If your pay changes from month to month, you've probably wondered whether a lender will take you seriously. The short answer: yes, you can get a home loan with irregular income, you just need to present your finances in a way lenders can understand and trust.

A growing share of Australians earn outside the traditional full-time salary, through casual shifts, freelance contracts, commissions, gig work and self-employment. Lenders see this kind of income every day, and many have policies built specifically for it. The challenge isn't whether you earn enough; it's proving that your income is stable and likely to continue.

At Stryve Finance, we help borrowers with non-traditional income get approved every week. This guide breaks down how lenders assess irregular income, what documents you'll need, how much you might borrow, and the strategies that turn a “maybe” into a “yes”.

What Is Irregular Income?

Irregular income is any earnings that fluctuate in amount or timing, rather than arriving as a fixed salary on a predictable cycle. It can come from one source or several.

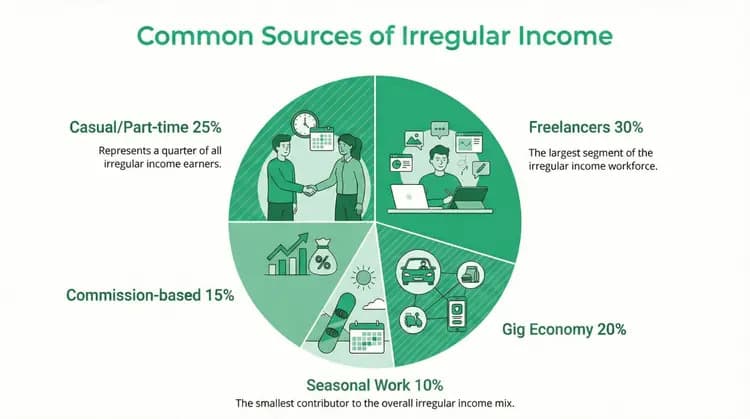

Common examples include:

- Freelancers and independent contractors

- Gig-economy workers (rideshare, delivery, task platforms)

- Self-employed business owners and sole traders

- Casual and part-time employees

- Commission-based roles such as sales and real estate

- People juggling multiple part-time jobs

- Seasonal workers in tourism, agriculture or events

To help you visualise the most common types of irregular income, here's a quick breakdown by category:

If your income doesn't follow a steady pay cycle, some lenders may view it as higher risk, but that perception is manageable. The key is understanding how lenders measure income stability, and giving them the documentation that backs it up.

Can You Get a Home Loan with Irregular Income?

Yes. Traditional banks don't automatically decline borrowers with fluctuating income, but they do apply closer scrutiny to make sure your earnings can support repayments over the life of the loan. Where you apply matters just as much as how much you earn.

Traditional lenders (major banks)

The major banks usually look for:

- A consistent income history, often around two years

- Evidence of ongoing work in the same field or industry

- Full financial documentation such as tax returns and bank statements

Banks may also be conservative with variable income, for example, only counting a portion of overtime, bonuses or commissions rather than the full amount.

Specialist and non-bank lenders

Specialist and non-bank lenders are typically more flexible with casual workers, freelancers and sole traders. They often offer low-doc or alt-doc loans, use custom assessment criteria, and accept a wider range of income types. Specialist lenders have built a significant part of the market around borrowers who don't fit the standard mould.

This is where a broker earns their keep: at Stryve we work across a panel of both bank and non-bank lenders, so we can match your situation to the lender most likely to say yes, instead of you guessing and risking a knockback.

How Lenders Assess Irregular Income

Whatever your income looks like, every lender is trying to answer one question: can this borrower comfortably afford the repayments over time? Here's how they work it out.

1. Income averaging

Rather than relying on one or two pay periods, most lenders average your income over a set window, commonly the last 6 to 24 months. For example, if your monthly income ranged from $3,000 to $7,000 over the past year, a lender might assess you on an average of around $5,000 a month. The longer and more consistent your track record, the more confident the lender will be.

2. The serviceability buffer

Here's something most articles skip, and it catches a lot of borrowers out. Lenders don't assess you at the actual interest rate, they add a serviceability buffer on top. In line with APRA guidance, lenders typically test whether you could still afford repayments at roughly 3 percentage points above the loan's interest rate. On irregular income, this buffer is exactly why a strong, well-documented income history matters: it gives you more headroom in the assessment.

