Credit card balances are sitting at record highs. Multiple rate rises have squeezed household budgets to the point where mortgage stress is hitting harder than ever. And for thousands of Australians juggling two or three debts at once, the search for relief has become urgent.

If you have landed here, you are probably weighing up whether a debt consolidation home loan, a personal loan, or doing nothing is the smartest move. A debt consolidation home loan lets you roll high-interest debts into your mortgage at a lower rate, but the total cost depends heavily on your loan term and discipline. This guide, put together by Stryve Finance, a Sydney-based mortgage broker, is built to help you make that call with real numbers rather than marketing promises.

It is not a pitch. Moneysmart advises consumers to avoid companies making unrealistic promises about debt consolidation, and we agree. So instead of burying the risks, we will lead with them. You will see the real numbers, including the total interest trap most lender pages conveniently leave out.

How Debt Consolidation Actually Works

In plain English, debt consolidation means replacing multiple debts (credit cards, personal loans, car loans) with a single loan at a lower interest rate. You end up with one repayment instead of three or four.

There are two main paths. The first is rolling your debts into your home loan through refinancing. The second is taking out a separate personal loan to pay them off. Moneysmart defines this as replacing or extending an existing loan with funds from the same or a different financial institution.

Here is what consolidation does not do: erase your debt. It restructures it. And as the National Debt Helpline explicitly states, rolling all debts into one loan may result in paying more under the new arrangement than the original loans. The total cost depends entirely on the rate, term, and fees of whatever you switch into. According to ASIC's guidance on credit and loans, borrowers should always compare the total cost of credit, not just the headline rate. The detailed numbers are in the total interest trap section below.

Credit Card Debt: The Number One Reason Australians Consolidate

Most Australians searching for a credit card debt consolidation loan are carrying somewhere between $15,000 and $25,000 across one or more cards at rates north of 20% p.a. That is the scenario where consolidation makes the biggest difference, so let us use it as our worked example throughout this guide.

The minimum repayment trap on $20,000 at 21% p.a.:

If you only pay the minimum on a $20,000 credit card balance at 21% p.a., you could be looking at around 30 years to clear the debt, with approximately $34,000 in total interest paid, often exceeding the original balance itself. (Figures are illustrative, based on a 2% minimum repayment assumption; actual results will vary by lender and repayment behaviour.)

That is not a typo. The minimum repayment structure on most credit cards is designed to keep you paying for as long as possible.

Now the question becomes: which consolidation path actually saves you money? A debt consolidation home loan at a lower rate, or a personal loan with a fixed end date? The answer is not as straightforward as the rate alone suggests.

