If you're lying awake at 3 am running numbers in your head, afraid to open your banking app, or carrying a quiet shame about how tight things have gotten, you're not imagining it. And you're not alone.

28.4% of Australian mortgage holders (over 1.5 million households) are now classified as “At Risk” of mortgage stress, according to Roy Morgan data for June 2025. That's the highest level since January 2025. The February Reserve Bank of Australia (RBA) rate decision rattled household budgets, and despite two cuts in early 2025, mortgage stress Australia data shows the pressure has not eased. Australian mortgage debt stress is now a national phenomenon, not a fringe concern. If you want to understand what the latest rate rise means for your mortgage, the short version is this: the pressure is real, it's structural, and it's not going away on its own.

Australians know it. Google searches for “mortgage stress australia” hit peak interest in 2025, up 40%. Searches for “australia mortgage stress suburbs data” surged an extraordinary 1,650%. People are googling their own financial pain in record numbers.

Most brokers chase rate-shoppers. Stryve Finance, a Sydney-based mortgage broker, exists for a different moment: helping borrowers who are already under pressure find the best available path across lenders nationwide. That starts with understanding exactly what mortgage stress is and whether you're in it.

What is Mortgage Stress?

Mortgage stress is most commonly defined as spending more than 30% of your gross household income on mortgage repayments and associated housing costs. This is the threshold used by the Australian Housing and Urban Research Institute (AHURI) and applied by the Australian Bureau of Statistics (ABS) Survey of Income and Housing.

A quick clarification: mortgage stress is not the same as housing affordability stress (the broader cost of housing relative to income) or rental stress (the same 30% threshold applied to renters). This article is specifically about your mortgage repayments and whether they're crushing your household budget.

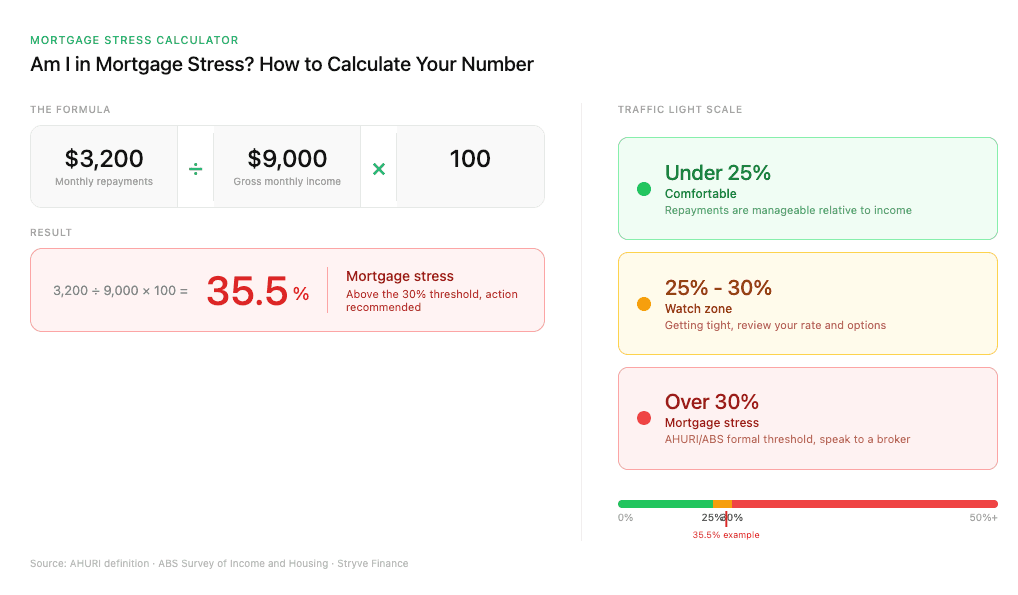

Here's a 60-second gut check you can do right now.

Your DIY mortgage stress calculator: 3 steps

- Find your monthly mortgage repayment (from your loan statement or banking app).

- Find your gross monthly household income (before tax, all earners in the household combined).

- Apply the formula: Monthly mortgage repayments ÷ gross monthly household income × 100

Here's what that looks like with real numbers, and where your result sits on the scale.

