If you bought your first home a couple of years ago and your repayments now feel heavier than you expected, you're not imagining things. This guide walks you through how home loan refinance rates work in 2026, helps you figure out whether refinancing actually makes sense for your situation, and gives you a clear picture of what the process looks like from start to finish.

No jargon. No pressure. Just the information you need to make a confident call.

Why Home Loan Refinance Rates Matter More Than Ever in 2026

The Reserve Bank of Australia (RBA) raised the cash rate again in February 2026, and if you're a first-home buyer who locked in a loan two or three years ago on a lower rate, you've likely felt the impact on your monthly repayments. Search interest in "home loan refinance rates" has been climbing steadily in recent months, which tells you plenty of Australians are in the same boat.

It's completely normal to feel the weight of that. You worked hard to get into the property market, and watching your repayments climb is stressful.

Here's the thing worth understanding: refinancing isn't just about chasing a lower rate. It's a strategic financial tool that can serve different goals depending on where you are in life. You might want to lower your monthly repayments, consolidate other debts into your home loan, access the equity you've built, or switch from an interest-only structure to a principal and interest structure. The best move depends on your situation, not a comparison table. That's what this guide is here to help you work through.

Should You Actually Refinance? A Quick Self-Assessment

Before you start comparing home loan refinance offers, it's worth asking yourself a few honest questions. You should consider refinancing your home loan if:

- Has your fixed rate period expired, or is it about to?

- Have you been on your current home loan for two or more years?

- Has your property value increased since you bought?

- Is your LVR (loan-to-value ratio, which is your remaining loan balance as a percentage of your property's current value) at or below 80%?

- Has your income increased or stabilised since you first applied?

- Are you paying a variable rate that's noticeably higher than the current rate?

If you ticked three or more, refinancing is worth exploring seriously. But it's not always the right move.

If you used the FHOG (First Home Owner Grant) when you purchased, your eligibility for refinancing isn't affected. The grant doesn't create any restrictions on switching lenders.

Staying put can make more sense if you're close to paying off your loan or still within a fixed-rate period where break costs would eat into any savings. Break costs on fixed-rate loans can be high. They're calculated based on the difference between your locked-in rate and the current wholesale rate, multiplied by your remaining fixed term. Ask your current lender for a break cost estimate before making any decisions.

It's also important to check your LVR before you apply. If refinancing pushes your LVR above 80%, you may need to pay LMI (Lenders Mortgage Insurance, a one-off premium that protects the lender if you default). LMI premiums typically range from $5,000 to $20,000 depending on loan size and LVR, so it's a critical number to check before you proceed.

If you don't know the answers to all of these questions, that's completely normal. A broker can help you fill in the gaps. In the meantime, you can plug your numbers into our refinance home loan calculator to see what potential savings might look like.

Best Home Loan Refinance Rates in Australia Right Now

Searching for the "best home loan refinance rates" will give you dozens of comparison tables, but here's what most of them won't tell you: the best refinance home loan for your neighbour might be a terrible fit for you.

Competitive variable rates for refinancers currently range and shift depending on your LVR, loan size, and whether you're an owner-occupier or an investor. Fixed rates vary further based on term length. Rather than fixating on a single headline number, focus on the comparison rate.

What is a comparison rate? A comparison rate is a single percentage that includes the interest rate plus most fees and charges, giving borrowers a more accurate picture of a loan's true cost. According to ASIC's MoneySmart guidance, comparison rates give you a truer picture of the total cost than the advertised rate alone. A home loan refinance rate of 5.89% with high ongoing fees can cost you more than a rate of 6.05% with minimal fees. Always compare apples with apples.

When people search for the best bank to refinance home loan, they often expect a single answer. Honestly, there's no single best lender. The right one depends on your borrowing profile, property type, income structure, and goals. This is where working with a mortgage broker like Stryve Finance, with access to 40+ lenders, gives you a genuine advantage over walking into one bank and hoping for the best. Stryve Finance brokers will also show you exactly what commission they earn from each lender they recommend, so you know the recommendation is transparent.

What About Cash Back Home Loan Offers?

You've probably seen lenders advertising cash-back home loans, where they offer you a lump sum (often $2,000-$4,000) to refinance with them. It sounds appealing, but these offers need careful evaluation.

Cash back offers have been shrinking across the market as lenders tighten margins following rate hikes. The ones that remain often come with clawback clauses. This means if you refinance again or close the loan within a set period (typically 2-4 years), you'll need to repay some or all of the cashback.