Debt Consolidation Home Loan vs Personal Loan

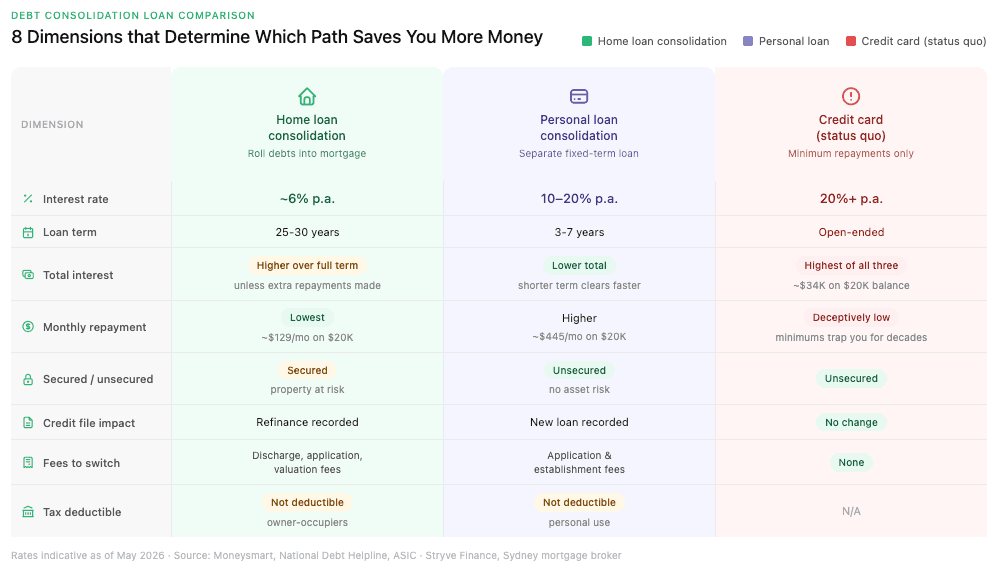

This is the debt consolidation loan comparison most lender pages will not give you.

Here are the eight dimensions that matter when you compare debt consolidation loans side by side.

The infographic below puts all eight dimensions side by side so you can see at a glance where each path wins, where it costs you, and what the status quo is actually doing to your finances.

The trade-off is clear in the data: the home loan path gives you the lowest monthly repayment but the highest total interest unless you make extra repayments, while the personal loan path costs more each month but forces the debt to zero in a fraction of the time.

| Dimension | Home loan consolidation | Personal loan consolidation | Credit card (status quo) |

|---|---|---|---|

| Interest rate range | ~6% p.a. | 10 to 20% p.a. | 20%+ p.a. |

| Loan term | 25 to 30 years | 3 to 7 years | Open-ended |

| Total interest paid | Higher over full term (unless extra repayments made) | Lower total due to shorter term | Highest of all three |

| Monthly repayment | Lowest | Higher | Varies (minimums are deceptively low) |

| Secured vs unsecured | Secured against your property | Typically unsecured | Unsecured |

| Credit file impact | New loan or refinance recorded | New loan recorded | No change |

| Fees to switch | Discharge, application, valuation fees | Application and establishment fees | None |

| Tax deductibility | Not deductible for owner-occupiers | Not deductible for personal use | Not applicable |

Rates shown are indicative as of May 2026 and may vary by lender and borrower profile. Consult a Stryve Finance broker for a personalised comparison based on current market rates.

The trade-off is clear. The home loan path gives you a lower rate but stretches the debt over decades. The personal loan path costs more per month but clears the debt faster with less total interest in many scenarios.

The National Debt Helpline identifies three key risks of the home loan path specifically: a longer repayment period increases total interest, secured debt replaces unsecured debt (increasing asset risk), and fees and charges on the new loan may outweigh savings.

Neither path is automatically better. It depends on your numbers, your equity, and your discipline.

