Knowing the exact documents required for a self-employed home loan can mean the difference between a smooth 2-week approval and a frustrating 6-week back-and-forth with your lender. At Stryve Finance, we've helped hundreds of self-employed Australians, sole traders, contractors, company directors, and trust beneficiaries, secure home loans across all major and specialist lenders.

The challenge is real. The Reserve Bank of Australia notes that small-business lending continues to grow steadily, but lenders still view self-employed borrowers as higher risk than PAYG employees. That perception makes strong documentation essential. Get the paperwork right the first time and your application moves quickly. Get it wrong, and even a strong borrower can face delays or outright rejection.

This guide walks you through the complete document checklist, full doc, low doc, and alt doc, plus lender-specific insights you won't find on the big bank websites. If your income varies month to month, our deeper guide on getting a home loan with irregular income is a useful companion read.

Quick Document Checklist for a Self-Employed Home Loan

For a standard (full doc) self-employed home loan in Australia, you'll need:

- Personal tax returns: Last 2 financial years

- ATO Notices of Assessment: Last 2 years

- Business tax returns: Last 2 financial years (for companies, partnerships, and trusts)

- Business financial statements: Profit and loss and balance sheet, prepared by a registered accountant

- Bank statements: Personal and business, last 3-6 months

- ABN registration: Typically active for at least 18-24 months

- BAS statements: Last 4 quarters (if registered for GST)

- Identification: 100 points of ID

- Asset and liability declaration: Full list of what you own and owe

Before applying, it's worth running your numbers through our borrowing capacity calculator to get a quick estimate of how much you may be able to borrow.

Who Qualifies as Self-Employed in Australia?

