The Reserve Bank of Australia (RBA) just raised interest rates, and if you're trying to buy your first home, you're probably wondering what this means for you. At Stryve Finance, we've been fielding this question from clients all week. The interest rate rise Australia saw on February 4, 2026, has real implications for your borrowing power, your repayments, and your timeline. But it also comes with a clear set of actions you can take right now.

Here's everything you need to know, broken down by your stage in the buying journey, with the steps our Stryve Finance brokers are recommending right now.

The RBA just Raised Rates to 3.85% - Here's What Actually Happened

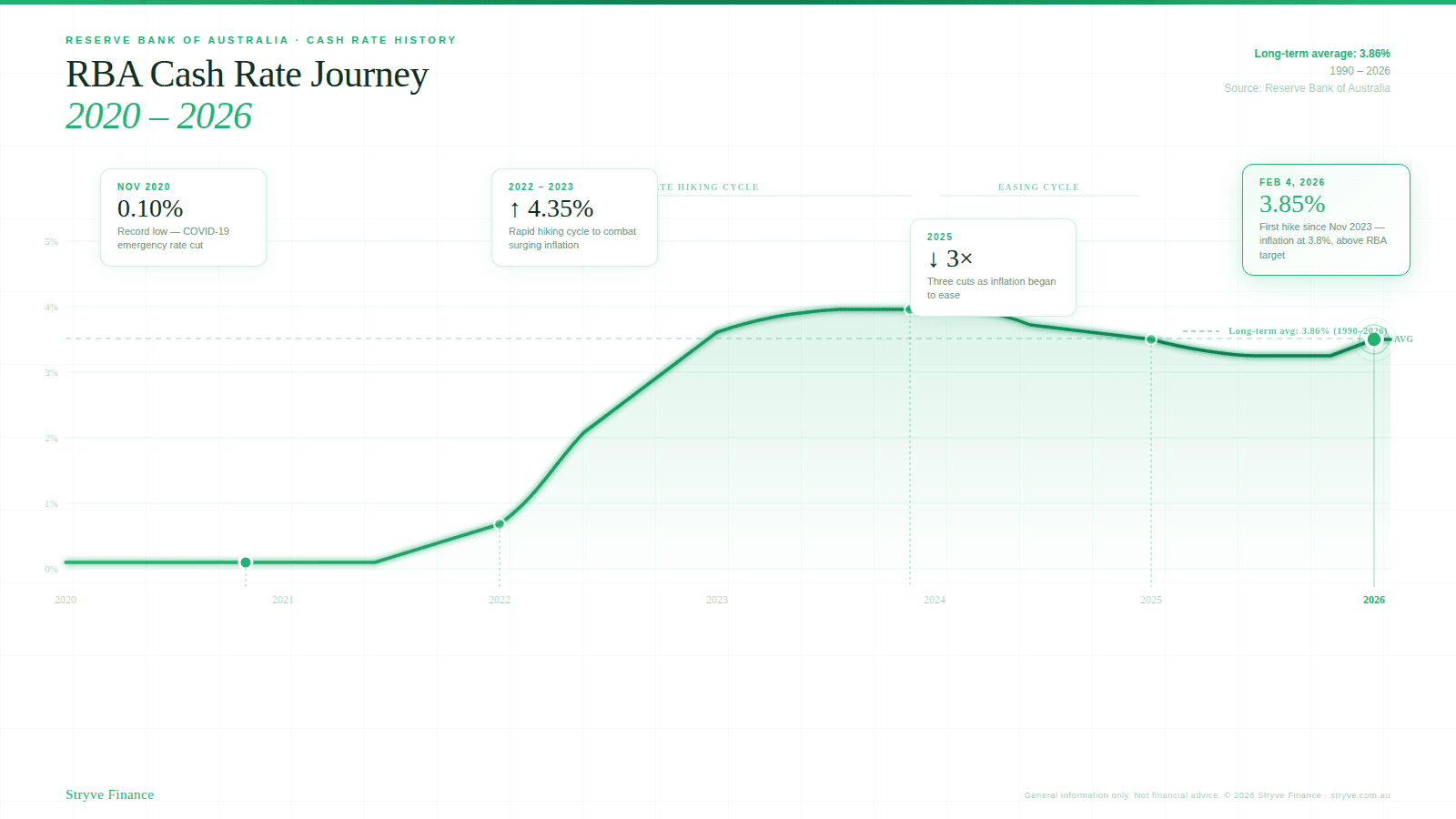

On February 4, 2026, the RBA raised the cash rate by 0.25% to 3.85%. This is the first rate rise since November 2023, reversing one of the three cuts made in 2025.

