potentially another round of LMI.

What Won't Work

Before we talk about what you can do, let's be honest about what will not help. Submitting multiple refinance applications without a strategy is counterproductive. Each application triggers a hard credit inquiry, which can reduce your credit score and make the next application harder.

AFCA can hear complaints if your lender has acted unfairly, but cannot compel a lender to approve a refinance or waive the buffer. Generic “shop around for a better rate” advice assumes you can pass the serviceability test. If you cannot, following it blindly can leave you worse off.

What You Can Actually Do if You're Stuck on a High Rate Mortgage

These are six genuine options. None of them are magic fixes. Each has trade-offs. But they are real pathways that work within the current regulatory framework.

- Negotiate a rate reduction with your current lender. Your existing lender does not need to reassess you under the buffer to adjust your current loan. Call their retention team and ask for a lower rate. They would rather keep you than lose you.

- Apply for a hardship variation. If repayments are genuinely unmanageable, your lender is obligated to consider a hardship application. This can include temporary payment reductions or restructured terms.

- Consolidate consumer debts into your existing mortgage. Credit cards, personal loans, and car loans often carry rates of 15% to 22%. A debt consolidation refinance rolls those higher-interest debts into your mortgage rate, which can meaningfully reduce your total monthly outflow. Even if you cannot switch lenders, your current lender may allow this restructure.

- Extend your loan term. Stretching from 20 remaining years to 30 reduces monthly repayments. The trade-off is more interest over the life of the loan.

- Switch to interest-only temporarily. This creates breathing room in the short term but delays equity building. Use it as a bridge, not a destination.

- Split your loan between fixed and variable. This manages rate exposure by locking in certainty on a portion while keeping flexibility on the rest.

Be clear-eyed about the trade-offs. A longer term means more total interest. Interest-only delays equity. Consolidation only helps if you do not re-accumulate consumer debt. But for borrowers who are stuck on a high rate mortgage with no path to refinance, these options can provide real relief.

If your credit file has already taken hits from missed payments or multiple applications, there are also specialist pathways for refinancing with bad credit.

Not sure if you're a mortgage prisoner or just need a better rate? A quick conversation with a Stryve broker can tell you where you stand. No credit check, no commitment.

Why a specialist broker is the highest-leverage move for a mortgage prisoner

Different lenders apply the APRA buffer differently within their own credit policies. Some have exception policies for refinancing borrowers with strong repayment histories and low LVRs. These exceptions are lender-by-lender and are not publicly advertised.

A Stryve Finance broker in Sydney with access to 50+ lenders knows which ones are most likely to engage with a tight serviceability file. The value is in knowing which doors to knock on and which to avoid, protecting your credit file from unnecessary hard inquiries.

Think of a specialist broker as a strategic navigator, not a salesperson. For mortgage prisoners, the broker's role is to identify whether any path out exists before a single application touches your credit file.

Stryve Finance is a specialist in self-employed and complex-income applicants, with full lender commission transparency so you know exactly how your broker is paid.

Choosing the right specialist refinance broker matters more for mortgage prisoners than for any other borrower segment. Here is what to look for.

Stryve brokers regularly work with tight serviceability files. We can run a no-application pre-assessment across 50+ lenders to identify whether any path out exists for you, without putting an application on your credit file until it is worth doing. Talk to a Stryve broker about your options.

Frequently Asked Questions About Mortgage Prisoners in Australia

What is a mortgage prisoner?

A mortgage prisoner is a borrower who is trapped on an uncompetitive rate with their current lender because they cannot pass the serviceability assessment required by a new lender. They are meeting all their repayments but are unable to refinance to a lower rate.

What does mortgage prisoner mean in Australia?

In Australia, a mortgage prisoner is specifically a borrower locked out of refinancing by APRA's 3% serviceability buffer, not by a closed-book lender as in the UK. The regulatory test for new lending is stricter than the test for keeping your existing loan, creating a trap for borrowers who are current on repayments but cannot qualify elsewhere.

Can I refinance if I can't pass the serviceability test?

It is difficult but not always impossible. Your existing lender can adjust your current loan without triggering a full reassessment. Some new lenders have exception policies for borrowers with strong repayment histories and low LVRs. A specialist broker can identify which lenders may consider your file.

What is the serviceability buffer in Australia?

APRA's serviceability buffer requires lenders to assess borrowers at their actual interest rate plus 3 percentage points. It was introduced at 3% in October 2021 and has not been reduced. A borrower applying at 6.5% must demonstrate they can afford repayments at 9.5%.

How do I escape mortgage prison?

Start by negotiating a rate reduction with your current lender, as they do not need to reassess you under the buffer. Consider debt consolidation, term extensions, or interest-only periods to reduce monthly outflow. Then speak with a Stryve Finance broker who can assess whether any lender on their panel has an exception pathway that fits your situation.

What is the difference between mortgage stress and being a mortgage prisoner?

Mortgage stress describes any borrower spending more than 30% of pre-tax household income on repayments. A mortgage prisoner is a sharper subset: they are stressed and cannot access relief through refinancing because they cannot pass the APRA serviceability test at a new lender. All mortgage prisoners are under financial pressure, but not all borrowers under pressure are mortgage prisoners. The distinction matters because the solutions are different.

General advice warning

This article provides general information only and does not constitute financial or credit advice. Consider your own circumstances and seek advice from a qualified mortgage broker or financial adviser before making any financial decisions.

Dylan Bertovic is the Director and Senior Finance Broker at Stryve Finance, specialising in non-traditional lending solutions. He helps clients across Australia with tiny home loans, construction finance, equipment and asset lending, refinancing, and investor loans. With deep expertise in self-employed and renovation mortgages, Dylan is known for crafting tailored strategies that get results