Most borrowers start their refinance search the same way. They Google “best home loan refinance rates,” scan the top results for home loan refinance offers, and fixate on the lowest advertised interest rate they can find. It feels logical. A lower rate means lower repayments, right?

Not always. The best home loan rates refinance seekers find are not always the ones with the lowest headline number. The advertised rate is just one number in a much bigger equation. Fees, loan features, cashback incentives, and even lender service quality all change the real cost of your loan over time. This guide, put together by Stryve Finance, a Sydney-based mortgage broker, helps you compare home loan refinance offers properly so you do not switch into a deal that looks cheaper on paper but costs more in practice.

The stakes are real. According to Moneysmart, there can be an interest rate difference of more than 2% between variable home loan rates available in the market. On a $500,000 loan over 25 years, that gap can translate to roughly $176,000 in extra interest paid over the life of the loan. And with the RBA adjusting the cash rate multiple times in recent months, more borrowers are feeling the squeeze and looking to switch.

But here is the thing: the RBA cash rate is not the only factor. Lenders set their own rates independently. So comparing home loan refinance offers means looking beyond the headline number.

This guide gives you a 6-factor comparison framework to evaluate any refinance offer properly: advertised rate, comparison rate, fees, cashback, features, and lender service quality. Use it to compare refinance home loans with confidence, whether you do it yourself or hand it to a broker.

Factor 1: Advertised interest rate, your starting point, not your answer

The advertised rate is the headline number lenders promote to get your attention. It is the starting point of any refinance home loan comparison, but it is never the full answer.

When you are comparing rates, you will see three main structures. Variable rates move with the market. Fixed rates lock in a rate for a set period. Split rates let you fix a portion and leave the rest variable. Each suits different situations. If you want certainty, fixed may appeal. If you want flexibility and the ability to benefit from future rate drops, variable is worth considering.

The key point is that rate alone does not account for fees or features. A lender offering 5.99% with $1,500 in annual fees may cost you more than one offering 6.15% with zero ongoing fees.

You can check current refinance rates across the market for specific numbers, but always read beyond the headline.

Factor 2: Comparison rate, what it tells you and where it misleads

What is a comparison rate?

A comparison rate is a single annual percentage that combines the interest rate with most fees and charges, calculated on a standardised $150,000 loan over 25 years.

Australia requires lenders to publish a comparison rate alongside their advertised rate. This is a single annual percentage that rolls the interest rate plus most fees and charges. It is designed to give you a more honest picture of the true cost.

And it does help. If one lender advertises 5.99% with a comparison rate of 6.45%, and another advertises 6.10% with a comparison rate of 6.15%, you can see immediately which loan carries heavier fees.

But here is the critical limitation most people miss. The comparison rate must be calculated on a standardised $150,000 loan over 25 years. That is the regulatory requirement. If your loan is $600,000, the fees that inflated the comparison rate are spread over a much larger balance, reducing their real impact. If your loan is $80,000, those same fees hit proportionally harder.

Use the comparison rate as a useful screening tool, not a final verdict. Always check the underlying fee schedule for your actual loan amount. The comparison rate gets you in the right ballpark. Your own numbers get you to the right answer.

Factor 3: Upfront and ongoing fees, the hidden cost of switching

Refinancing is not free. Before you commit to a switch, you need to know exactly what it will cost to move and how long it will take to recoup those costs.

The key switching costs to check:

- Discharge fee from your existing lender (to release your current mortgage, see our mortgage discharge fee breakdown)

- Application or establishment fee with the new lender

- Valuation fee if the new lender requires a fresh property valuation

- Lenders Mortgage Insurance (LMI) if your loan-to-value ratio (LVR) has changed and now exceeds 80%

Moneysmart recommends contacting your current lender first to negotiate a better rate before committing to a switch. If they will not budge, then you compare alternatives with full knowledge of the switching costs.