Why did they do it? Inflation. The latest figures show inflation sitting at 3.8% as of January 2026, well above the RBA's target band of 2-3%. The RBA's board stated that inflation is likely to remain above the target band “for some time,” and they needed to act to bring it back under control.

For context, the cash rate has averaged 3.86% from 1990 to 2026. So while this rate feels high compared to the record-low 0.10% we saw in November 2020, it's actually right around the long-term average. The era of ultra-cheap money was the exception, not the norm.

So how does the cash rate affect your mortgage? The cash rate is the interest rate at which banks lend to each other overnight. When it goes up, banks' costs go up, and they typically pass that increase on to you through higher variable mortgage rates. Your actual home loan rate will be the cash rate plus your lender's margin, which usually ranges from 1.5% to 2.5%, depending on the lender and your loan profile.

That margin is where lender choice really matters, especially for first home buyers who may not realise how much variation exists between providers. At Stryve Finance, we compare rates across 50+ lenders to make sure you're not paying more than you need to.

How CBA, NAB, ANZ and Westpac Responded to the Rate Rise

Not every bank responds to an RBA interest rate rise in the same way, or at the same speed. Here's how the big four have moved following the February decision.

| Bank | Rate passed on | Effective date |

|---|---|---|

| CBA | Full 0.25% | February 18, 2026 |

| NAB | Full 0.25% | February 14, 2026 |

| ANZ | Full 0.25% | February 21, 2026 |

| Westpac | Full 0.25% | February 18, 2026 |

The CBA, NAB, and ANZ interest rate rises all passed on the full 0.25%. But notice the different effective dates. If you're comparing lenders, those timing gaps matter for your repayments.

Here's the thing most first home buyers miss: the big four aren't your only options. Smaller lenders and non-bank lenders sometimes absorb part of the increase, or offer sharper rates to win new business. As a Stryve Finance client, you get access to loan options from 50+ lenders so you can see what's actually competitive right now, not just what the big four are advertising.

The forward outlook also matters for your lender decision. More on that in the section below.

