Published: May 2026. This article is refreshed regularly to reflect current rate conditions.

Yes, you can refinance a fixed rate mortgage at any point during the fixed period. A fixed rate mortgage refinance is possible before your term expires, though break costs will apply. You should get a formal quote from your lender before deciding whether the numbers stack up for your situation.

Let's get the big question out of the way first. Yes, you can exit a fixed rate home loan at any point during the fixed period. You do not need to wait until your term expires. But whether you should is a different question entirely, and the answer depends on your specific numbers.

If you have been feeling stuck in your fixed rate, you are not alone. Thousands of Australian borrowers are asking whether they can refinance a fixed rate mortgage right now, and for good reason. With multiple rate movements in 2026, the landscape has shifted materially. Stryve Finance, a Sydney-based mortgage broker, helps borrowers in exactly this position work out whether breaking early makes financial sense.

Here's where it gets interesting. There are two very different groups of borrowers asking this question right now.

- Group one: You locked in at a low rate back in 2020 to 2022, your term is ending soon, and you're about to roll onto a much higher variable rate.

- Group two: You locked in at a higher fixed rate more recently, and you're now seeing better deals elsewhere.

The gap between fixed and variable rates has narrowed significantly. Many lenders' fixed mortgage refinance rates currently range between 5.9% and 6.8%, while variable rates sit between 5.7% and 6.5% (rates as at May 2026). That's a meaningful shift, and it's why so many borrowers are rethinking their fixed rate after the 2026 rate rises.

This guide covers both scenarios. By the end, you'll have a concrete framework to decide whether breaking your fixed rate home loan is worth it, before you speak to anyone.

Which type of fixed rate borrower are you?

Scenario A: the legacy low-rate borrower. You locked in around 2% in 2021 and your fixed term is expiring or has already expired. Your goal is to refinance strategically at or near expiry to secure the best possible rate. If your term is nearly up, break costs may be minimal or zero.

Scenario B: the recent high-rate borrower. You locked in at 6.5% or higher in late 2023 or 2024 and you are now seeing better deals on the market. Breaking mid-term may save you thousands, but the break cost is the central barrier you need to calculate first.

Both situations are legitimate. Both are common. And Moneysmart confirms you do not need to wait until the end of your fixed term to refinance. Exit is possible at any point, though break costs will apply.

The rest of this article addresses both scenarios. The break cost calculation is the key variable that determines the right move for you.

What break costs are and why they change every day

Break costs confuse almost everyone, so here's how they work in plain English.

When you locked in your fixed rate, your lender effectively hedged that rate on the wholesale market. They locked in a wholesale swap rate to fund your loan for the agreed term. If wholesale rates have moved since then, the break cost reflects the difference between what they locked in and what they can now get for the remaining term on your loan.

Here's the critical point: break costs can change daily. They're tied to wholesale swap rates, not the RBA cash rate directly. A quote you get on Monday could be materially different by Friday. This is not a stable number you can look up on a website.

That's why you must get your break cost in writing from your current lender before making any decision. This is a formal quote, not a rough estimate from a comparison site. It's the only number you can rely on.

A worked example: is it worth breaking with 18 months left?

Let's put real numbers to this. The example below is illustrative only. Your actual figures will differ based on your lender, loan balance, and the day you request your quote.

The scenario:

| Detail | Amount |

|---|---|

| Loan balance | $500,000 |

| Current fixed rate | 6.5% |

| Remaining fixed term | 18 months |

| Best available variable rate | 5.8% |

| Rate differential | 0.7% |

The monthly saving:

A 0.7% rate reduction on a $500,000 balance saves roughly $200 per month in interest. Over the remaining 18 months of the fixed term, that's approximately $3,600 in total interest savings.

The break-even logic:

Now layer in the break cost. Depending on wholesale rate movements, a break cost on this loan might fall in the $3,000 to $5,000 range.

- If your break cost is $3,000: you save $200/month, so you break even in 15 months. That's inside your remaining 18-month term. Worth exploring.

- If your break cost is $6,000: you'd need 30 months to break even. That's well beyond your remaining term. Not worth it.

This is why the exact break cost quote matters so much. A difference of a few thousand dollars flips the entire decision.

And remember, Moneysmart notes there can be more than a 2% difference between variable home loan rates on the market. The rate you switch to matters enormously. Don't just compare against the average. Compare against the best rate you can actually qualify for.