If your number lands in the amber or red zone, keep reading, the next sections explain exactly what's driving that pressure and which levers are available to bring it down.

If the result is above 30, you're in the zone that researchers formally classify as mortgage stress.

For example: $3,200 monthly repayment ÷ $9,000 gross monthly income × 100 = 35.5%. That's mortgage stress.

This is a rough guide, not a clinical diagnosis. But if the number makes your stomach drop, trust that feeling. You can run your numbers through our refinance calculator for a more detailed picture of where you stand and what might be possible.

Worth noting: the RBA cut rates twice in early 2025, but mortgage stress still rose in June. Why? Because borrowers took out larger mortgages following the cuts. Rate relief alone does not fix structural stress. Which raises the question: where is the pain concentrated?

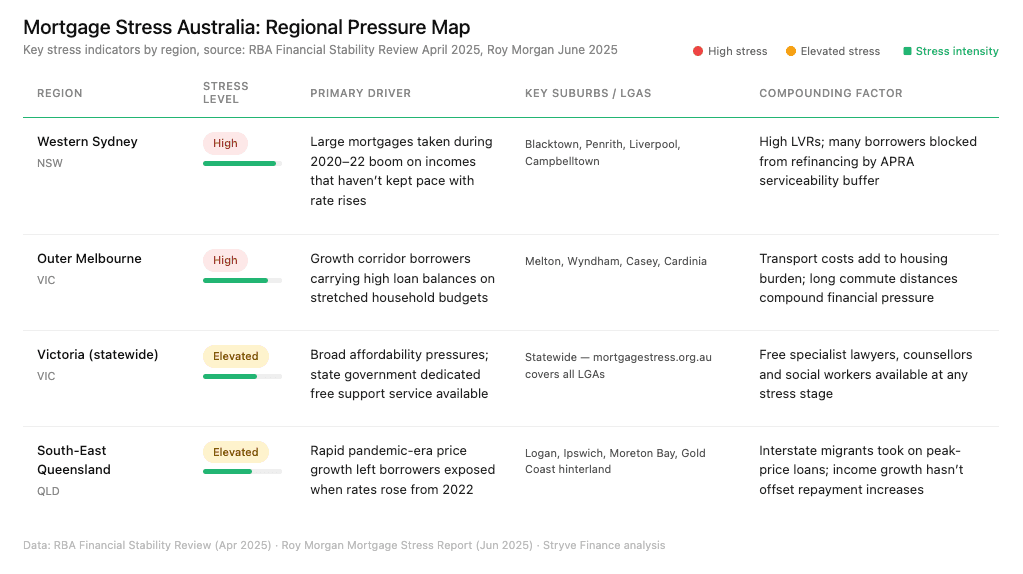

Where mortgage stress is hitting hardest across Australia

The RBA Financial Stability Review (April 2025) included a dedicated analysis on “Household financial stress across the regions.” The picture is uneven, and some areas are bearing far more weight than others.

The table below breaks down where that weight is falling hardest, by region, primary driver, and the suburbs most exposed.

Western Sydney carries the heaviest load, but as the data shows, the stress is structural across multiple corridors, and the compounding factors differ enough that the right response will depend on where you are and how your loan was structured.

Western Sydney remains one of the most acutely stressed corridors in the country. Mortgage stress in Sydney is concentrated in outer suburbs, including Blacktown, Penrith, Liverpool, and Campbelltown, where borrowers took on large mortgages during the 2020-2022 property boom and are now servicing those loans on household incomes that haven't kept pace with rate rises.

These LGAs consistently appear in the RBA's regional stress data as among the hardest hit in New South Wales. Outer Melbourne follows a similar pattern, with borrowers in growth corridors facing the double pressure of high loan balances and long commutes that add transport costs on top of housing costs. Parts of south-east Queensland, particularly areas that saw rapid price growth during the pandemic migration wave, are also flagged in the RBA's regional data.

