Navigating home loan products, cashback deals, and lender fine print takes real time. After multiple rate rises, choosing the right refinance home loan broker matters more than ever. That is exactly why roughly 75% of all new residential home loans in Australia are now written through mortgage brokers, according to Mortgage and Finance Association of Australia (MFAA) data.

The case for using a refinance home loan broker is strong. The ACCC found that existing borrowers paid an average of 0.26% more than new customers at the same bank, a loyalty tax that costs the average owner-occupier around $1,300 per year on a $500,000 loan. A good refinance home loan broker, like Stryve Finance in Sydney, exists to address that imbalance by accessing a wide panel of lenders and negotiating on your behalf.

But not every broker is equal. When you're choosing one, it comes down to three things: how many lenders they actually compare, how they get paid, and whether they'll explain the whole process clearly enough for you to make a confident decision.

This article gives you a specific checklist to vet any refinance home loan broker, a worked savings example, and the trust signals to look for. If you are still weighing whether refinancing makes sense, start with our guide on whether to refinance your home loan in 2026.

What is a refinance home loan broker?

A refinance home loan broker is a licensed credit professional who compares home loan products from a panel of lenders on your behalf, manages your application from assessment to settlement, and is legally required to act in your best interests under Australia's Best Interests Duty.

The Six Questions to Ask any refinance broker before you commit

Before you sign anything, ask these six questions. The answers will tell you whether a broker is genuinely working for you or just processing an application. The checklist below gives you everything you need in one place, screenshot it before your first broker call.

Here is what each question is designed to uncover, and what a good answer actually sounds like.

