You locked in a fixed rate that made perfect sense at the time. Now circumstances have changed, and you are staring down the cost of leaving early. If the number your lender quoted on your home loan break costs has caught you off guard, you are not alone. Break costs can be genuinely confronting, and understanding what drives them puts you back in control.

What are home loan break costs?

Home loan break costs are the amount a lender charges to recover lost interest income when you exit a fixed-rate loan before the fixed term ends. They are calculated based on the gap between your contracted rate and the current wholesale rate, and can range from a few hundred dollars to tens of thousands depending on your loan size, remaining term, and rate movements since you locked in.

Home loan break costs are not a penalty fee. They represent the lender's recovery of lost interest income. When you fix your rate, the lender locks in wholesale funding to match. If you exit early, the lender calculates the economic loss created by the gap between your contracted rate and the current wholesale rate. That loss becomes your break cost.

A common point of confusion: exit fees on new variable-rate loans were banned by the Australian Government from 1 July 2011. But fixed rate home loan break costs were explicitly excluded from that ban and remain lawful. The Australian Financial Complaints Authority (AFCA) confirms that break fees on fixed-rate loans represent the lender's actual economic loss. They are not capped by regulation, which means they can be substantial.

Break costs can be triggered by:

- Repaying the loan in full before the fixed term ends

- Refinancing to another lender

- Switching from fixed to variable rate with your current lender

- Selling the property during the fixed term

- Making lump-sum repayments above your annual threshold

- Porting the loan to a new property (if your lender does not permit it)

If you are weighing up whether to exit your fixed loan entirely, our guide to refinancing a fixed-rate home loan covers the strategic decision in full. Stryve Finance, a Sydney-based mortgage broker, can also run the numbers across 50+ lenders before you commit to any move.

How the Break Cost Calculation Actually Works

Here is the break cost calculation in plain English. The formula has four moving parts:

Break cost formula

(Your fixed rate minus the current wholesale rate) × remaining loan balance × remaining fixed term in years

The result is then discounted to present value. Let's define each variable.

Your fixed rate is the rate locked into your loan contract. The current wholesale rate is the bank bill swap rate for a term matching your remaining fixed period. This is not the RBA cash rate and not the advertised variable rate. It is the rate at which banks lend to each other in wholesale markets. Your remaining loan balance is what you still owe. The remaining fixed term is the time left on your fixed period, expressed in years or fractions of years.

Here is the critical caveat for any break fee fixed mortgage calculation: lenders use their own internal funding rates, not publicly quoted wholesale rates. AFCA notes that lenders are not always required to disclose the precise formula they use. This means your estimate using a fixed home loan break cost calculator will always be approximate. Only your lender can provide the exact figure.

That said, running the numbers yourself gives you a ballpark. And a ballpark is exactly what you need to sense-check what your lender quotes you.

The formula also explains why break costs move in one direction for some borrowers and the opposite direction for others. Moneysmart confirms the directional relationship: the more rates have fallen since you locked in, the higher the break fee. The more rates have risen above your fixed rate, the lower the break cost, and it can even approach zero.