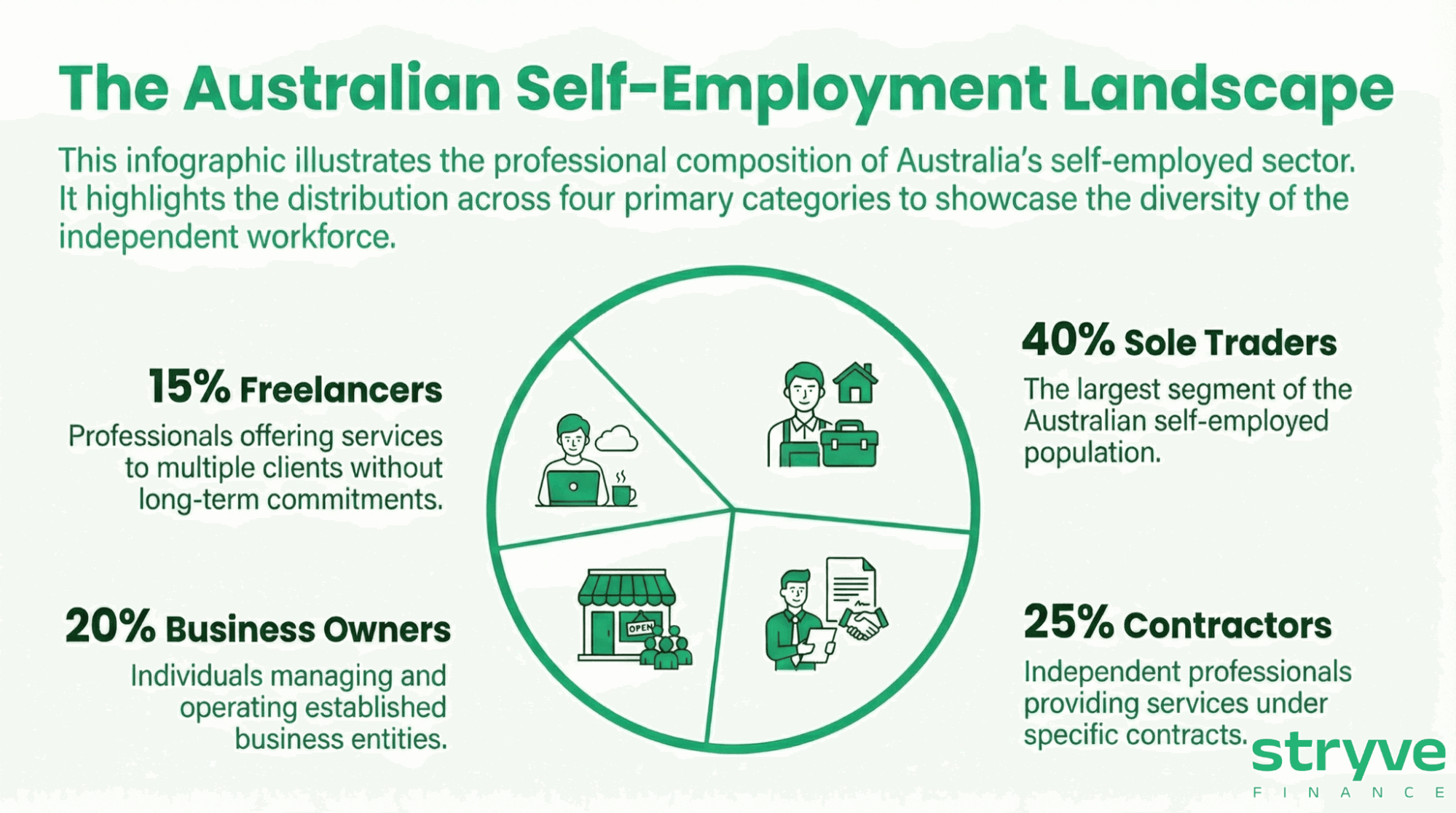

You're classified as self-employed for home loan purposes if you earn income through your own business rather than as a PAYG employee. This includes four main categories:

1. Sole traders

Tradespeople, consultants, freelancers, and other professionals operating under their personal ABN. Document requirements are simpler, usually just personal tax returns (no separate business returns needed). For a deeper breakdown of how lenders assess this structure, see our dedicated guide on sole trader home loans.

2. Contractors and Freelancers

IT consultants, construction workers, creatives, and others working on a contract basis. Some lenders treat long-term contractors with a single client similarly to PAYG employees if the contract has been ongoing for 12 months or more. Our contractor home loans page explains exactly which lenders offer this favourable treatment.

3. Company Directors

If you own 25% or more of a Pty Ltd company, lenders consider you self-employed, even if you pay yourself a regular salary. You'll need both personal and company tax returns. We've covered the specifics in our guide to home loans through a company, and if you pay yourself through dividends, our article on getting a mortgage when you pay yourself in dividends is essential reading.

4. Trust Beneficiaries and Partnerships

If you receive income through a family trust or business partnership, expect to provide trust deeds, partnership agreements, and distribution statements alongside the standard documents.

From our broker desk

“A common surprise for company directors, even when you pay yourself a fixed PAYG-style salary from your own company, almost every lender still treats you as self-employed. We always check ABN ownership percentage early in the conversation to set the right expectations.” - Dylan Bertovic, Stryve Finance

Full Doc vs Low Doc vs Alt Doc - Which Applies to You?

Self-employed home loans come in three documentation tiers. The right one depends on what financial records you can actually produce.

The right strategy: Most self-employed Australians qualify for full doc but don't realise it. At Stryve Finance, we always start by checking full-doc eligibility before exploring alt doc or low doc home loan options, because the interest rates and LVR caps are significantly better.

Core Documents Required for a Self-Employed Home Loan (Full Doc)

1. ABN and GST registration

Your Australian Business Number is the foundation of any self-employed home loan application. Most lenders want to see a minimum of 18-24 months of active ABN history. If you take director's fees or company dividends as income, your ABN or ACN typically needs to be valid for two years.

GST registration is required if your business turnover exceeds $75,000 per year. Lenders use your GST status to cross-check your declared income against your BAS statements.

Lender-specific note: Specialist lenders such as Pepper Money accept ABNs as new as 6 months old. This is exactly where working with a broker matters, we know which lenders match your ABN history. If you've been self-employed for less than two years, our specialist page on home loans for self-employed under 2 years covers the lender shortlist in detail.

2. Personal tax returns (last 2 years)

Your two most recent personal tax returns are the single most important document in your application. Lenders use these to:

- Confirm your declared taxable income

- Identify “add-back” expenses that can increase your serviceable income

- Spot inconsistencies between years that might signal income instability

If your most recent return shows significantly lower income than the prior year, most lenders will assess your borrowing capacity using the lower figure, so timing your application matters. For a deeper look at exactly how lenders interpret tax returns, read our companion guide on self-employed mortgage tax return requirements.