3. How long you've earned this way

Time in role (or in business) is a major factor. As a rough guide, many lenders want to see around 6 to 12 months in a casual or contract position, and about two years of self-employment. That said, policies vary widely, some lenders accept shorter histories, a single year of tax returns, or strong industry experience even after a recent job change. A freelancer with three years in the same field is viewed far more favourably than someone who started last month.

4. Verifiable, traceable income

Lenders want income they can document and trace. Tax returns, bank statements, BAS, invoices, payslips and ATO income summaries all help build the paper trail. The more your deposits line up with your declared income, the smoother the assessment.

How Much Can You Borrow on Irregular Income?

Your borrowing power on irregular income comes down to your assessable income, the figure the lender accepts after averaging and after discounting any variable components, minus your living expenses and existing debts, all stress-tested against that serviceability buffer.

Two borrowers earning the same headline figure can end up with very different borrowing limits, depending on how much of their income a particular lender will count. That's why running the numbers with the right lender policy in mind is so valuable.

A good starting point is our borrowing capacity calculator for a ballpark figure, then a broker can refine it against lenders that treat your income type generously.

What Documents Do You Need?

With irregular income, your documentation does the heavy lifting. The stronger the evidence, the more confident a lender will be, even when your income varies. Requirements differ by income type.

Here's a side-by-side comparison of the key documents required for different income types, so you can quickly see what applies to your situation:

Self-employed, freelancers and contractors

- Two years of personal and/or business tax returns

- ATO income summary (formerly the PAYG summary)

- Around 12 months of bank statements showing income deposits

- BAS, if you're registered for GST

- ABN and business registration details

- A profit and loss statement, especially for sole traders

Our guides on documents required for a self-employed home loan and self-employed tax return requirements go deeper on getting this right.

Casual and part-time employees

- Recent payslips, typically covering the last 6 to 8 weeks

- An employment letter confirming your role, hours and income

- A group certificate or ATO income summary

- Bank statements showing your pay landing

Tip: if you earn from multiple jobs or gigs, lenders can often consider your combined income, as long as each stream is properly documented. Getting the paperwork packaged correctly is frequently the difference between approval and rejection, and it's exactly what we handle for you.

Can Centrelink, Bonuses or Side Hustles Count as Income?

When you're applying with irregular income, every reliable stream can help, but lenders treat each type differently.

Income that may be accepted

- Centrelink payments: Some lenders accept Family Tax Benefit, Parenting Payment or the Disability Support Pension, particularly alongside employment income.

- Bonuses and commissions: If received regularly over 12 months or more and evidenced by payslips or tax returns, many lenders will average them in (often counting a portion rather than 100%).

- Side hustle or secondary income: Freelancing, rideshare or online selling can support your application if it's run for at least 6 to 12 months and is backed by bank statements or BAS.

- Rental income: Usually counted at around 70 to 80% to allow for vacancies and costs.

Income that usually isn't accepted

- One-off lump sums such as an inheritance or a single short gig

- Temporary contracts with no prospect of extension

- Informal cash work with no paper trail

- Most one-off, non-taxed payments

As an example, a casual retail worker who also drives rideshare and receives Family Tax Benefit could potentially be assessed on all three sources, provided each is documented. We'll help you work out what's usable and find lenders that recognise the full scope of your earnings.

Does Your Credit Score Matter?

Yes, your credit profile still counts, and on irregular income it can carry extra weight, because lenders are already looking harder at risk. A solid repayment history, low existing debt and few credit enquiries all strengthen your position. If your score isn't where you'd like it, it's worth understanding what credit score you need for a home loan before you apply, so a string of applications doesn't leave marks on your file.

Deposit and LMI with Irregular Income

Deposit expectations are broadly the same as for any borrower, but specialist and low-doc lenders sometimes ask for a larger one (often 20% or more) to offset the perceived risk. Below a 20% deposit, you'll generally pay Lenders Mortgage Insurance (LMI) a one-off cost that protects the lender, not you. A bigger deposit can lower your LMI, improve your rate options, and widen the pool of lenders willing to consider you. Our explainer on how LMI works covers the detail.