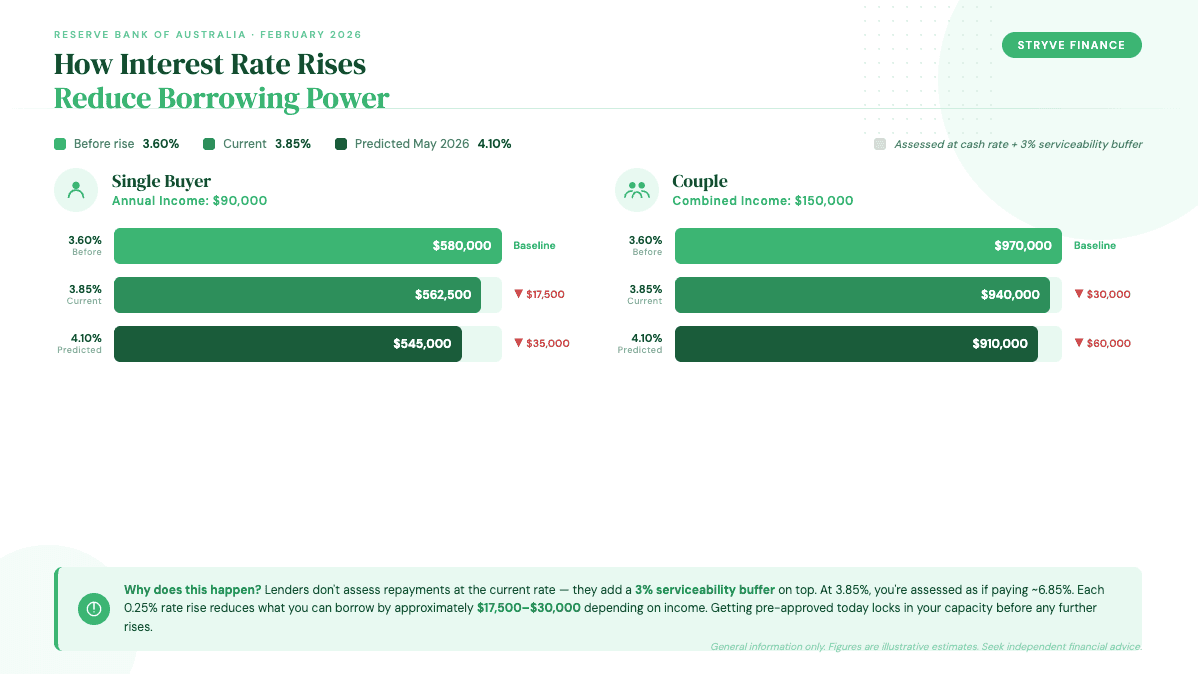

What this Rate Rise Means for Your Borrowing Power

This is where the interest rate news hits home. When the cash rate rises, your borrowing capacity drops. Here's why.

Banks don't assess your ability to repay at the current rate. They add a buffer, typically 3%, on top. This is called the serviceability buffer, and it's designed to make sure you can still afford your repayments if rates climb further.

At a cash rate of 3.85%, and assuming a typical lender margin, your mortgage rate might be around 6.10-6.35%. But the bank assesses you as if you're paying roughly 6.85% or higher. That's a meaningful difference when it comes to how much they'll lend you.

Worked example:

A single buyer earning $90,000 per year might see their maximum borrowing capacity drop by approximately $15,000 to $20,000 compared to where it stood before the February hike. For a couple earning $150,000 combined, the reduction could be in the range of $25,000-$35,000.

If the predicted May 2026 hike goes ahead, the assessment rate could rise towards 7.10%, squeezing borrowing power further.

This doesn't mean your plans are derailed. It means your numbers have shifted, and knowing your exact position puts you back in control. The best next step is to check your updated borrowing power with our free calculator.

Check how the rate rise affects your borrowing power with the calculator above. It takes two minutes and gives you a clear starting point.

Could Another Rate Rise Hit in May 2026?

Three of four major banks are predicting another 0.25% hike at the May 2026 RBA meeting. Will there be another interest rate rise? The honest answer is: probably, but it's not locked in.

The RBA has been clear that its approach is “data-dependent.” That means future moves hinge on incoming economic data, particularly inflation figures and employment numbers. If inflation starts trending down convincingly, the board may hold. If it stays sticky, they'll likely act again.

The next RBA meeting is March 17, 2026, with the announcement at 2:30 pm AEDT. Most economists expect a hold in March, with May being the more likely date for any further movement.

Here's what you can control: your own preparation. You can't influence the RBA's decision, but you can lock in your borrowing position now before any potential further tightening. A Stryve Finance pre-approval, assessed at today's rates protects your capacity for the next three to six months, covering you through the May decision window, with no upfront fees.

Fixed vs Variable: Which Makes More Sense Right Now?

This is one of the most common questions after any rate movement, and there's no single right answer.

Variable rates move with the cash rate. You get flexibility, including the ability to make extra repayments and access offset accounts. But you're exposed if rates keep climbing.

Fixed rates lock in your repayment amount for a set period, usually one to five years. You get certainty, which is valuable when rates are rising. But if rates drop later, you're stuck paying the higher amount unless you break the loan (which comes with costs).

| Option | Pros | Cons |

|---|---|---|

| Variable | Flexibility, extra repayments, offset accounts | Exposed if rates keep rising |

| Fixed | Repayment certainty; protection from further rises | Stuck if rates fall; break costs apply |

| Split | Certainty on part of the loan, flexibility on the rest | More complex to manage |

One important detail: fixed rates are priced based on where banks expect rates to go, not where they are today. If banks are predicting a May hike, that expectation is likely already baked into current fixed rate offers.

A practical middle ground is splitting your loan. Part fixed for certainty, part variable for flexibility. This is exactly the kind of conversation our Stryve Finance brokers have every day, modelling the numbers across 40+ lenders to find a structure that fits your situation, with no hidden fees.

Government Schemes That Help Offset Rising Rates

When borrowing power gets squeezed, government schemes become even more valuable.

Here are the key ones for first home buyers.