Now factor in the typical costs of refinancing in Australia, set out in the table below. These can add up to $1,800 or more, which can erode or even exceed a cashback offer.

| Cost Item | Typical Range |

|---|---|

| Discharge fee | $150 - $400 |

| Application fee | $0 - $600 |

| Valuation fee | $0 - $300 |

| Settlement fee | $200 - $500 |

| Total refinancing costs | $550 - $1,800+ |

| Minus typical cashback offer | -$2,000 to -$4,000 |

A lower home loan refinance rate over the life of your loan will almost always save you more than a one-off cashback payment. Calculate the total cost of the new loan over two to three years, subtract the cashback, and compare that against a loan with a genuinely lower rate and fewer fees. That's the real comparison.

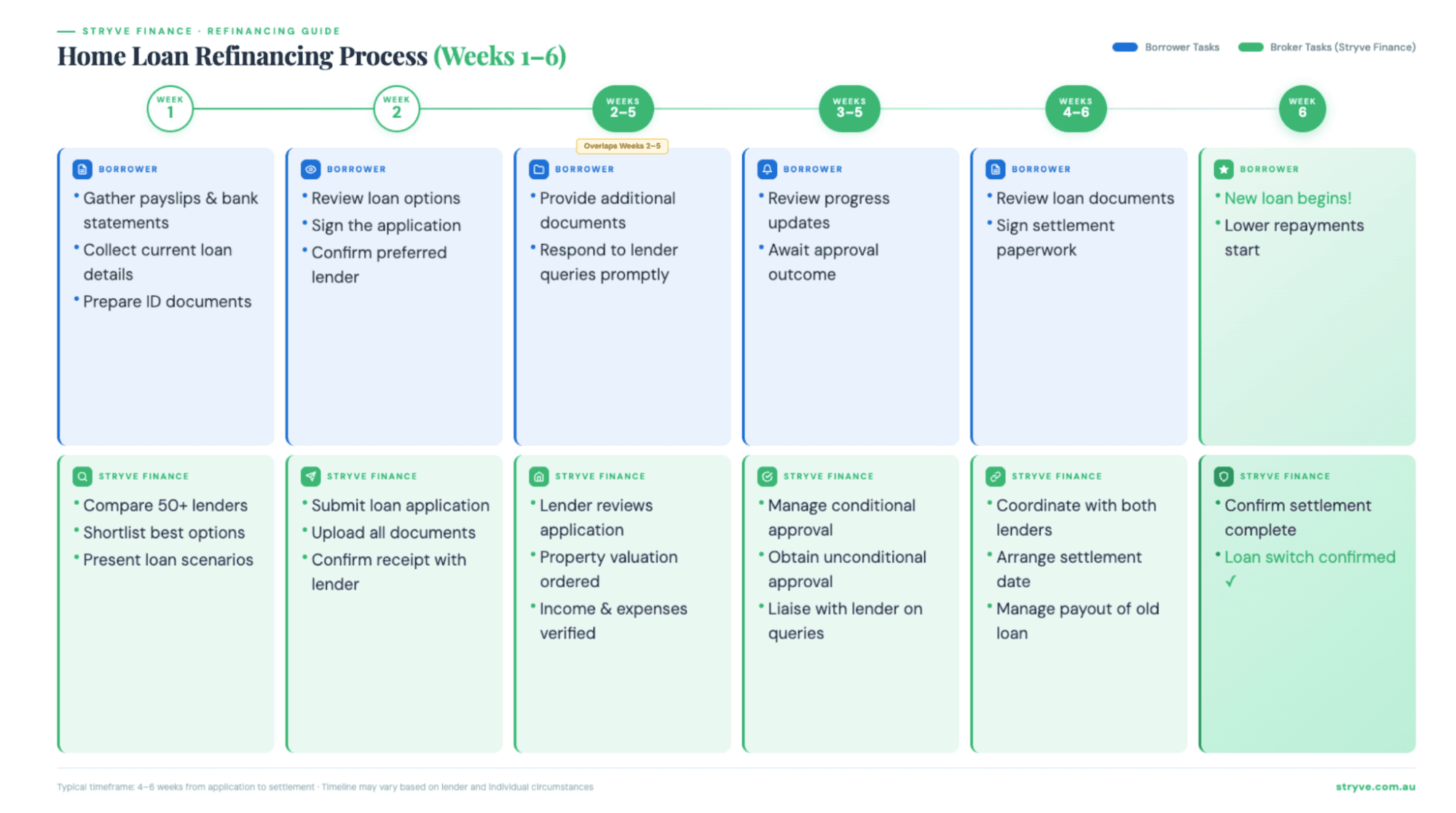

The Refinancing Process: What Actually Happens Week by Week

One of the biggest barriers to refinancing is simply not knowing what to expect. Here's a realistic week-by-week breakdown of how it works. The typical timeframe is 4-6 weeks from application to settlement.

- Week 1: Gather documents and compare options: You'll need recent payslips, bank statements, your current loan details, and ID. Your broker does the heavy lifting here, comparing options across lenders and presenting you with a shortlist. Your job is mainly paperwork.