Alternative Loan Options for Irregular Income

If the major banks are too rigid for your situation, there are well-established alternatives.

Low-doc loans

Low-doc loans suit self-employed borrowers who can't provide full tax returns. Instead, lenders may accept BAS, bank statements or an accountant's declaration.

Trade-offs: easier to qualify and more flexible documentation, but often slightly higher rates, lower borrowing limits and larger deposit requirements.

Guarantor loans

If a family member (usually a parent) will guarantee part of your loan, a guarantor loan can help you borrow more and reduce or avoid LMI.

Trade-off: the guarantor takes on real risk if you can't repay, so it's a serious commitment on both sides.

Specialist (non-bank) lenders

These lenders focus on your real-world income rather than a rigid template, and often accept multiple income streams, seasonal earnings and short-term contract income. They typically work through brokers, which is where we come in.

If you're an independent contractor or sole trader, there are lenders and products built specifically for how you earn.

Tips to Strengthen Your Application

A few practical moves can meaningfully improve your chances:

- Build a longer track record, the more months of consistent income you can show, the better.

- Keep clean, organised records, tidy bank statements and up-to-date tax returns make assessment easier.

- Lodge your tax returns on time, self-employed borrowers can't be assessed on income they haven't declared.

- Reduce other debts, clearing credit cards and personal loans frees up borrowing power.

- Get pre-approval first, knowing your position before you shop is invaluable; here's how to get home loan pre-approval.

- Apply through the right lender the first time, multiple knockbacks can hurt your credit file.

Why Work with a Mortgage Broker Like Stryve Finance

With irregular income, choosing the right lender is only half the job, the real skill is presenting your income so lenders trust it. That's where a broker makes the difference.

- We know the lender policies. Every lender treats casual, freelance and self-employed income differently. We know who says yes, so you don't waste applications.

- We position your income strategically. Whether you earn from gigs, commissions or multiple streams, we package your documents to show consistency and reliability.

- We protect your credit file. Rather than scattering applications, we submit where you're most likely to succeed.

- We advocate for you. Seasonal income? Multiple streams? We explain your situation directly to the lender so they see the full picture, not just a number.

If you're weighing up going direct versus using a broker, our piece on why use a mortgage broker lays out the difference.

Ready to get started?

Irregular income doesn't have to stand between you and your own home. Book a free consultation with a Stryve Finance broker, and we'll help you build an application lenders can say yes to.

Frequently Asked Questions

Can I get a home loan if I'm a casual worker?

Yes. Many lenders accept casual income, especially once you've been in the same role or industry for around 6 to 12 months. They'll usually average your income and may want an employment letter confirming your hours.

How many years of income history do I need?

It varies by lender. Self-employed applicants are often asked for two years of tax returns, while casual and contract workers may qualify with 6 to 12 months in a role. Some lenders accept shorter histories or a single year of returns, which is where the right lender match matters.

Will lenders count my overtime, bonuses or commissions?

Often, yes, if they're regular and documented over 12 months or more. Lenders commonly count a portion (frequently around 80%) rather than the full amount, to allow for variability.

Can I use Centrelink payments towards a home loan?

Some lenders will consider stable, ongoing payments such as Family Tax Benefit or the Disability Support Pension, usually alongside employment income. Acceptance varies between lenders.

Do I need a bigger deposit with irregular income?

Not always, but some specialist and low-doc lenders ask for a larger deposit (often 20% or more) to offset risk. A bigger deposit can also reduce or remove LMI and open up better rates.

Is it harder to get approved with irregular income?

It can require more preparation and the right lender, but it's far from impossible. Strong documentation, a consistent track record and a broker who knows which lenders suit your income type all make approval realistic.

Dylan Bertovic is the Director and Senior Finance Broker at Stryve Finance, specialising in non-traditional lending solutions. He helps clients across Australia with tiny home loans, construction finance, equipment and asset lending, refinancing, and investor loans. With deep expertise in self-employed and renovation mortgages, Dylan is known for crafting tailored strategies that get results