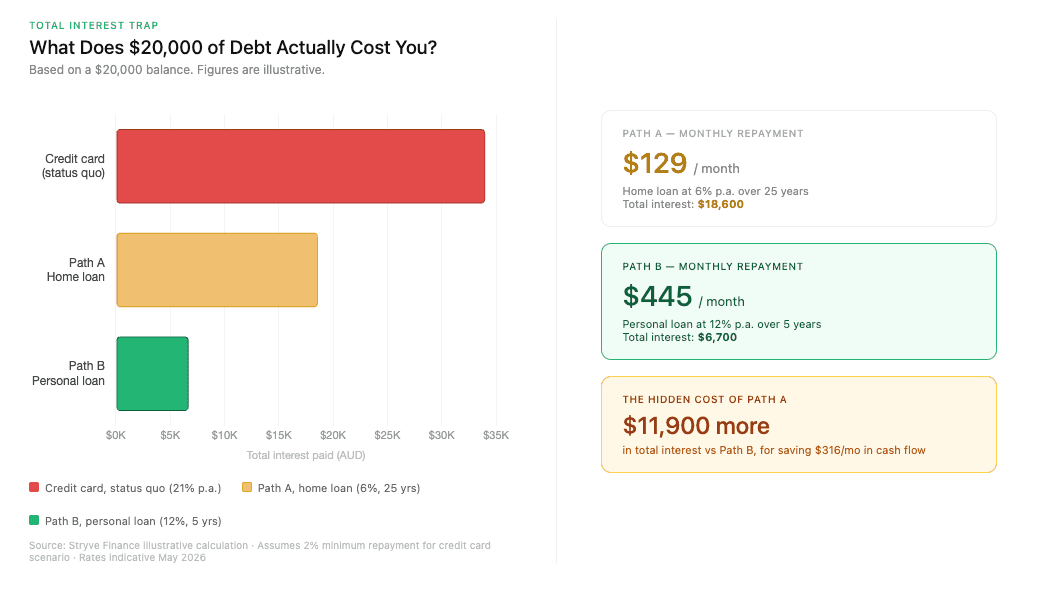

The Total Interest Trap:What the Monthly Saving Really Costs You

Let us put real dollars on the $20,000 credit card scenario. The chart below makes the gap impossible to ignore.

Path A saves you $316 every month, which feels like a win until you realise it costs nearly $12,000 more in total interest over the life of the loan, that is the trap.

Path A: Consolidate into a home loan at 6% p.a. over 25 years

- Monthly repayment: approximately $129

- Total interest paid over 25 years: approximately $18,600

Path B: Personal loan at 12% p.a. over 5 years

- Monthly repayment: approximately $445

- Total interest paid over 5 years: approximately $6,700

Path A saves you roughly $316 per month in cash flow. But it costs you nearly $12,000 more in total interest over the life of the loan.

That is the total interest trap. The monthly saving feels like a win, but the long-term cost tells a different story.

The home loan path only wins on total cost if you commit to making extra repayments to clear the consolidated portion faster. Without that discipline, you are paying for a credit card balance well into your 60s or 70s.

You also need to account for the refinancing costs you need to factor in, including discharge fees, application fees, and valuation costs. These can run into the thousands and eat directly into your savings.

As Moneysmart warns, debt consolidation may cost more overall if the interest rate or fees are higher, or if the loan term is extended.

See what you could save with a debt consolidation refinance. A Stryve Finance broker can run both scenarios with your actual numbers across 50+ lenders.

The risk you need to understand: unsecured debt becomes secured

This is the risk that deserves its own section, not a footnote.

When you consolidate credit card or personal loan debt into a home loan, you convert unsecured debt into secured debt. Your property is now collateral for what was previously debt that could not touch your home.

The consequence is straightforward. If you fall behind on repayments, the lender can take action against your property for debt that originally had no claim on it. A $20,000 credit card balance that once carried no asset risk now sits inside a loan secured by your biggest asset.

This is the central trade-off of a debt consolidation home loan, and it is the reason consolidation is not automatically the right move for everyone. The National Debt Helpline identifies this secured-for-unsecured swap as a key risk that borrowers must understand before proceeding.

Is debt consolidation a good idea? Honest pros and cons

Pros of consolidation:

- One single repayment instead of juggling multiple debts

- Potentially lower interest rate than your current debts

- Reduced monthly cash flow pressure

- Clear end date if the loan is structured well

Cons of consolidation:

- Total interest may increase significantly over a longer term

- Unsecured debt becomes secured, putting your home at risk. See the risk section above for the full implications.

- Temptation to re-accumulate debt on cleared credit cards

- Fees and break costs can erode or eliminate savings

- False sense of progress without genuine behavioural change

Moneysmart explicitly warns that consolidating can lead to deeper debt if the borrower gains access to more credit and is tempted to spend more. Closing the cleared credit cards is essential.

When consolidation is the wrong choice:

- You are near the end of your home loan term (adding debt resets the clock)

- You have no plan to change the spending habits that created the debt

- Your debt balances are small enough that fees outweigh savings

- You are in genuine financial hardship

If you are in that last category, free financial counselling through the National Debt Helpline (1800 007 007) is a better first step than any loan product. Moneysmart also recommends negotiating directly with creditors or exploring hardship provisions before consolidating.