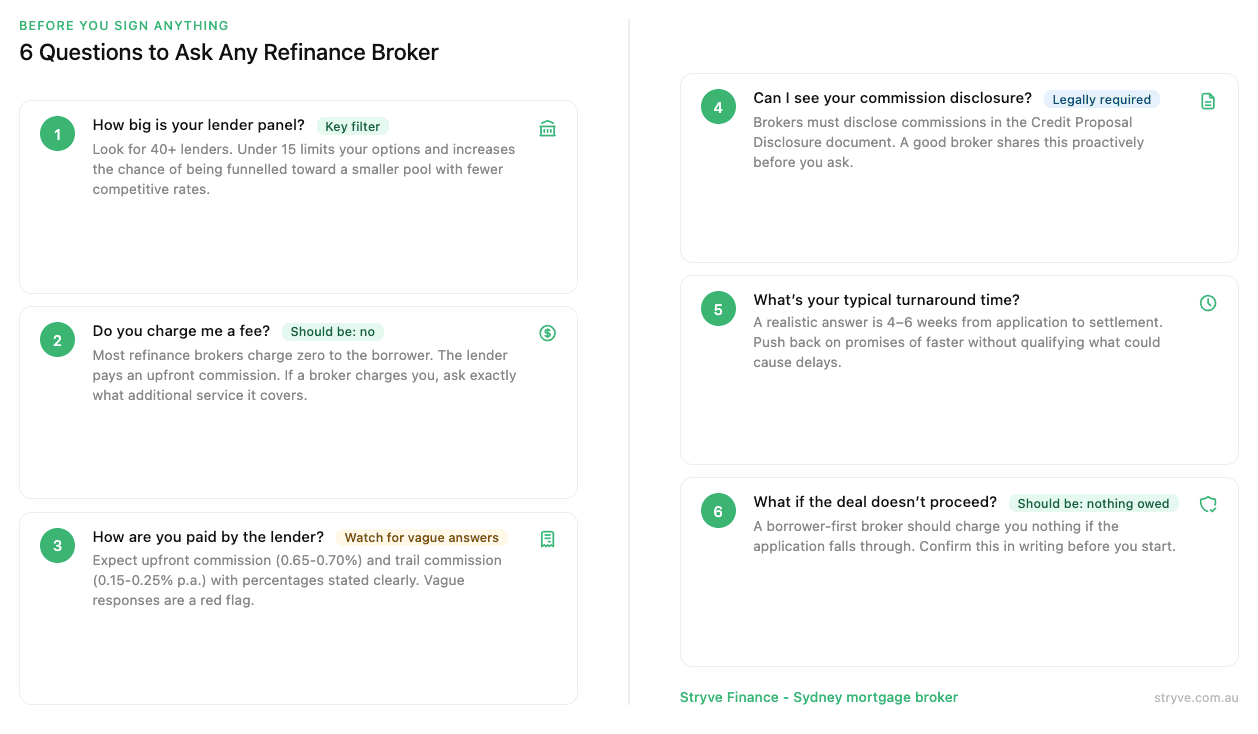

1. How big is your lender panel?

A panel of 50+ lenders gives a broker genuine comparison power. Anything under 15 limits your options and increases the chance you're being funnelled toward a smaller pool. A good broker should be able to walk you through how to compare refinance offers across their full panel, not just cherry-pick two or three.

2. Do you charge me a fee?

Most mortgage refinance brokers charge no fees to borrowers. The lender pays the commission. If a broker charges you a fee, ask exactly what additional service it covers and whether it's deducted from the commission or added on top.

3. How are you paid by the lender?

You want a straight answer here: upfront commission and trail commission, with the percentages stated clearly. Vague responses are a red flag.

4. Can I see your commission disclosure?

Brokers are legally required to disclose commissions in the Credit Proposal Disclosure document. This is not optional. A broker who proactively shares this information before you ask is one worth keeping on your shortlist.

5. What's your typical turnaround time?

A good broker will give you a realistic timeline, typically 4 to 6 weeks from application to settlement. If they promise faster without qualifying it, push back and ask what could cause delays.

6. What happens if the deal doesn't proceed?

You need to know upfront whether you'll owe anything if the application falls through. The answer from a borrower-first broker should be no.

Refinance Broker vs Bank

The refinance broker vs bank question deserves a direct answer. Here's how they compare on the things that actually matter.

| Factor | Refinance broker | Going direct to your bank |

|---|---|---|

| Lender panel | 50+ lenders compared | One lender, one product range |

| Fee transparency | Commission disclosed in writing | Margin built into the rate, not disclosed |

| Best Interests Duty | Yes, legally required since January 2021 | No, bank staff have no equivalent obligation |

| Negotiation leverage | Can play lenders off each other | Limited to internal retention offers |

| Application support | Broker manages all paperwork and lender communication | You handle it yourself |

To be fair, if your bank proactively offers you a genuinely competitive rate through their retention team, staying can make sense. But this is the exception. The ACCC's mortgage pricing inquiry found loyalty tax is the norm, not the outlier.

The real difference is accountability. Under the Best Interests Duty introduced via National Consumer Protection Act (NCCP) amendments effective January 2021, brokers are legally required to act in your best interests. Your bank has no such obligation.

How Refinance Brokers Get Paid

Understanding refinance broker fees starts with knowing who actually pays. In almost every case, the lender pays the broker. You pay nothing.

Here's how it works on a $600,000 loan:

- Upfront commission (typically 0.65% to 0.70% of the loan amount): $3,900 to $4,200, paid by the lender at settlement

- Trail commission (typically 0.15% to 0.25% per annum on the outstanding balance): $900 to $1,500 per year, paid by the lender for the life of the loan

Both must be disclosed in the Credit Proposal Disclosure document. This is a regulatory requirement, not a courtesy.

Now, the honest part. A conflict of interest can arise if a broker recommends a lender paying a higher commission over one offering a better deal for you. This is a real risk, not a theoretical one.

The safeguard is the Best Interests Duty (see the licensing section below). Stryve Finance goes further with full lender commission transparency and no hidden fees, making it easy to verify the recommendation rather than taking it on trust.

If a broker charges you a fee on top of the lender-paid commission, ask why. There may be a legitimate reason for complex scenarios, but for a standard refinance, you should not be paying out of pocket.

What Refinancing Actually Costs

Switching lenders is not free. But the costs are predictable, and a good broker will run this calculation with you in the first conversation.