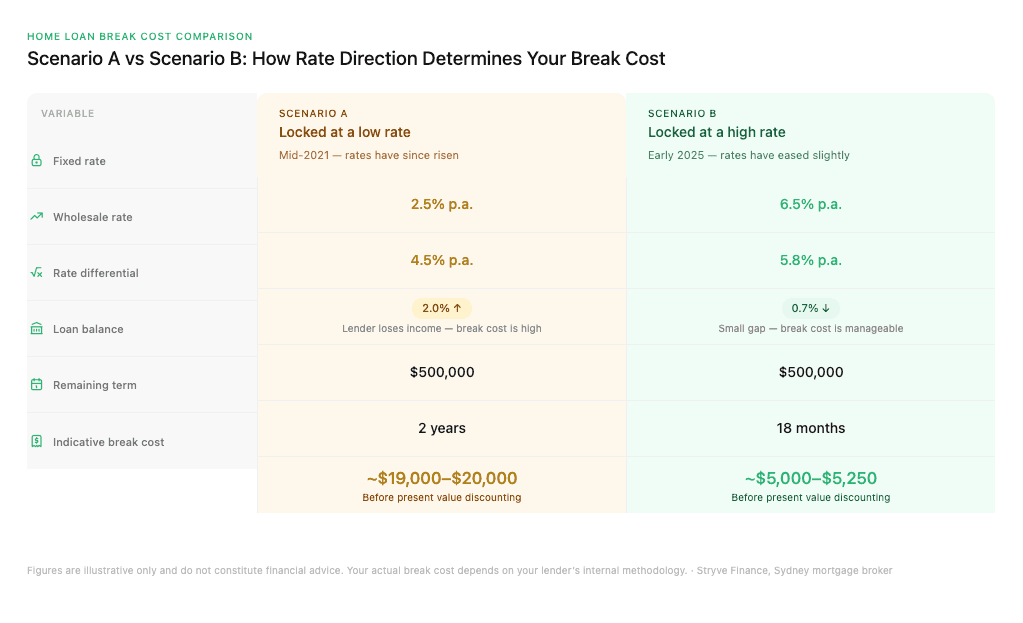

Worked Example 1: Locked at a Low Rate, Facing a High Break Cost

Scenario A: You took out a $500,000 loan fixed at 2.5% in mid-2021. You have two years remaining on the fixed term. The current comparable wholesale rate for a two-year term is 4.5%. These examples are for illustrative purposes only and do not constitute financial advice. Your actual break cost will depend on your lender's internal methodology.

Here is the arithmetic, line by line:

- Rate differential: 4.5% minus 2.5% = 2.0%

- Annual cost to the lender: 2.0% × $500,000 = $10,000 per year

- Multiplied by remaining term: $10,000 × 2 years = $20,000 before present value discounting

The present value discount reduces this slightly, but the indicative break cost sits around $19,000 to $20,000. Borrowers who locked at record lows during 2020 and 2021 are the group most likely to face large break costs in 2025 and 2026. Wholesale rates have risen significantly since then, creating a wide differential.

Important: this is a ballpark estimate. Your lender's internal wholesale rate and discounting method will produce a different exact figure, so use this to sense-check a quote rather than as a precise prediction.

Worked Example 2: Locked at a High Rate, Break Cost May be Minimal

Scenario B: You took out a $500,000 loan fixed at 6.5% in early 2025. You have 18 months remaining. The current comparable wholesale rate for an 18-month term is 5.8%.

The arithmetic:

- Rate differential: 6.5% minus 5.8% = 0.7%

- Annual cost to the lender: 0.7% × $500,000 = $3,500 per year

- Multiplied by remaining term: $3,500 × 1.5 years = $5,250 before present value discounting

The indicative break cost here is roughly $5,000 to $5,250. A much more manageable figure. The key asymmetry: when rates sit close to or above your fixed rate, the differential shrinks, and break costs can be modest or even negligible.

The table below puts both scenarios side by side so the asymmetry is impossible to miss.

The loan balance is identical in both cases, the entire difference in break cost comes down to which direction rates moved after you locked in.

The direction and size of rate movement since you locked in determines whether breaking is expensive or cheap. Your home loan break cost calculator estimate depends entirely on this differential.

See what you could save by refinancing your fixed-rate loan. A Stryve Finance broker in Sydney can model the full picture, including the break cost offset, across 50+ lenders.

Why Your Break Cost Quote Expires so Quickly

Lender break cost quotes are typically valid for just one business day. That is because they are tied to wholesale market rates that move with every trading session.

The practical implication: the break cost figure you receive today may be different tomorrow. If you are planning to refinance, request a fresh quote as close to your intended settlement date as possible. Build a buffer into your modelling to account for daily fluctuations.

Timing matters when deciding when to refinance. A few days of wholesale rate movement can shift your break cost by hundreds or even thousands of dollars on a large loan balance.

What Changes Your Break Cost Figure

Several factors can move your break cost up or down beyond the headline rate differential. Prepayments during the fixed term. Most lenders allow $10,000 to $30,000 per year in extra repayments without triggering a break cost. Exceed that threshold and you may trigger partial break costs on the excess amount.

- Redraw activity: If you have redrawn funds, your effective loan balance may differ from what you expect. This changes the base figure in the calculation.

- Split loans: If you have a split loan with part fixed and part variable, only the fixed portion attracts a break cost. The variable portion can be refinanced freely at any time.

- Porting your loan: Some lenders allow you to port your fixed rate to a new property if you are selling and buying simultaneously.

This can help you avoid break costs entirely. Check your lender's policy before assuming you will face a charge.

Break Costs Are Just One Piece of the Switching Puzzle

Break costs can dominate your thinking, but they are one of several costs involved in switching lenders. You may also face discharge fees, application fees, valuation fees, and potentially LMI (Lenders Mortgage Insurance, required when borrowing more than 80% of the property value).