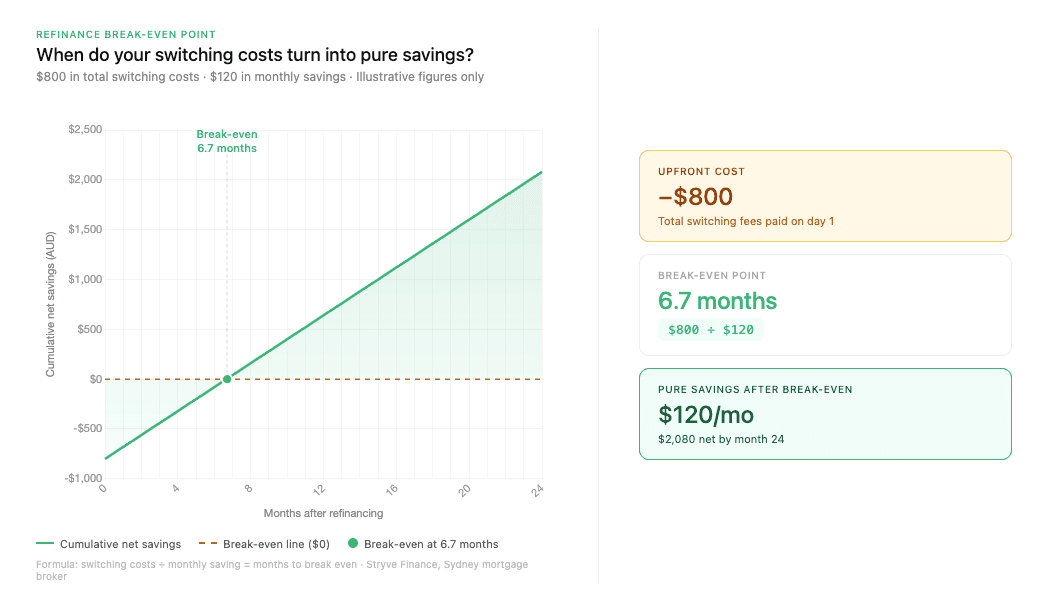

Here is a simple break-even calculation you can run yourself. Add up all the fees involved in switching. Divide that total by your monthly saving.

Worked example: Your total switching costs come to $800. The new loan saves you $120 per month. $800 ÷ $120 = 6.7 months to break even. Anything beyond that is pure saving. If you plan to hold the loan for years, that is a strong result. If you might move or refinance again within 12 months, the maths gets tighter.

The chart below traces exactly when that break-even point arrives and how the savings stack up after it.

That positive territory after month 6.7 is the entire point of refinancing, but only if you stay in the loan long enough to reach it, which is why timing matters as much as the rate gap itself.

Factor 4: Cashback offers, when they are worth it and when they are not

Cashback offers are everywhere in the refinance market right now. They are a legitimate comparison criterion. But they should never be the sole reason you switch.