3. ATO Notices of Assessment

Your Notice of Assessment (NOA) is the ATO's confirmation that your tax return has been lodged and processed. Lenders use this to verify your tax return is genuine and final, not a draft. If you haven't lodged your most recent return yet, your options include:

- Lodge as soon as possible and request a fast NOA from the ATO

- Provide an accountant's letter confirming the return is in preparation

- Apply with a lender that accepts older returns (up to 22½ months old in some cases)

4. Business Tax Returns (last 2 years)

If you operate through a company, partnership, or trust, you'll need 2 years of business tax returns in addition to your personal returns. Sole traders don't need separate business returns — your personal return covers it.

5. Business Financial Statements

For companies, partnerships, and trusts, lenders require accountant-prepared financial statements including:

- Profit and Loss Statement: shows business income versus expenses over the last 2 financial years

- Balance sheet: snapshot of business assets, liabilities, and equity

- Depreciation schedule: helps lenders identify add-backs

These should be prepared by a registered tax agent or accountant on their letterhead. Our business owner home loans page outlines the specific company financials each major lender requires.

6. BAS (Business Activity Statements)

If your business is GST-registered, you'll need to provide BAS statements for the last 4 quarters (some lenders ask for 8 quarters on low doc applications). BAS statements show your business turnover and GST activity, giving lenders a recent view of your trading performance between annual tax returns.

7. Bank statements (last 3-6 months)

Lenders typically request 3-6 months of statements for:

- Personal transaction accounts

- Personal savings accounts

- Business operating accounts

- Any account where loan repayments will be drawn

They're looking at your cash flow behaviour: regular deposits matching declared income, no excessive gambling or buy-now-pay-later activity, and savings discipline.

8. Identification documents (100 points of ID)

Standard Australian 100-point ID check, drawn from:

- Driver's licence (40 points)

- Passport (70 points)

- Medicare card (25 points)

- Birth certificate (70 points)

You'll need to clear 100 points across primary and secondary documents.

9. Asset and liability declarations

A full disclosure of:

- Assets: Properties, vehicles, savings, super, investments, business equity

- Liabilities: Existing home loans, car loans, credit card limits (lenders assess on limit, not balance), HECS-HELP, BNPL accounts

From our broker desk

“We see applications get held up over credit card limits more than anything else. A $20,000 credit card limit reduces your borrowing capacity by roughly $80,000-$100,000, even if your balance is zero. Always close or reduce unused cards before applying.” - Dylan Bertovic, Stryve Finance

Additional Documents by Business Structure

Sole traders

- Personal tax returns (2 years)

- ATO Notices of Assessment

- ABN registration certificate

- Bank statements (personal and business)

- BAS (if GST registered)

Partnerships

All sole trader documents, plus:

- Partnership agreement showing ownership splits

- Partnership tax returns (2 years)

- Each partner's individual tax returns

Companies (Pty Ltd)

All sole trader documents, plus:

- Company tax returns (2 years)

- Company financial statements (P&L and balance sheet)

- Director's individual tax returns

- ASIC company extract showing directorship and shareholding

Trusts

All standard documents, plus:

- Trust deed

- Trust tax returns (2 years)

- Distribution statements for each beneficiary

- Identification for trustees and beneficiaries

Documents for Low Doc Home Loans

A low doc home loan is designed for self-employed borrowers who can't produce full tax returns or financial statements. Common scenarios include:

- New business under 2 years old

- Tax returns not yet lodged for the most recent year

- Complex income across multiple business structures

- Recently changed business structure

Typical low doc documentation:

- Self-declared income form, you state your income, signed under truth-in-lending declarations

- Accountant's letter, your accountant confirms your income and that your business is trading profitably

- BAS statements, usually 12 months (4 quarters)

- Business bank statements, 6+ months showing consistent business deposits

- ABN registration, usually 12+ months active

Trade-offs: Low doc loans typically come with a 0.5%-1.5% rate premium and a maximum LVR of 80%, meaning you'll need a 20% deposit (no LMI available). They're a useful bridge, many borrowers refinance to a full doc loan after 2 years of tax returns become available. When you're ready, our self-employed refinance guide explains how to switch from low doc to full doc to access better rates.