Victoria deserves specific attention. Housing affordability pressures across the state have pushed a significant number of borrowers into stress, and the state has responded with a resource most people don't know about. Mortgagestress is a free, government-supported service that provides specialist lawyers, financial counsellors, and social workers to Victorians experiencing mortgage stress at any stage. That includes borrowers whose payments are still up to date and those who have already received court repossession orders. If you're in Victoria, this is a genuine lifeline.

The suburb-level search data tells its own story. The 1,650% surge in searches for suburb-specific stress data suggests Australians want to know whether their neighbours are struggling too. Roy Morgan's June 2025 figures confirm the trend is national: stress rose again even after two rate cuts, because the underlying debt loads haven't shrunk.

So what can you actually do about it?

Five mortgage levers you can actually pull right now

Mortgage stress articles love to tell you to “review your budget” or “cut back on takeaway.” That's not a strategy. These are the five structural levers that can genuinely change your monthly position, ranked by impact.

1. Refinance to a lower rate with a different lender

If you haven't reviewed your rate in the last 12 months, you're almost certainly paying more than you need to. A Stryve Finance broker can identify options your current bank will never mention. The common objection is cost. Here's the reality: what refinancing actually costs is often far less than the savings it unlocks over even the first year.

2. Consolidate your debts into the mortgage

This is the highest-leverage move for the largest group of stressed borrowers: those carrying credit card debt, personal loans, or car loans on top of the mortgage. Consider this: $30,000 in credit card debt at 20% interest costs roughly $500 per month in interest alone. Roll that into a mortgage at around 6%, and the interest cost drops dramatically. Yes, you're extending the repayment period on that debt. That's the trade-off. But if the alternative is defaulting on multiple obligations, consolidation buys you breathing room. You can consolidate your debts with a refinance and see what the monthly difference looks like for your situation.

3. Extend the loan term

Switching from 20 years remaining to 30 years reduces your monthly repayment significantly. The honest trade-off: you'll pay more interest over the life of the loan. But if the choice is between a higher total cost and losing your home, the maths is straightforward.

4. Switch to interest-only repayments temporarily

Some lenders allow a period of interest-only repayments (typically 1-2 years). This can cut your monthly obligation by 20-30%. The trade-off: you're not paying down principal, so your loan balance stays the same. This is a pressure valve, not a solution.

5. Request a hardship variation with your current lender

Every Australian lender is required to consider hardship applications. This can include reduced repayments, paused repayments, or restructured terms. It won't appear on your credit report as a default. It's a legitimate, regulated process.

The right lever depends on your situation. A Stryve Finance broker can assess all five options across 50+ lenders with full transparency on lender commissions and no hidden fees. Not sure if refinancing is right for you yet? That's a reasonable place to be. Start with the numbers.

Why the APRA Stress Test Blocks thousands of Borrowers from Refinancing

Here's the part that makes people furious once they understand it.

The Australian Prudential Regulation Authority (APRA) requires all lenders to assess borrowers at the loan interest rate plus 3 percentage points. This is the mortgage stress test. So a borrower on a 6.5% rate isn't assessed at 6.5%. They're assessed at 9.5%.

The cruel irony: the borrower who most needs a lower rate is often the one who can't pass the serviceability test to get it. You might be looking at a new lender offering 5.99%, which would save you hundreds per month. But because the assessment is run at 8.99%, your income doesn't clear the bar. You're stuck on the higher rate. Not because you can't afford the lower one, but because a regulatory buffer says you might not afford a hypothetical higher one.

This is a structural trap, not a personal failing. It has a name: mortgage prisoner. Some borrowers are genuinely locked in, and a Stryve Finance broker specialises in identifying lenders with policy exceptions or lower assessment rates. This is where access to a wide lender panel earns its value.

If this sounds like your situation, what to do if you can't refinance at all walks through the options that remain available.

Your 30-day Mortgage Stress Action Plan

Stop scrolling. Start here.

- Run the 30% stress calculation from earlier in this article. Monthly repayments ÷ gross monthly income × 100. Know your number.

- Gather three documents: your last three payslips (or tax returns if self-employed), your current loan statement, and a list of every debt you hold with its balance and interest rate.

- Talk to a broker before you talk to your bank. Your bank can only show you their own products. A Stryve Finance broker can search across lenders and find options your bank has no incentive to mention.