Which Path is Best for You? A Quick Decision Checklist

Home loan consolidation is best if: You have significant equity, a large debt balance ($15,000+), a long remaining mortgage term, and the discipline to make extra repayments on the consolidated amount.

Personal loan consolidation is best if: Your debts are smaller, you do not have sufficient equity, or you want a fixed end date that forces the debt to zero within a few years.

Doing nothing (and attacking the debt directly) is best if: You are near the end of your mortgage term, your balances are small, or the fees of switching would outweigh the savings.

Self-qualification checklist before you call a broker:

- Do you have at least 20% equity? (Your LVR, or loan-to-value ratio, needs to be low enough to avoid triggering LMI, or Lenders Mortgage Insurance.)

- Is your total unsecured debt above $10,000 to $15,000?

- Do you have 15+ years remaining on your home loan?

- Are you confident you will not re-accumulate debt on cleared cards?

- Can you commit to extra repayments on the consolidated amount?

- Have you factored in all switching fees and break costs?

If you answered yes to most of those, the home loan path is worth exploring with real numbers. If your credit history has some marks on it, there are still refinancing options for borrowers with bad credit worth considering.

Get a personalised comparison across 50+ lenders. A Stryve Finance broker can map both paths to your specific situation.

How a Stryve Finance Compares Both Paths for You

A Stryve Finance broker can run both scenarios side by side: the home loan consolidation path and the personal loan path, with actual rates and fees from over 50 lenders. You see which option genuinely saves you money, not which one pays the highest commission.

That means full lender commission transparency and no hidden fees. If the numbers show that consolidation is not the right move, a good broker will tell you that too.

If the home loan path is right for your situation, the next step is exploring a debt consolidation refinance with a Stryve Finance broker who will walk you through the numbers with no surprises.

Talk to a Stryve Finance broker about your debt consolidation options. Get a side-by-side comparison built around your actual debts, your equity, and your goals.

Frequently Asked Questions About Debt Consolidation Loans

Is debt consolidation a good idea?

It depends on your situation. Consolidation can reduce your monthly repayments and simplify your finances, but it may cost you more in total interest if the loan term is extended. The pros and cons section above breaks down exactly when it works and when it does not.

What is the difference between a debt consolidation home loan and a personal loan?

A debt consolidation home loan rolls your debts into your mortgage at a lower rate (around 6% p.a.) but over a much longer term (25 to 30 years). A personal loan typically charges 10 to 20% p.a. but clears the debt in 3 to 7 years. The comparison table above covers all eight dimensions you should weigh up.

What is the best debt consolidation loan in Australia?

There is no single best debt consolidation loan in Australia. The right option depends on your equity, debt size, income, and goals. A Stryve Finance broker in Sydney can compare across 50+ lenders to identify the top debt consolidation loans and low rate debt consolidation loans available for your specific profile.

How does debt consolidation work?

Debt consolidation involves replacing multiple debts with a single loan, ideally at a lower interest rate. As Moneysmart defines it, this means replacing or extending an existing loan with funds from the same or a different financial institution. You then make one repayment instead of several, and the total cost depends on the rate, term, and fees of the new loan.

Can I consolidate credit card debt into my home loan?

Yes, this is the most common use case. A credit card debt consolidation loan through your home loan can dramatically lower your interest rate. But you need sufficient equity, and you must understand that your property becomes collateral for that credit card debt. The risk section above explains why this matters.

Dylan Bertovic is the Director and Senior Finance Broker at Stryve Finance, specialising in non-traditional lending solutions. He helps clients across Australia with tiny home loans, construction finance, equipment and asset lending, refinancing, and investor loans. With deep expertise in self-employed and renovation mortgages, Dylan is known for crafting tailored strategies that get results