Standard switching costs:

- Discharge fee from your existing lender (see our mortgage discharge fee guide): $150 to $400

- Application or establishment fee with the new lender: $0 to $600

- Government mortgage registration and transfer fees: $100 to $200 in most states

- Lenders Mortgage Insurance (LMI) if your new loan-to-value ratio (LVR) exceeds 80%: LMI is not transferable between lenders, so it may apply again

Worked example on a $600,000 loan with a 0.5% rate reduction:

| Item | Amount |

|---|---|

| Total switching costs | ~$800 |

| Annual interest saving | ~$3,000 |

| Net annual saving | ~$2,200 |

| Net saving over five years | ~$10,200 |

Some lenders also offer current cashback offers from lenders that can offset switching costs further. A broker with full market visibility will flag these for you, so you don't have to hunt for them.

A note on fixed-rate break costs. If you're currently on a fixed rate, break costs are calculated on the lender's economic cost of breaking the term. They can range from negligible to tens of thousands of dollars, depending on the remaining term and rate movements. These must be confirmed with your existing lender before proceeding. A good broker will get this number for you upfront so there are no surprises.

Book your free rate review with Stryve and see exactly what the numbers look like for your loan.

How to Check Your Broker is Licensed

Before engaging any broker, verify two things:

- Licensing: Every broker must hold an Australian Credit Licence or be an authorised credit representative under one. You can check this on the ASIC Connect professional register. It takes 30 seconds and confirms they're legally permitted to provide credit assistance.

- Best Interests Duty. Since January 2021, brokers are legally required to act in your best interests under the NCCP amendments. This replaced the older “not unsuitable” standard. It means your broker must demonstrate that their recommendation is the best option available to you from their panel, not just one that technically fits.

- Industry body membership. Membership of the MFAA (Mortgage and Finance Association of Australia) or FBAA (Finance Brokers Association of Australia) is an additional trust signal. It indicates ongoing professional development and adherence to a code of conduct. But it is not a substitute for the legal obligations above.

What "best refinance broker" actually means for your situation

There is no universal best refinance broker. The right one depends on your borrower profile.

If you're self-employed, you need a broker experienced with low-doc and alt-doc lending. Not every broker knows which lenders accept one year of financials or how to present irregular income favourably. Stryve Finance, for example, specialises in self-employed applicants and maintains broad access to lenders, which matters when mainstream banks decline applications that specialist lenders would approve.

If you're an investor or a mum-and-dad investor scaling a portfolio, you need someone fluent in loan structuring, tax-effective strategies, and cross-collateralisation risks.

If you're a straightforward PAYG refinancer, you need speed and panel breadth more than niche expertise.

Your quick mental checklist: does the broker have experience with your borrower type, do they have genuine full market comparison capability, and are they transparent about how they are paid? If the answer to all three is yes, you have found a good fit.

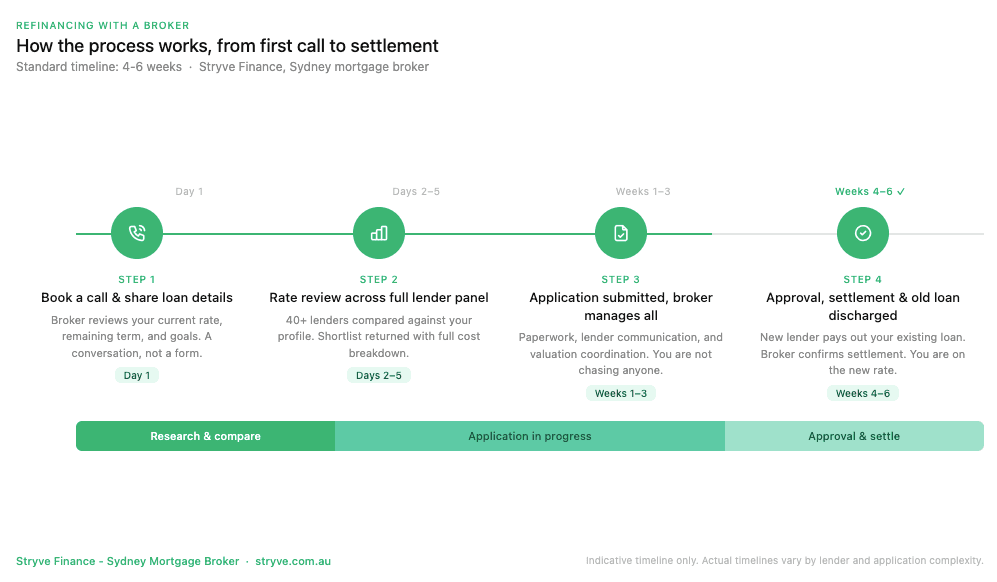

How the Refinance Process Works with a Broker

Here's what the process looks like from start to finish. The timeline below shows what happens at each stage and roughly how long each one takes.