What Are “Add-Backs” and Why Do They Matter?

Add-backs are the difference between your taxable income and your serviceable income for home loan purposes. Many self-employed borrowers can borrow far more than their tax return suggests because legitimate business expenses can be “added back” to their assessable income.

Common add-backs lenders accept:

- Depreciation: Non-cash expense on vehicles, equipment, fit-out

- One-off expenses: Equipment purchases, professional fees, unusual costs

- Superannuation: Self-funded super contributions

- Interest on investment debt: If servicing is already assessed elsewhere

- Company car expenses, for vehicles used personally

- Director's salary in own company, adds back to company profit assessment

From our broker desk

“A Brisbane plumber came to us thinking he could only borrow $480K based on his taxable income of $85,000. After our team identified $42,000 in legitimate add-backs, depreciation on two work utes, superannuation contributions, and a one-off tool purchase, his assessable income increased to $127,000. We secured approval for $720K with a major lender.” - Dylan Bertovic, Stryve Finance

Different lenders apply different add-back policies. This is one of the highest-value reasons to work with a specialist broker, the right lender choice can mean $200K+ in extra borrowing capacity on the same financials.

How Long Should You Have Been Self-Employed?

One of the most common questions we hear from self-employed Australians is: “Have I been trading long enough to get approved?” The answer depends on which lenders you approach. The timeline below shows which Australian lenders match each stage of your self-employment journey, from a brand-new ABN to a fully established business of two years or more.

| Time Self-Employed | Lender Options |

|---|---|

| 2+ years | All major banks and specialist lenders. Full doc available. |

| 12-24 months | Many lenders accept with 1 year tax return + strong supporting documents |

| 6-12 months | Specialist lenders only (Pepper Money, Liberty, others). Usually alt doc or low doc. |

| Under 6 months | Very limited. Usually requires prior PAYG income in the same industry. |

Previous experience in the same industry significantly strengthens applications with a short self-employment history. For example, a plumber who has been self-employed for 12 months but worked as an employed plumber for the previous 5 years has a much stronger case than someone making a career change. If you're in this position, our specialist page on self-employed home loans under 2 years shows you the exact lender shortlist.

Tips to Strengthen Your Self-Employed Home Loan Application

1. Maintain a strong credit score

A credit score above 700 opens up the widest range of lenders and the best rates. Pay all bills on time, keep credit utilisation below 30%, and avoid applying for multiple credit products in the 6 months before your home loan application. Our credit score guide breaks down exactly how Australian credit scores are calculated and how to improve yours.

2. Reduce existing debts

Close unused credit cards, pay down personal loans, and consider consolidating BNPL accounts. Every $10,000 in credit card limit reduces your borrowing capacity by approximately $40,000-$50,000.

3. Save a 20% deposit (avoid LMI)

A 20% deposit eliminates Lenders Mortgage Insurance (LMI), which can save you $15,000-$40,000+ depending on loan size. For self-employed borrowers, a larger deposit also signals financial discipline.

4. Keep clean financial records

Separate your business and personal accounts. Maintain consistent monthly drawings. Lodge BAS on time. Avoid maximising every possible tax deduction in the financial year before applying, lower taxable income directly reduces borrowing capacity.

5. Time your application strategically

The ideal window: 3-6 months after lodging your most recent tax return and receiving your NOA. This gives lenders the freshest income evidence and avoids “stale return” issues. Getting pre-approval before house-hunting also strengthens your position with sellers and agents.

6. Work with a self-employed mortgage specialist

The home loan process for self-employed borrowers involves lender-specific policy knowledge that takes years to learn. At Stryve Finance, we have access to 50+ lenders and know which specialist lenders accept which document combinations, saving you weeks of trial and error.

Frequently Asked Questions

What do you need to show for a self-employed mortgage?

For a self-employed mortgage in Australia, you typically need to show 2 years of personal and business tax returns, ATO Notices of Assessment, business financial statements (profit and loss and balance sheet), 3-6 months of bank statements, an active ABN (usually 18-24 months minimum), and BAS statements if you're GST-registered. You'll also need 100 points of ID.

Can I get a home loan if self-employed?