The smart approach is a break-even analysis. Calculate how many months of interest savings at the new lower rate you need to recoup the total switching costs, including the break cost. If you recover the costs within 12 to 18 months and plan to hold the loan for years beyond that, breaking may make strong financial sense.

Optimising break costs in isolation can lead to poor decisions. The question is not just “how much does it cost to leave?” but “does refinancing a fixed-rate home loan save me more than the total cost of switching?”

Get a personalised refinance quote from a Stryve Finance broker to see the full cost-versus-savings picture.

How to Sense-Check Your Lender's Break Cost Quote

Your lender may not disclose the precise formula behind their quote. But you can still use the formula structure above to generate a ballpark and compare.

Run the numbers using publicly available bank bill swap rates for your remaining term. If your estimate and the lender's quote land in the same range, the quote is likely reasonable. If there is a large unexplained gap, say your estimate is $8,000 and the lender quotes $18,000, you have grounds to ask questions.

Request a written breakdown of how the figure was calculated. Ask which wholesale rate was used and for what term.

If you believe a break fee has been incorrectly calculated or applied, you have the right to complain to AFCA. AFCA can investigate whether the fee reflects the lender's actual economic loss. This is a genuine consumer protection pathway, not a theoretical one.

Checklist: What to Ask Your Lender When Requesting a Break Cost Quote

Use this checklist when you call your lender or ask your broker to request the figure on your behalf:

- What is the current break cost figure for my fixed-rate loan?

- How long is this quote valid? (Expect one business day.)

- What calculation method and wholesale rate did you use?

- Have my recent prepayments or redraw activity been factored in?

- Can I do a partial break if I have a split loan?

- What is the discharge process and timeline?

- Can you provide this quote in writing?

Always get the quote in writing so you have a record. A Stryve Finance broker can request this on your behalf, interpret the result, and compare it against the potential savings from switching.

Stryve Finance brokers are transparent about how they are paid, so the advice sits genuinely in your corner.

Let a Stryve Finance Do the Break Cost Maths for You

Stryve Finance brokers can request indicative break cost figures from your current lender and model the full switch maths before you commit to anything. The result is a clear comparison: your break cost alongside the potential savings across 50+ lenders, laid out so the decision makes itself.

No hidden fees. No guesswork. If you have complex income, such as self-employed earnings, Stryve Finance specialises in structuring applications that lenders actually approve.

For the full picture on exiting a fixed loan, read our guide to refinancing a fixed-rate home loan. Talk to a Stryve Finance broker about your break cost options.

Frequently Asked Questions About Home Loan Break Costs

How is a break cost calculated on a fixed home loan?

The lender applies the formula: (your fixed rate minus the current wholesale rate) multiplied by your outstanding balance and remaining fixed term, then discounted to present value. See the full methodology and worked examples in the calculation section above.

Break costs vs early repayment fees: what is the difference?

They are often used interchangeably but refer to the same thing on fixed-rate loans. The important distinction is with exit fees on variable-rate loans, which the Australian Government banned from 1 July 2011 for new loans. Break costs on fixed-rate loans were explicitly excluded from that ban and remain fully lawful. If you are on a variable rate, you cannot be charged a break cost when you exit. If you are on a fixed rate, you can.

Can I avoid break costs on a fixed loan?

You can avoid break costs by waiting until your fixed term expires. Some lenders also allow you to port your fixed rate to a new property. Staying within your annual prepayment threshold (typically $10,000 to $30,000) avoids triggering partial break costs on extra repayments.

Are break costs tax deductible?

Break costs may be deductible for investment properties as a borrowing expense. They are generally not deductible for owner-occupied homes. Consult a registered tax professional for advice specific to your situation.

What happens to break costs if I sell my house?

Selling your property during the fixed term triggers break costs in the same way refinancing does. The lender loses the remaining interest income, and the break cost formula applies. Factor this into your selling costs if you are considering an early sale.

Can I negotiate a break cost with my lender?

Break costs are calculated based on the lender's actual economic loss, so there is limited room for negotiation on the figure itself. However, you can negotiate other aspects of the switch, such as discharge fees, or ask your new lender for cashback offers that offset the total cost of moving.

Dylan Bertovic is the Director and Senior Finance Broker at Stryve Finance, specialising in non-traditional lending solutions. He helps clients across Australia with tiny home loans, construction finance, equipment and asset lending, refinancing, and investor loans. With deep expertise in self-employed and renovation mortgages, Dylan is known for crafting tailored strategies that get results