- Get a refinance assessment. This tells you whether debt consolidation, a rate switch, or a term extension is actually possible given your income, equity, and debt profile.

- If you can't refinance, ask your broker about hardship variations or lender policy exceptions. There are pathways even when the standard door is closed.

- If you're in Victoria, contact mortgagestress.org.au for free legal and financial counselling support. This service is available whether you're up to date on payments or already in arrears.

Do not wait for the next RBA decision. Rate movements remain uncertain and mortgage stress Australia data shows the underlying debt burden is not resolving on its own. The window to act is now, while lenders still have competitive offers on the table. A broker conversation costs nothing and carries no obligation.

Frequently Asked Questions About Mortgage Stress in Australia

What is mortgage stress?

Mortgage stress is most commonly defined as paying more than 30% of your gross household income on mortgage repayments and associated housing costs. This threshold is used by AHURI and the ABS Survey of Income and Housing. It is distinct from rental stress and broader housing affordability stress.

How do I calculate if I'm in mortgage stress?

Divide your monthly mortgage repayment by your gross monthly household income, then multiply by 100. If the result exceeds 30, you're in the zone formally classified as mortgage stress. For a more detailed assessment, use a refinance calculator to see what options might reduce that number.

What is the mortgage stress test in Australia?

APRA requires lenders to assess borrowers at the loan interest rate plus 3 percentage points. This means a borrower applying at a 6.5% rate is tested at 9.5%. The buffer exists to ensure borrowers can handle rate rises, but it also prevents many stressed borrowers from refinancing to a lower rate.

Can I refinance if I'm in mortgage stress?

In many cases, yes. A debt consolidation refinance can roll high-interest debts into your mortgage at a much lower rate, reducing your total monthly outgoings. However, the APRA serviceability buffer may block some borrowers. A broker with access to multiple lenders can identify exceptions.

What is mortgage stress in Victoria and where can I get help?

Victoria has a dedicated free service at mortgagestress.org.au, supported by the Victorian government. It provides specialist lawyers, financial counsellors, and social workers to borrowers at any stage of mortgage stress, from early difficulty through to court repossession proceedings.

Will refinancing cost me money I don't have?

Refinancing involves some costs, including discharge fees, application fees, and potentially valuation fees. But in many cases, the monthly savings from a lower rate or consolidated debts far outweigh the upfront costs within the first few months. A broker can map this out for you before you commit to anything.

Should I refinance or apply for a hardship variation?

Refinancing is a permanent structural change: you move to a better rate or consolidate debts to reduce your monthly obligations long-term. A hardship variation is a temporary relief measure offered by your existing lender, such as reduced or paused repayments, while your finances stabilise. If you can pass the APRA serviceability test, refinancing generally delivers more lasting benefit. If you cannot, a hardship variation is the faster, more accessible option and does not appear on your credit report as a default. In practice, many borrowers use a hardship variation as a bridge while they work toward a refinance. A Stryve Finance broker can assess which path is viable for your situation.

General advice warning

This article provides general information only and does not constitute financial or credit advice. It does not take into account your personal objectives, financial situation, or needs. Before acting on any information in this article, consider its appropriateness to your circumstances and speak to a qualified mortgage broker or financial adviser.

You don't have to figure this out alone

If you're reading this late at night, trying to work out whether your mortgage is still manageable, that takes courage. This is not where anyone planned to be. But it is a moment where the right conversation can change your trajectory.

A Stryve Finance broker is not a rate-shopping service. They help borrowers under pressure find the best available path, with full transparency on lender commissions and no hidden fees. That includes complex situations like self-employed income or multiple debts.

Talk to a Stryve Finance broker about your options. No obligation, no cost, no judgement. Just someone who can run the numbers across 50+ lenders and tell you what's actually possible for your situation.

Dylan Bertovic is the Director and Senior Finance Broker at Stryve Finance, specialising in non-traditional lending solutions. He helps clients across Australia with tiny home loans, construction finance, equipment and asset lending, refinancing, and investor loans. With deep expertise in self-employed and renovation mortgages, Dylan is known for crafting tailored strategies that get results