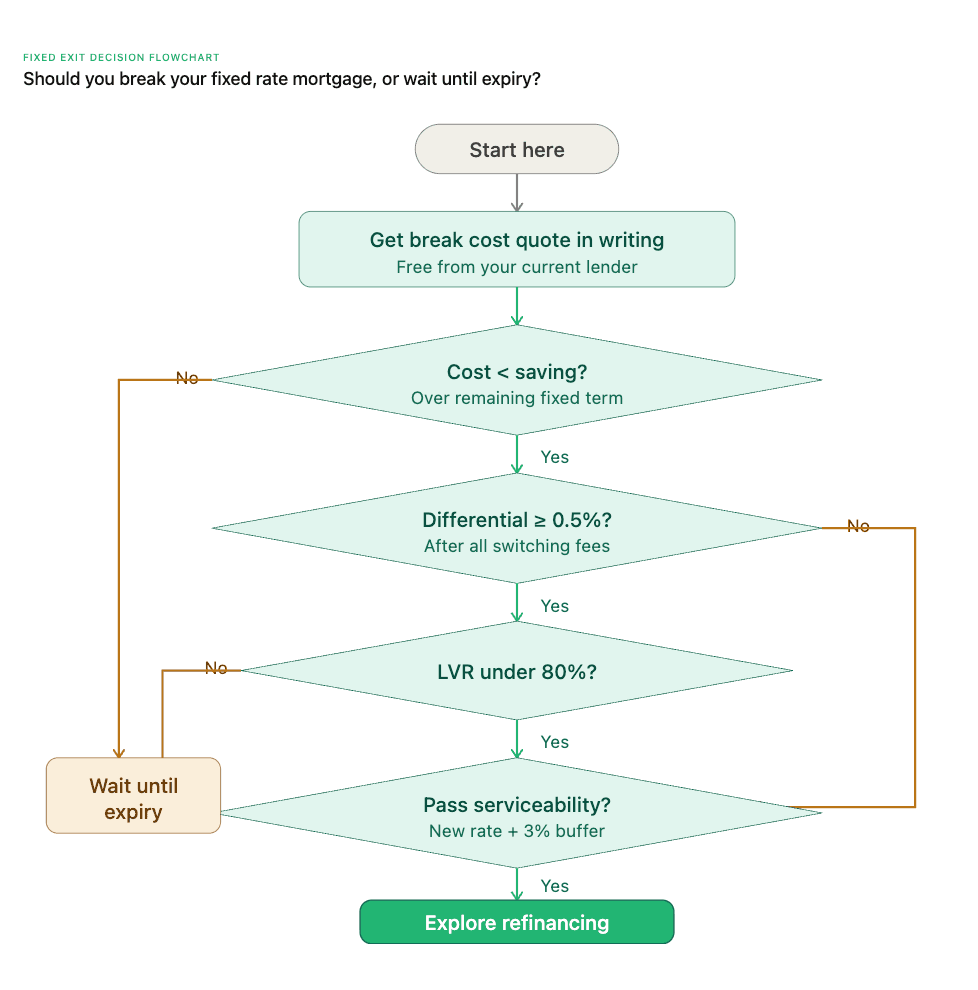

Is it worth breaking your fixed rate

Before you call anyone, run through this checklist. If you can tick all five, breaking your fixed rate is likely worth exploring seriously. If you fail on two or more, waiting until expiry may be the smarter move.

Work through the flowchart below first, if you reach the green box, the numbered checklist that follows will confirm the detail behind each step.

Each decision point in the flowchart maps directly to one of the five conditions below, here is what to check for each one.

The five-point test before you refinance out of a fixed rate:

- Your break cost is less than the total interest saving over the remaining fixed term. This is the fundamental equation. If the saving doesn't exceed the cost, stop here.

- The rate differential is at least 0.5% to 0.7% after accounting for all switching costs. A tiny rate drop won't cover the fees involved.

- Your remaining fixed term is long enough to recoup the total cost of switching. That means break cost plus discharge fee plus any establishment fee on the new loan.

- Your LVR (loan-to-value ratio) hasn't changed in a way that would trigger LMI (Lenders Mortgage Insurance). If your property value has dropped, you could face unexpected insurance costs.

- You can pass the current serviceability assessment. Your new lender will stress-test your income at a higher rate. More on this below.

If you tick all five, the numbers are on your side. If you're unsure on one or two items, it's worth getting the formal quotes to confirm. See what you could qualify for. Get a free refinance assessment.

What refinancing a fixed rate loan actually costs from start to finish

Break costs get all the attention, but they are not the only expense. Here is the full cost inventory you need to account for when you refinance a fixed rate mortgage:

| Cost item | Typical range | Who charges it |

|---|---|---|

| Break cost | Varies widely; can be $0 to $20,000+ | Current lender |

| Discharge fee | $150 to $400 | Current lender |

| Establishment fee | $0 to $600 | New lender |

| Valuation fee | $0 to $300 (may be waived) | New lender or valuer |

| LMI re-trigger risk | Thousands if LVR exceeds 80% | New lender (LMI provider) |

The total switching cost is what actually matters for your decision, not just the break cost in isolation. Add every line item together, then compare that total against your projected interest savings.

Why some borrowers cannot refinance even when the numbers look right

This is the barrier nobody talks about, and it catches more borrowers than you'd expect.