Each step in the timeline maps to a specific action, here is what to expect at each one.

Step 1: Book a call and share your current loan details. Your broker reviews your existing loan, remaining term, current rate, and what you're looking to achieve. This is a conversation, not a form.

Step 2: Your broker runs a rate review across their full lender panel. They compare products against your specific situation and present your best options with a clear breakdown of costs, features, and savings.

Step 3: Application, approval, and settlement, managed by your broker. Once you choose a lender, your broker handles the paperwork, communication with the lender, and valuation coordination. At settlement, the new lender pays out your existing loan, and the transition is done.

Realistic timeline: Standard is 4 to 6 weeks from application to settlement. Digital-first brokers with streamlined processes, such as Stryve's model, which combines digital efficiency with human guidance, can tighten this. If your fixed rate is expiring, work backwards from that date and start the conversation early.

Start your free rate review with Stryve Finance and let your broker handle the rest.

Ready to Find Out What a Better Rate Looks Like?

You now know the three things that matter: panel size, fee transparency, and a broker willing to explain everything clearly. Stryve Finance, a Sydney-based mortgage broker, offers all three with access to 50+ lenders, zero borrower fees, and full lender commission disclosure.

This is not a sales call. It's a no-obligation rate review to see what's available for your specific loan.

Refinance with Stryve and book your appointment to see what a full market comparison can uncover for your loan.

Frequently Asked Questions

How much does a refinance broker charge?

Most refinance brokers charge no fees to borrowers. The lender pays the broker an upfront commission (typically 0.65% to 0.70% of the loan amount) and a trail commission (0.15% to 0.25% per annum). If a broker charges you a fee, ask what specific additional service it covers.

Is it better to refinance through a broker or a bank?

For most borrowers, a broker offers more value. Brokers compare a wide range of lenders, are bound by the Best Interests Duty, and manage the entire application. Banks offer a single product range and have no legal obligation to act in your best interests. If your bank proactively matches the market, staying can work, but that is the exception.

How do refinance brokers get paid?

Lenders pay brokers an upfront commission at settlement and an ongoing trail commission on the outstanding loan balance. These amounts must be disclosed in the Credit Proposal Disclosure document. The borrower typically pays nothing to the broker.

How long does refinancing take with a broker?

The standard timeline is approximately 4 to 6 weeks from application to settlement. Digital-first brokers with streamlined processes can reduce this. If your fixed rate is expiring, start the conversation early to allow enough lead time.

What should I look for in a refinance broker?

Look for a broad lender panel for genuine comparison, zero borrower fees, full commission transparency, and experience with your borrower type. Verify their Australian Credit Licence on the ASIC Connect register and confirm they operate under Best Interests Duty.

Should I use a broker or a financial adviser for refinancing?

These are different roles. A refinance home loan broker provides credit assistance by sourcing and structuring home loan products. A financial adviser provides financial advice, including broader wealth strategy, tax, and investment planning. For the mechanics of finding and applying for a new loan, you need a licensed broker. If you also want advice on how refinancing fits your broader financial goals, a financial adviser can work alongside the broker to address those questions.

General advice warning

This article provides general information only and does not constitute financial or credit advice. Consider your own circumstances and seek advice from a qualified mortgage broker or financial adviser before making any financial decisions.

Dylan Bertovic is the Director and Senior Finance Broker at Stryve Finance, specialising in non-traditional lending solutions. He helps clients across Australia with tiny home loans, construction finance, equipment and asset lending, refinancing, and investor loans. With deep expertise in self-employed and renovation mortgages, Dylan is known for crafting tailored strategies that get results