The First Home Guarantee allows eligible buyers to purchase with as little as a 5% deposit without paying Lenders Mortgage Insurance (LMI). This means you can buy with a loan-to-value ratio (LVR) of up to 95%. LMI can run into tens of thousands of dollars, so avoiding it frees up significant cash. This scheme is administered through the National Housing Finance and Investment Corporation.

The Help to Buy scheme provides a government equity contribution, reducing the amount you need to borrow. A smaller loan means lower repayments, which directly offsets the impact of higher rates.

The First Home Owner Grant (FHOG) varies by state and territory but typically provides a lump sum for eligible buyers purchasing new or substantially renovated homes. Check your state's revenue office for current amounts and eligibility.

These schemes exist specifically to keep the door open when conditions tighten. Eligibility criteria apply. The Stryve Finance team checks scheme eligibility as part of every first home buyer consultation, at no cost to you.

Your Action Plan Based on Where You Are Right Now

Your next move depends on where you sit in the buying journey. Here are four clear paths.

- Still saving your deposit. Reassess your target deposit and timeline using the borrowing capacity calculator. Your borrowing power has shifted, which may change the deposit you need or the price range you're targeting. Factor in the possibility of a May hike when setting your numbers.

- Ready to buy. Pre-approval is the single most powerful move you can make right now. It locks in your assessed borrowing capacity at today's rates, and a typical pre-approval is valid for three to six months. That means getting approved now covers you through the predicted May 2026 decision. Get your Stryve Finance pre-approval before rates move again and give yourself certainty while the market shifts.

- Already pre-approved. Check whether your pre-approval amount has been affected by the February hike. Some lenders reassess automatically, others don't. Contact your Stryve Finance broker to confirm your numbers still work for the properties you're looking at.

- Under contract or settling. Your rate is likely locked for settlement, but it's worth reviewing your loan structure with your broker. If you're on a variable rate, discuss whether a partial fix makes sense given the forward outlook. Self-employed first home buyers should also confirm all documentation is current, as lenders can be particularly thorough during rate-tightening cycles.

Thousands of first-home buyers purchase in rising-rate environments every year. Working with a Stryve Finance broker means you go in prepared, knowing your numbers, your best lender options, and exactly what to do next.

What about refinancing if you already have a home loan?

If you already own a property and landed here searching for interest rate news, this section is for you.

Refinancing after a rate rise can be a smart move, particularly if your current lender passed on the full 0.25% increase but competitors didn't. It's also worth investigating if you've been on the same loan for a few years and suspect you're paying a “loyalty tax”: a higher rate than what new customers are being offered.

The key is comparing like-for-like across enough lenders to know whether switching actually saves you money after accounting for any discharge or application fees. You can read more in our guide to refinancing after a rate rise.

Frequently Asked Questions about the 2026 rate rise

Will there be another interest rate rise in 2026?

May 2026 is flagged as the likely date for a further move, with current bank forecasts leaning toward another 0.25% increase. The decision will depend on incoming inflation and employment data over the next few months.

How much did CBA, NAB, ANZ and Westpac raise their rates?

All four major banks passed on the full 0.25% increase. Effective dates varied: NAB from February 14, CBA and Westpac from February 18, and ANZ from February 21, 2026.

When is the next RBA meeting?

The next RBA meeting is on March 17, 2026, with the rate decision announced at 2:30 pm AEDT. Most economists expect a hold in March, with May 2026 being the more likely date for any further movement.

How does the rate rise affect my borrowing capacity?

With the cash rate at 3.85%, banks assess your repayment ability at approximately 6.85% (current rate plus the 3% serviceability buffer). This reduces how much you can borrow compared to when rates were lower.

Should I lock in a fixed rate now?

It depends on your circumstances. Fixed rates offer certainty if you believe rates will keep rising, but they're already priced with expected hikes factored in. A split loan (part fixed, part variable) can offer a balanced approach. Book a free consultation with a Stryve Finance broker to model the right structure for your situation.

This article was written by the Stryve Finance team. It provides general information only and does not constitute financial advice. Credit licensing details available at stryve.com.au. Consider your own circumstances and seek independent advice before making financial decisions.

Dylan Bertovic is the Director and Senior Finance Broker at Stryve Finance, specialising in non-traditional lending solutions. He helps clients across Australia with tiny home loans, construction finance, equipment and asset lending, refinancing, and investor loans. With deep expertise in self-employed and renovation mortgages, Dylan is known for crafting tailored strategies that get results