When you refinance, your new lender must run a completely fresh borrowing capacity assessment. APRA (the Australian Prudential Regulation Authority) requires lenders to assess you at the loan interest rate plus a 3% serviceability buffer.

In practice, that means if your new loan rate is 5.8%, you'll be assessed as though you're paying 8.8%. If your income hasn't changed much but rates have risen significantly since your original loan, you may not qualify for the same amount you currently owe.

This is particularly relevant if you stretched to get into the property market as a first home buyer. The loan you were approved for three years ago may not be the loan you'd be approved for today.

If serviceability is a concern, you have options: paying down other debts, extending your loan term, or working with a Stryve Finance broker who can identify lenders with more favourable serviceability policies, since not all lenders assess identically.

What to do if a full break does not stack up

If the full break doesn't stack up on the checklist but doing nothing feels wrong, there are middle-ground options.

- Partial breaks: Some lenders allow you to break a portion of your fixed loan while keeping the rest fixed. This reduces your break costs while giving you some exposure to a better rate. Not all lenders offer this, so you'll need to ask.

- Split loan refinancing: If your loan is already split (part fixed, part variable), you may be able to refinance just the variable portion without triggering any break costs on the fixed portion. This can be a smart way to capture a better variable rate now while letting the fixed portion run its course.

Both options are worth discussing with your lender or broker to understand when refinancing makes sense for your situation.

How a Stryve Finance broker makes this easier

By this point, you've got the framework. You understand break costs, the full switching cost picture, and the serviceability hurdle. A broker's value is in turning that framework into precise numbers for your situation.

A Stryve Finance broker in Sydney can request indicative break cost quotes from your current lender, then model the switch across 50+ lender alternatives before you commit to anything. You get a precise comparison of your break cost against potential savings, with full transparency on lender commissions and no obligation until the numbers make sense for you.

Talk to a Stryve Finance broker about your fixed rate options.

The three-step process from today to settlement

Three things to do from here:

- Call your current lender and request a formal break cost quote in writing. This is free and commits you to nothing.

- Run the numbers against the Fixed Exit Checklist above. You'll know within minutes whether the math is in your favour.

- Book a no-obligation broker call to validate the math and see what's available across 50+ lenders.

The quote is free. The broker call is free. Nobody is committed to anything until the numbers make sense for you.

Feeling stuck in a fixed rate is common right now. Understanding your options is the first step to taking back control.

Get a personalised break cost assessment. talk to a Stryve Finance and see what refinancing could save you across 50+ lenders, with no obligation.

Frequently Asked Questions

Can I refinance a fixed rate mortgage before the term ends?

Yes. You can exit a fixed rate home loan at any point during the fixed period, not just at expiry. However, break costs will apply and you should get a formal quote in writing from your current lender before making any decision.

How much does it cost to break a fixed rate home loan?

It depends on your loan balance, remaining term, and the difference between your fixed rate and current wholesale rates. Break costs can range from a few hundred dollars to tens of thousands. The only way to get an accurate figure is to request a formal quote from your lender, and be aware that quote can change daily.

Can I refinance part of my fixed rate loan?

Some lenders allow partial breaks or split loan refinancing. If your loan is already split between fixed and variable, you may be able to refinance just the variable portion without triggering break costs on the fixed portion. Ask your lender or broker about your specific options.

Will I pass the serviceability test if I refinance?

Your new lender will assess you at the current loan rate plus a 3% buffer, as required by APRA. If the new rate is 5.8%, you'll be assessed at 8.8%. If your income or circumstances have changed since your original loan, this could be a barrier. Reducing other debts or extending your loan term can help.

How long does it take to refinance out of a fixed rate?

From break cost quote to settlement, the process typically takes four to eight weeks depending on the lenders involved. Getting your break cost quote early gives you the most time to make an informed decision.

Is it better to break a fixed rate or wait until expiry?

It depends entirely on your break cost figure and the rate differential available to you. Use the Fixed Exit Checklist above to run the maths. If your break cost is less than the total interest saving over your remaining fixed term, and you can pass the serviceability test, breaking early is worth exploring seriously. If the break cost exceeds your projected savings or your remaining term is short, waiting until expiry is usually the smarter move. A Stryve Finance broker can model both scenarios with your actual numbers at no cost.

General advice warning

This article provides general information only and does not constitute financial or credit advice. It does not take into account your personal objectives, financial situation, or needs. Consider your own circumstances and seek professional advice from a qualified mortgage broker or financial adviser before making any financial decisions.

Dylan Bertovic is the Director and Senior Finance Broker at Stryve Finance, specialising in non-traditional lending solutions. He helps clients across Australia with tiny home loans, construction finance, equipment and asset lending, refinancing, and investor loans. With deep expertise in self-employed and renovation mortgages, Dylan is known for crafting tailored strategies that get results