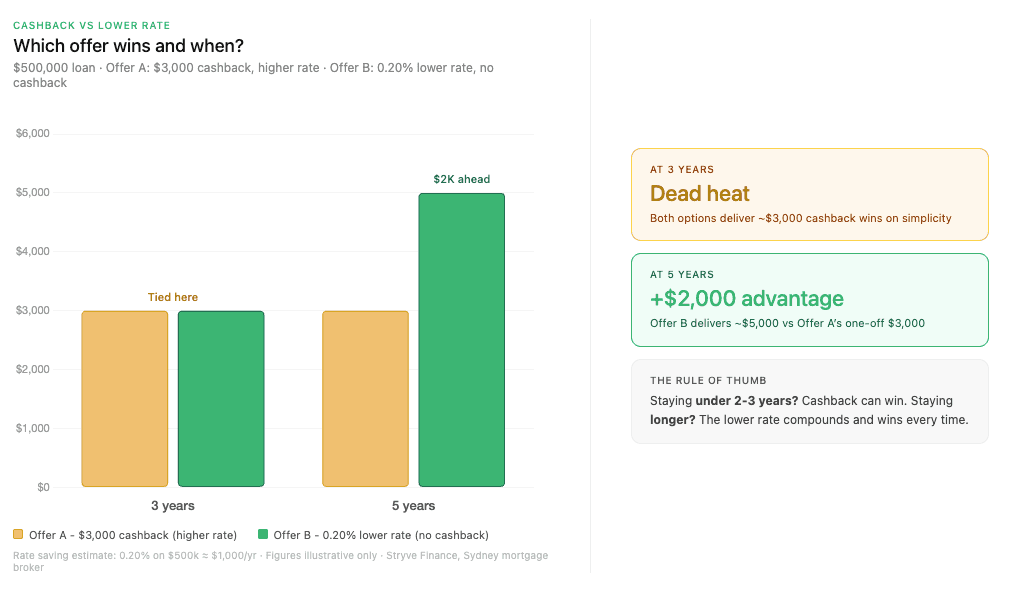

Here is why. Consider two offers on a $500,000 loan:

- Offer A: $3,000 cashback at a slightly higher rate

- Offer B: No cashback but a rate that is 0.20% lower

The chart below shows exactly where the two offers diverge, and why the timeline of your loan matters more than the cashback headline.

The lesson is clear in the data: at three years both offers are roughly equal, but every month beyond that the lower rate compounds further ahead.

Over 3 years, the rate reduction on Offer B saves you roughly $3,000 in interest, roughly matching the cashback. But over 5 years, that 0.20% lower rate saves you approximately $5,000 or more, clearly outweighing the one-off cashback payment.

The lesson is straightforward. Cashback rewards the short term. A lower rate rewards the long term. If you are confident you will refinance again within two years, cashback might be the winner. If you plan to stay put, the lower rate almost always delivers more value.

Cashback offers shift weekly in the current market. For a deeper look at what is available right now, check out current cashback offers and how to evaluate them. Just remember to weigh them as one factor in the framework, not the whole decision.

Factor 5: Loan features that actually matter

Not every loan feature is worth paying for. The trick is matching features to how you actually manage your money. For a deeper look at the two most-asked-about features, see our offset vs redraw comparison.

- Offset account: Links a savings or transaction account to your loan. You only pay interest on the loan balance minus the offset balance. Most valuable if you keep consistent savings in your everyday account.

- Redraw facility: Lets you access extra repayments you have made. Suits disciplined borrowers who regularly pay above the minimum and want a safety net.

- Extra repayments without penalty: Essential if you plan to pay down your loan faster. Some fixed rate loans restrict this.

- Split loan option: Lets you fix a portion of your loan and leave the rest variable. Useful if you want partial certainty without giving up all flexibility.

Here is the honest take. If you will not use an offset account, do not pay for one. A no-frills loan with a lower rate may beat a feature-rich loan every time for borrowers who just want the cheapest repayments. Match the features to your behaviour, not to a marketing brochure.

Factor 6: Lender service quality and settlement speed

This is the factor almost nobody talks about. But it can directly affect your wallet.

Settlement speed varies significantly between lenders. Some process a refinance in two to three weeks. Others take six weeks or longer. Every extra week you wait is another week you are paying your old, higher rate. If your monthly savings is $200, a four-week delay costs you roughly $200 in savings you will never get back.

Lender service quality also matters during the application process. Slow communication, lost documents, and unclear requirements create stress and delays.

This is where a broker adds genuine value. A broker who works across 50+ lenders has real-time insight into which are processing quickly and which are backlogged, and can steer you toward lenders that are not just offering good rates but actually settling loans on time. Stryve Finance, a Sydney-based mortgage broker, makes that visibility a standard part of every comparison.