- Week 2: Submit your application: Your broker lodges the application with the chosen lender. You sign the forms. Most of this is handled digitally now.

- Weeks 2-5: Assessment, valuation, and approval: The lender reviews your application, verifies income and expenses, and orders a property valuation. You'll typically receive conditional approval first, then unconditional approval once everything checks out.

- Weeks 4-6: Settlement and switchover: The new lender pays out your old loan and your new loan begins. Your Stryve Finance broker coordinates this with both lenders. You'll receive confirmation once it's done.

It's worth knowing that if you're shopping around, submitting multiple refinancing applications within 14 days is generally treated as a single inquiry on your credit file, so comparing a few options won't hurt your credit score.

Will I Actually Get Approved? Common Refinancing Eligibility Concerns

The fear of being rejected is real, and it keeps many people from even starting the process. But refinancing approval criteria can actually work in your favour compared to when you first applied.

You now have a repayment track record, you've likely built equity in your property, and your income may have grown. CoreLogic data shows Australian home values rose around 8% nationally between 2022 and 2024, meaning many first-home buyers have gained meaningful equity. These factors all strengthen your refinancing position.

That said, applications do get knocked back. The most common reasons are:

- Insufficient equity (LVR above 80%, triggering LMI requirements that many borrowers want to avoid)

- Changed employment status, such as moving from full-time to contract work

- Increased debt levels since your original application

- Property valuation is coming in lower than expected

If you're self-employed, know that specialist pathways exist. Lenders who focus on self-employed applicants assess your financials differently, often using one or two years of tax returns or BAS statements rather than traditional payslips. A Stryve Finance broker experienced with self-employed borrowers can match you directly with these lenders.

Understanding all costs upfront, with no hidden fees, is part of the process. If something doesn't stack up, a good broker will tell you honestly rather than push you into a loan that doesn't make sense.

Three Real Scenarios Where Refinancing Made Sense

Scenario 1: The expired fixed rate. A couple purchased their first home in 2023 on a two-year fixed rate. When it rolled onto the lender's standard variable rate, their repayments jumped by over $400 a month. After factoring in discharge and settlement fees totalling approximately $800, they switched to a new lender with a lower variable rate and saved $280 per month, netting over $2,500 in the first year alone.

Scenario 2: Removing LMI and consolidating debt. A single buyer who originally purchased with a 90% LVR had built enough equity over three years to bring their LVR below 80%. They refinanced to a new lender, avoided LMI entirely on the new loan, and rolled a $15,000 car loan into their home loan at a much lower interest rate. Their total monthly repayments across all debts decreased, and they simplified their finances into a single payment.

Scenario 3: The self-employed borrower. A freelancer was limited to a small pool of lenders when they first bought, resulting in a higher rate. Two years later, with a stronger trading history and two full years of tax returns, they qualified for a mainstream lender at a significantly better home loan refinance rate. Total refinancing costs were around $1,200, recouped within four months through lower repayments.

For investment properties, it's worth noting that refinancing costs may be tax-deductible under ATO guidance. Check with your accountant to understand what applies to your situation.

Want to see what your own numbers look like? You can run your own numbers through our refinance calculator.

Should I Refinance to a Fixed or Variable Rate in 2026?

With the RBA cash rate at 4.35% as of early 2026, the choice between fixed and variable comes down to your appetite for certainty versus flexibility. A fixed rate locks in your repayment for a set term, typically one to five years, which is useful if you're budgeting tightly. A variable rate moves with the market and usually allows extra repayments and offset accounts without penalty.

For most refinancers in 2026, variable rates have been more competitive at the point of switching, but fixing a portion of your loan can give you a hedge if further rate rises are a concern. A Stryve Finance broker can model both scenarios against your loan balance and timeline so you can compare the numbers directly.

Your Next Step: Find Out What You Could Save

You've done the research, and that puts you ahead of most people. Here's what it comes down to: don't chase the lowest headline rate. Factor in all costs. Think about what you actually need from your home loan right now. And get advice tailored to your situation, not a generic comparison table.

Stryve Finance brokers have access to 40+ lenders, do the comparison work for you, and will show you exactly what commission they earn from each recommendation. No guesswork. No hidden agendas.

If you're ready to find out what refinancing could look like for you, book a free refinancing assessment with Stryve Finance. It's a no-obligation conversation, not a sales pitch. Just a clear picture of your options so you can make a confident decision.

Dylan Bertovic is the Director and Senior Finance Broker at Stryve Finance, specialising in non-traditional lending solutions. He helps clients across Australia with tiny home loans, construction finance, equipment and asset lending, refinancing, and investor loans. With deep expertise in self-employed and renovation mortgages, Dylan is known for crafting tailored strategies that get results