Yes, being self-employed doesn't prevent you from getting a home loan. All major Australian banks and dozens of specialist lenders offer home loans to self-employed borrowers. With full documentation (2 years of tax returns), you can access the same interest rates as PAYG employees. Newer businesses or those with incomplete documentation may need a low doc or alt doc loan, typically through specialist lenders.

What is the documentation required for self-employed borrowers?

The documentation required for self-employed borrowers includes: 2 years of personal tax returns, 2 years of business tax returns (for companies, partnerships, and trusts), ATO Notices of Assessment, accountant-prepared financial statements, bank statements covering 3-6 months, ABN and GST registration certificates, BAS statements for the last 4 quarters, 100 points of ID, and a full asset and liability declaration. Low doc applications substitute some of these with an accountant's letter and self-declared income.

What do lenders look at for self-employed?

Lenders assess self-employed borrowers on four key factors: (1) Income stability: averaged across 2 years of tax returns, (2) Business viability: profitability trends and industry risk, (3) Cash flow behaviour: bank statement analysis showing consistent deposits and responsible spending, and (4) Documentation completeness: ABN longevity, GST registration, BAS lodgement consistency, and credit history.

How many years of tax returns do I need for a self-employed home loan?

Most Australian lenders require 2 years of personal and business tax returns. However, specialist lenders such as Pepper Money, Liberty, and several others accept just 1 year of tax returns with strong supporting documentation, particularly if you have previous experience in the same industry as a PAYG employee.

Can I get a home loan with only 1 year of self-employment?

Yes. Several specialist lenders accept self-employed borrowers with just 12 months of ABN registration and 1 financial year of tax returns. You'll typically need to demonstrate previous industry experience, provide an accountant's letter, and may need a slightly larger deposit. A specialist broker can match you with these lenders, see our dedicated page on self-employed home loans under 2 years for the full lender list.

What is a low doc home loan and who is it for?

A low doc home loan is designed for self-employed borrowers who can't supply full tax returns or financial statements. Instead, lenders accept BAS statements, an accountant's declaration, and business bank statements as income evidence. Low doc loans suit newly self-employed borrowers, those with complex income structures, or anyone whose most recent tax return isn't yet lodged. They typically carry a 0.5-1.5% rate premium and cap at 80% LVR.

Do I need an ABN to apply for a self-employed home loan?

Yes, an active Australian Business Number is essential. Most lenders require your ABN to be registered for at least 18-24 months. Specialist lenders such as Pepper Money accept ABNs as new as 6 months old. If your business turnover exceeds $75,000, you'll also need GST registration.

Are self-employed home loan rates higher than standard rates?

Not always. With full documentation, self-employed borrowers can access the same interest rates as PAYG employees from most major lenders. Low-doc and alt-doc loans carry a rate premium of 0.5-1.5% to reflect the lender's increased reliance on alternative income evidence.

What is an “add-back” on a self-employed home loan application?

Add-backs are non-cash or one-off expenses that reduce your taxable income on paper but don't affect your actual cash flow. Lenders may add back items such as depreciation, superannuation contributions, one-off business purchases, and company car expenses to your assessable income, often increasing your borrowing capacity by $100,000 or more.

Ready to Apply? Let’s Get Your Documents in Order

At Stryve Finance, we specialise in self-employed home loans. Whether you're a sole trader, contractor, company director, or running a complex trust structure, our team knows exactly which lenders suit your situation and which documents each one requires.

Here's what happens when you book a free consultation with Stryve:

- We review your business structure and income evidence in a 30-minute call

- We identify add-backs and other capacity boosters most brokers miss

- We match you with 2-3 lenders most likely to approve your specific situation

- We package your documents to lender specification, eliminating delays

- You get a clear answer on borrowing capacity before formally applying

Book your free self-employed home loan consultation →

Your dream home is closer than you think, even if you work for yourself.

Stryve Finance is an Australian credit licensed mortgage broker (ACL 384704) specialising in self-employed home loans. This article is general information only and does not constitute personal financial advice. Lender policies change frequently, verify current requirements with a Stryve broker before applying.

Dylan Bertovic is the Director and Senior Finance Broker at Stryve Finance, specialising in non-traditional lending solutions. He helps clients across Australia with tiny home loans, construction finance, equipment and asset lending, refinancing, and investor loans. With deep expertise in self-employed and renovation mortgages, Dylan is known for crafting tailored strategies that get results