Your Refinance Comparison Worksheet

Before you commit to any offer, line up at least three options side by side using this refinance comparison checklist:

| Factor | Offer 1 | Offer 2 | Offer 3 |

|---|---|---|---|

| Advertised interest rate | |||

| Comparison rate | |||

| Total switching costs (all fees) | |||

| Cashback amount | |||

| Key features (offset, redraw, extra repayments, split) | |||

| Lender service notes (settlement speed, reviews) | |||

| Break-even period (switching costs ÷ monthly saving) |

Fill this in for at least three offers before making a decision. Or hand it to a Stryve Finance broker who can complete it across their full lender panel and return a shortlist tailored to your situation.

Once you have your shortlist, plug your numbers into the refinance savings calculator to model exactly what each offer saves you over time.

See how much you could save with a refinance.

Should you compare refinance offers yourself or use a broker?

You absolutely can run this comparison yourself. The framework above gives you everything you need. But there is a practical ceiling on DIY comparison.

Most borrowers can realistically research and compare three to five lenders before the spreadsheet fatigue sets in. A Stryve Finance compares 50+. That is not a small difference when the best home loan refinance offers often come from lenders you have never heard of. Stryve Finance offers a 50+ lender panel covering major lenders, smaller specialists, and non-bank options, full commission transparency, no hidden fees, and specialist expertise for self-employed applicants whose income structures make standard comparisons more difficult.

Think of the broker not as a replacement for understanding how to compare refinance home loans, but as the mechanism that makes the 6-factor framework actionable at scale. You understand what matters. They run the numbers across a panel you could never access alone. If you are leaning toward working with a broker, here is a guide on how to choose the right refinance broker.

Get your personalised refinance comparison from a Stryve Finance broker.

Frequently Asked Questions About Comparing Refinance Offers

What is the best bank to refinance a home loan?

There is no single best bank to refinance a home loan. The best refinance home loan is the one that fits your loan size, features, and timeline. If you want the absolute lowest rate and do not need features, a no-frills lender with a stripped-back product may suit you. If you need an offset account and flexible repayment options, a lender with a full-featured loan is worth the slightly higher rate. If you need fast approval and settlement, the lender with the shortest current turnaround time wins. The right question is not “which lender is best?” but “which lender is best for my situation?”

How do I compare refinance home loans?

To compare refinance home loans, evaluate each offer across six factors: advertised rate, comparison rate, total switching costs, cashback, loan features, and lender service quality. Use the 6-factor framework from this guide for every offer, record them in the worksheet above, and calculate your break-even period before committing.

What are the best home loan refinance rates right now?

Rates change frequently, and the headline rate is only part of the picture. The comparison rate matters more because it includes most fees. For current data, check the latest refinance rates for 2026. Remember that with a 2%+ gap between the highest and lowest variable rates in the market, it is worth checking even if you think your current rate is reasonable.

Should I refinance to a fixed or a variable rate?

Choose fixed if you want repayment certainty and believe rates may rise further. Choose variable if you want flexibility, the ability to make unlimited extra repayments, and exposure to any future rate drops. A split loan, where you fix one portion and leave the rest variable, is a middle path that suits borrowers who want partial certainty without giving up all flexibility. A Stryve Finance broker can model all three structures with your actual numbers across multiple lenders before you commit.

Let a Stryve Finance Run the Comparison for You

You now have the framework. A Stryve Finance broker runs this exact 6-factor comparison across 50+ lenders as standard practice. The outcome is a shortlist of offers that genuinely fit your situation, with full commission transparency so you know exactly how the broker is paid. No hidden fees. No guesswork.

Book your free refinance comparison appointment and refinance through Stryve.

Dylan Bertovic is the Director and Senior Finance Broker at Stryve Finance, specialising in non-traditional lending solutions. He helps clients across Australia with tiny home loans, construction finance, equipment and asset lending, refinancing, and investor loans. With deep expertise in self-employed and renovation mortgages, Dylan is known for crafting tailored strategies that get results